Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- smartCRE - Redefining ExpDokument7 SeitensmartCRE - Redefining Exprizwan_habibNoch keine Bewertungen

- Lord Dalhousie and His ReformsDokument5 SeitenLord Dalhousie and His Reformsrizwan_habibNoch keine Bewertungen

- Is Active Euthanasia The Next Step - The HinduDokument3 SeitenIs Active Euthanasia The Next Step - The Hindurizwan_habibNoch keine Bewertungen

- Current Affairs Feb Mar 2018 PDFDokument75 SeitenCurrent Affairs Feb Mar 2018 PDFrizwan_habibNoch keine Bewertungen

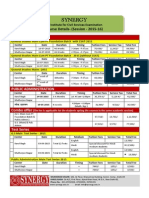

- Fees Structure Final With ModulesDokument2 SeitenFees Structure Final With Modulesrizwan_habibNoch keine Bewertungen

- Death Penalty India Report Summary PDFDokument50 SeitenDeath Penalty India Report Summary PDFrizwan_habib100% (1)

- Writ Petition and AffidavitDokument6 SeitenWrit Petition and Affidavitrizwan_habibNoch keine Bewertungen

- Candidate Collaboration AAGDokument2 SeitenCandidate Collaboration AAGrizwan_habibNoch keine Bewertungen

- Death Penalty India Report Summary PDFDokument50 SeitenDeath Penalty India Report Summary PDFrizwan_habib100% (1)

- 7th Pay CommissionDokument2 Seiten7th Pay Commissionrizwan_habibNoch keine Bewertungen

- Time Table of DTC Bus RoutesDokument567 SeitenTime Table of DTC Bus Routesrizwan_habibNoch keine Bewertungen

- (MOTIVATION) Madhusudhan Hulgi Rank 392, CSE - 2014: Three Times Failed To Clear Prelims, Fourth Time Secured A RankDokument5 Seiten(MOTIVATION) Madhusudhan Hulgi Rank 392, CSE - 2014: Three Times Failed To Clear Prelims, Fourth Time Secured A Rankrizwan_habibNoch keine Bewertungen

- Constitutional Parties in IndiaDokument5 SeitenConstitutional Parties in Indiarizwan_habibNoch keine Bewertungen

- Principles of Natural Justice PDFDokument13 SeitenPrinciples of Natural Justice PDFविशाल चव्हाण100% (2)

- General Science Printed Notes @aspire PDFDokument48 SeitenGeneral Science Printed Notes @aspire PDFsweetakamNoch keine Bewertungen

- Representation of The People Act, 1951Dokument67 SeitenRepresentation of The People Act, 1951kewal1829Noch keine Bewertungen

- Press Advertisement Notice Dated 05-Feb-2015Dokument1 SeitePress Advertisement Notice Dated 05-Feb-2015rizwan_habibNoch keine Bewertungen

- MMC 204Dokument145 SeitenMMC 204rizwan_habibNoch keine Bewertungen

- Urbanization's Impact on the EnvironmentDokument16 SeitenUrbanization's Impact on the Environmentrizwan_habibNoch keine Bewertungen

- Hostels For Post Graduate StudentsDokument3 SeitenHostels For Post Graduate Studentsrizwan_habibNoch keine Bewertungen

- State Branch Address &telephone Nos. (Updated 25-02-2015)Dokument15 SeitenState Branch Address &telephone Nos. (Updated 25-02-2015)rizwan_habib100% (1)

- Our biggest asset is our people – Suneeth Katarki & Srinivas Katta, IndusLawDokument11 SeitenOur biggest asset is our people – Suneeth Katarki & Srinivas Katta, IndusLawrizwan_habibNoch keine Bewertungen

- Spark-LED Intelligent Lead Brand-Led Light ManufacturerDokument2 SeitenSpark-LED Intelligent Lead Brand-Led Light Manufacturerrizwan_habibNoch keine Bewertungen

- Betraying Indiasdas WildlifeDokument4 SeitenBetraying Indiasdas WildlifeRohith NairNoch keine Bewertungen

- The Hindu-Dairy Events of 2013Dokument82 SeitenThe Hindu-Dairy Events of 2013Jitendra BeheraNoch keine Bewertungen

- Air Pollution: Prepared For Class Discussion by Prof. S.SuryanarayananDokument8 SeitenAir Pollution: Prepared For Class Discussion by Prof. S.SuryanarayananAmal BharaliNoch keine Bewertungen

- LSDokument24 SeitenLSrizwan_habibNoch keine Bewertungen

- Commissions and Committees-1Dokument7 SeitenCommissions and Committees-1rizwan_habibNoch keine Bewertungen

- Commissions and Committees-1Dokument7 SeitenCommissions and Committees-1rizwan_habibNoch keine Bewertungen

- Employee Experience DatabaseDokument6 SeitenEmployee Experience Databaserizwan_habibNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- G2593R9Dokument21 SeitenG2593R9TanaNoch keine Bewertungen

- Indian Steel IndustryDokument28 SeitenIndian Steel Industrykeanu100% (1)

- SA336Dokument10 SeitenSA336ismaelarchilacastilloNoch keine Bewertungen

- RG 1.43 PDFDokument3 SeitenRG 1.43 PDFAlex GutierrezNoch keine Bewertungen

- (Welding) MIG-MAG Welding Guide - Lincoln Electric (Ebook, 48 Pages)Dokument48 Seiten(Welding) MIG-MAG Welding Guide - Lincoln Electric (Ebook, 48 Pages)Ahmad Arafa100% (10)

- 29006.eng - Cpi.std - Painting Systems SheetsDokument37 Seiten29006.eng - Cpi.std - Painting Systems SheetsMatteoNoch keine Bewertungen

- Toyota Camry 2006 2011 Body Repair ManualDokument10 SeitenToyota Camry 2006 2011 Body Repair Manualsarah100% (45)

- 1143 Ewf Iiw Diploma August 2013Dokument4 Seiten1143 Ewf Iiw Diploma August 2013Marcus BarberNoch keine Bewertungen

- Aisi 9254 - Spring SteelDokument2 SeitenAisi 9254 - Spring SteelSergio100% (1)

- BSI ListDokument158 SeitenBSI ListAndie AviNoch keine Bewertungen

- Ain Shams Engineering Journal: Yousef R. Alharbi, Aref A. Abadel, Nourhan Elsayed, Ola Mayhoub, Mohamed KohailDokument7 SeitenAin Shams Engineering Journal: Yousef R. Alharbi, Aref A. Abadel, Nourhan Elsayed, Ola Mayhoub, Mohamed KohailMAHESH A VNoch keine Bewertungen

- Astm A781 PDFDokument13 SeitenAstm A781 PDFJeisson GómezNoch keine Bewertungen

- Norma Rejillas Tránsito Vehicular - ANSI NAAMM MBG532-00Dokument75 SeitenNorma Rejillas Tránsito Vehicular - ANSI NAAMM MBG532-00JuanNoch keine Bewertungen

- Parts Manuals Mega PDFDokument52 SeitenParts Manuals Mega PDFCepeda Arancibia Alejandro Pedro100% (1)

- Pipe Wall THK Calc For External PressureDokument2 SeitenPipe Wall THK Calc For External PressurektejankarNoch keine Bewertungen

- Avinash PanchalDokument92 SeitenAvinash PanchalDhyey KalariyaNoch keine Bewertungen

- BS2789 Grade 600-3 SG Iron: Form of SupplyDokument2 SeitenBS2789 Grade 600-3 SG Iron: Form of SupplySama UmateNoch keine Bewertungen

- Instruction Manual ELOTOP 502-EnDokument46 SeitenInstruction Manual ELOTOP 502-EnEmigdio PoloNoch keine Bewertungen

- Metallurgy-Investigatory Project PDFDokument20 SeitenMetallurgy-Investigatory Project PDFAbhishek yadav80% (5)

- Piping Study Guide ASME Codes Standards MaterialsDokument15 SeitenPiping Study Guide ASME Codes Standards MaterialsnandajntuNoch keine Bewertungen

- Chinese Standards On Steel Materials-1Dokument3 SeitenChinese Standards On Steel Materials-1mesmerize59100% (2)

- BS en ISO 2063-2005. Thermal Spraying. Metallic and Other Inorganic Coatings. Zinc, Aluminium and Their AlloysDokument22 SeitenBS en ISO 2063-2005. Thermal Spraying. Metallic and Other Inorganic Coatings. Zinc, Aluminium and Their AlloysStephen LeighNoch keine Bewertungen

- MSM Lab ManualDokument31 SeitenMSM Lab Manualprashant patilNoch keine Bewertungen

- Din Data 401 PDFDokument524 SeitenDin Data 401 PDFamit gajbhiye100% (2)

- 6-79-0015 Rev 1Dokument12 Seiten6-79-0015 Rev 1abhishek0% (1)

- Engg Materials Lab Manual Kle UniveristyDokument42 SeitenEngg Materials Lab Manual Kle UniveristysimalaraviNoch keine Bewertungen

- Astm A276Dokument7 SeitenAstm A276Joffre ValladaresNoch keine Bewertungen

- HDS Benefits From Plate Heat ExchangersDokument6 SeitenHDS Benefits From Plate Heat Exchangerssaleh4060Noch keine Bewertungen

- Sa-Ra Hardware CatalogDokument132 SeitenSa-Ra Hardware CatalogGunuzNoch keine Bewertungen

- Steel Grades Equivalence TableDokument16 SeitenSteel Grades Equivalence Tabletwintwinkai100% (3)