Das könnte Ihnen auch gefallen

- Minor Project Report On Mild Steel BarsDokument22 SeitenMinor Project Report On Mild Steel BarsPawan KumarNoch keine Bewertungen

- Application Form For BusinessesDokument1 SeiteApplication Form For Businessesentabs20160% (1)

- Met Smart Plus BrochureDokument5 SeitenMet Smart Plus BrochurenivasiNoch keine Bewertungen

- Electric Vehicles in IndiaDokument24 SeitenElectric Vehicles in Indiabunny1006100% (5)

- Pangasinan State University: Student Profile FormDokument1 SeitePangasinan State University: Student Profile Formroger quinitoNoch keine Bewertungen

- SBI LIFE INSURANCE - Smart Scholar Brochure V1Dokument16 SeitenSBI LIFE INSURANCE - Smart Scholar Brochure V1Babujee K.NNoch keine Bewertungen

- SBI LIFE INSURANCE - Smart Wealth Brochure New VersionDokument12 SeitenSBI LIFE INSURANCE - Smart Wealth Brochure New VersionBabujee K.NNoch keine Bewertungen

- Kotak Endowment PlanDokument2 SeitenKotak Endowment PlanMichael GreenNoch keine Bewertungen

- Savings Assurance PlanDokument1 SeiteSavings Assurance Planrajeshdubey7Noch keine Bewertungen

- Assurance PlanDokument1 SeiteAssurance Planswetaagarwal2706Noch keine Bewertungen

- Ko Tak Capital Multiplier PlanDokument2 SeitenKo Tak Capital Multiplier PlanemailtotesttestNoch keine Bewertungen

- Key Features Document - Aviva I LifeDokument4 SeitenKey Features Document - Aviva I LifeSonisx SintuNoch keine Bewertungen

- Life Partner Plus Pay Endowment To Age 75 NewDokument6 SeitenLife Partner Plus Pay Endowment To Age 75 NewshamaritesNoch keine Bewertungen

- Life Stay Smart Plan BrochureDokument2 SeitenLife Stay Smart Plan BrochureBadi SudhakaranNoch keine Bewertungen

- LIC's New One Year Renewal Group Term Assurance Plan - IDokument3 SeitenLIC's New One Year Renewal Group Term Assurance Plan - Ilove05kumar05Noch keine Bewertungen

- Guaranteed Return PlanDokument2 SeitenGuaranteed Return PlanShikha ShuklaNoch keine Bewertungen

- Sales Brochure LIC GCLIDokument5 SeitenSales Brochure LIC GCLIRKNoch keine Bewertungen

- Saral Shield Brochure New Version - SBI Life InsuranceDokument8 SeitenSaral Shield Brochure New Version - SBI Life InsuranceBabujee K.NNoch keine Bewertungen

- Ko Tak Term PlanDokument8 SeitenKo Tak Term Plansarvesh.bhartiNoch keine Bewertungen

- Super Cash GainDokument2 SeitenSuper Cash GainElangovan PurushothamanNoch keine Bewertungen

- Preferred Term Plan: Financial Protection For Your Loved Ones. AssuredDokument7 SeitenPreferred Term Plan: Financial Protection For Your Loved Ones. AssuredpankajzapNoch keine Bewertungen

- Sales Brochure - LIC S New Children S Money Back PlanDokument11 SeitenSales Brochure - LIC S New Children S Money Back Planamit_saxena_10Noch keine Bewertungen

- Kotak Money Back PlanDokument2 SeitenKotak Money Back PlanRupran RaiNoch keine Bewertungen

- KFD U39Dokument3 SeitenKFD U39mniarunNoch keine Bewertungen

- Term Insurance - Smart Shield Brochure New Version - SBI Life InsuranceDokument16 SeitenTerm Insurance - Smart Shield Brochure New Version - SBI Life InsuranceBabujee K.NNoch keine Bewertungen

- APIP BrochureDokument2 SeitenAPIP Brochurearpitnigam21Noch keine Bewertungen

- Aviva I-Growth BrochureDokument1 SeiteAviva I-Growth BrochureVarun SharmaNoch keine Bewertungen

- LIC - Jeevan Labh - Brochure - 9 Inch X 8 Inch - EngDokument13 SeitenLIC - Jeevan Labh - Brochure - 9 Inch X 8 Inch - Engnakka_rajeevNoch keine Bewertungen

- Ilife BrochureDokument1 SeiteIlife BrochureSudhakar GanjikuntaNoch keine Bewertungen

- Ko Tak Preferred Term PlanDokument7 SeitenKo Tak Preferred Term PlanvtanmaynNoch keine Bewertungen

- Kotak Complete Cover Group PlanDokument7 SeitenKotak Complete Cover Group PlanGens GeorgeNoch keine Bewertungen

- Metlife Group Accident Death Benefit Plus Rider - Sales Literature - tcm47-66271Dokument4 SeitenMetlife Group Accident Death Benefit Plus Rider - Sales Literature - tcm47-66271Amit PrasadNoch keine Bewertungen

- Kotak Money Back PlanDokument2 SeitenKotak Money Back PlanDriptendu MaitiNoch keine Bewertungen

- SBI LIFE INSURANCE - GrameenBima BrochureDokument2 SeitenSBI LIFE INSURANCE - GrameenBima BrochureBabujee K.N100% (1)

- Reliance Group Credit Shield Plan: Security, Guaranteed!Dokument6 SeitenReliance Group Credit Shield Plan: Security, Guaranteed!Mahipal YadavNoch keine Bewertungen

- Super Endowment BrochureDokument13 SeitenSuper Endowment BrochuremiteshtakeNoch keine Bewertungen

- Sales - Brochure - LIC S New Money Back 25 Yrs PlanDokument11 SeitenSales - Brochure - LIC S New Money Back 25 Yrs PlanShubham PandeyNoch keine Bewertungen

- HDFC Click2protect Plus BrochureDokument8 SeitenHDFC Click2protect Plus Brochurethirudan29Noch keine Bewertungen

- Shriram Extra Insurance Cover Rider (UIN:128B009V01)Dokument4 SeitenShriram Extra Insurance Cover Rider (UIN:128B009V01)Romil TiwariNoch keine Bewertungen

- 831 J Sangam IntroDokument6 Seiten831 J Sangam IntroJames WilliamsNoch keine Bewertungen

- I Don't Want To Postpone My Loved Ones' Aspirations: Bharti AXA Life Secure Income PlanDokument15 SeitenI Don't Want To Postpone My Loved Ones' Aspirations: Bharti AXA Life Secure Income PlanSandhya AgrawalNoch keine Bewertungen

- AR Educare Advantage Insurance Plan 5 May 2014Dokument6 SeitenAR Educare Advantage Insurance Plan 5 May 2014ÌmřańNoch keine Bewertungen

- Lic Brochure 917 Single Endoment Plan 2021Dokument12 SeitenLic Brochure 917 Single Endoment Plan 2021राजकुमार पटेल स्वदेशी प्रचारकNoch keine Bewertungen

- Addar ShilaDokument16 SeitenAddar ShilaK M Reddy ReddyNoch keine Bewertungen

- Lic Leaflet Endoment Plan4 5x8 Inches WXH NewDokument16 SeitenLic Leaflet Endoment Plan4 5x8 Inches WXH NewVishal 777Noch keine Bewertungen

- LIC PM Vaya Vandana YojanaDokument6 SeitenLIC PM Vaya Vandana YojanaShaji MathewNoch keine Bewertungen

- Lic Leaflet Jeevan Anand 4 5x8 Inches WXH DEC 2020Dokument16 SeitenLic Leaflet Jeevan Anand 4 5x8 Inches WXH DEC 2020bantwal_venkateshNoch keine Bewertungen

- Benefits:: (A Non-Linked, Participating, Limited Premium, Individual, Life Assurance Savings Plan)Dokument11 SeitenBenefits:: (A Non-Linked, Participating, Limited Premium, Individual, Life Assurance Savings Plan)coolestkasinovaNoch keine Bewertungen

- Sales Brochure LIC S Single Premium Endowment PlanDokument9 SeitenSales Brochure LIC S Single Premium Endowment Plansantosh kumarNoch keine Bewertungen

- I Secure More BrochureDokument2 SeitenI Secure More BrochureAnand RajgopalNoch keine Bewertungen

- Aviva Life InsuranceDokument3 SeitenAviva Life InsuranceumashankarsinghNoch keine Bewertungen

- 934 Sales Brochure Jeevan TarunDokument16 Seiten934 Sales Brochure Jeevan TarunRV Ranveer SharmaNoch keine Bewertungen

- Lic Market Plus IDokument8 SeitenLic Market Plus Ianpuselvi125Noch keine Bewertungen

- A Nu RagDokument9 SeitenA Nu RagHarish ChandNoch keine Bewertungen

- Ko Tak Capital Multiplier PlanDokument2 SeitenKo Tak Capital Multiplier PlanMeeta AnandNoch keine Bewertungen

- Contact Your Agent/Branch or Visit Our Website WWW - Licindia.in or SMS YOUR CITY NAME TO 56767474 (Eg. MUMBAI)Dokument12 SeitenContact Your Agent/Branch or Visit Our Website WWW - Licindia.in or SMS YOUR CITY NAME TO 56767474 (Eg. MUMBAI)RustyNoch keine Bewertungen

- HDFC SL CrestDokument4 SeitenHDFC SL CrestPreetinder Singh BrarNoch keine Bewertungen

- Sales Brochure LIC S Jeevan Lakshya PDFDokument11 SeitenSales Brochure LIC S Jeevan Lakshya PDFamit_saxena_10Noch keine Bewertungen

- Now I Can Secure My Family's Future With Just A Click.: Bharti AXA Life ProtectDokument12 SeitenNow I Can Secure My Family's Future With Just A Click.: Bharti AXA Life ProtectVenkatram Reddy KamasaniNoch keine Bewertungen

- Smart Platina Plus Brochure - BRDokument3 SeitenSmart Platina Plus Brochure - BRSumit RpNoch keine Bewertungen

- Jeevan Anurag: Assured BenefitDokument10 SeitenJeevan Anurag: Assured BenefitMandheer ChitnavisNoch keine Bewertungen

- 933 Sales Brochure Jeevan LakshyaDokument16 Seiten933 Sales Brochure Jeevan LakshyaPREM MURUGANNoch keine Bewertungen

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterVon EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNoch keine Bewertungen

- SBI LIFE INSURANCE - GrameenBima BrochureDokument2 SeitenSBI LIFE INSURANCE - GrameenBima BrochureBabujee K.N100% (1)

- Saral Pension Brochure English - SBI Life InsuranceDokument8 SeitenSaral Pension Brochure English - SBI Life InsuranceBabujee K.NNoch keine Bewertungen

- SBI LIFE INSURANCE - Retire Smart BrochureDokument12 SeitenSBI LIFE INSURANCE - Retire Smart BrochureBabujee K.N0% (1)

- Investment Land Sale at Valapuram 8124248679Dokument1 SeiteInvestment Land Sale at Valapuram 8124248679Babujee K.NNoch keine Bewertungen

- Land Sale Below GOVERNMENT GUIDELINE VALUE at Mosur Railway Station Call Babujee 8124248679Dokument1 SeiteLand Sale Below GOVERNMENT GUIDELINE VALUE at Mosur Railway Station Call Babujee 8124248679Babujee K.NNoch keine Bewertungen

- Investment Land Sale at Sriperumbudur Valapuram 8124248679Dokument2 SeitenInvestment Land Sale at Sriperumbudur Valapuram 8124248679Babujee K.NNoch keine Bewertungen

- Term Insurance - Smart Shield Brochure New Version - SBI Life InsuranceDokument16 SeitenTerm Insurance - Smart Shield Brochure New Version - SBI Life InsuranceBabujee K.NNoch keine Bewertungen

- Shubh Nivesh Brochure New Version - SBI Life InsuranceDokument12 SeitenShubh Nivesh Brochure New Version - SBI Life InsuranceBabujee K.NNoch keine Bewertungen

- HARSHAM Gated Community Luxury Flats at Affordable Price at Pallavaram 200 Feet Road Call 8124248679Dokument7 SeitenHARSHAM Gated Community Luxury Flats at Affordable Price at Pallavaram 200 Feet Road Call 8124248679Babujee K.NNoch keine Bewertungen

- SBI LIFE INSURANCE - Retire Smart BrochureDokument12 SeitenSBI LIFE INSURANCE - Retire Smart BrochureBabujee K.N0% (1)

- Saral Shield Brochure New Version - SBI Life InsuranceDokument8 SeitenSaral Shield Brochure New Version - SBI Life InsuranceBabujee K.NNoch keine Bewertungen

- Saral Pension Brochure English - SBI Life InsuranceDokument8 SeitenSaral Pension Brochure English - SBI Life InsuranceBabujee K.NNoch keine Bewertungen

- Eshield Brochure New Ver - SBI LIFE InsuranceDokument8 SeitenEshield Brochure New Ver - SBI LIFE InsuranceBabujee K.NNoch keine Bewertungen

- For Billing Enquiry Visit Https://selfcare - Tikona.inDokument2 SeitenFor Billing Enquiry Visit Https://selfcare - Tikona.inVivek Jain100% (1)

- Guingona V City FiscalDokument1 SeiteGuingona V City FiscalFaye Jennifer Pascua PerezNoch keine Bewertungen

- CRUDIFY - The Best Crude Oil Intraday Trading StrategyDokument11 SeitenCRUDIFY - The Best Crude Oil Intraday Trading StrategyRajeswaran DhanagopalanNoch keine Bewertungen

- Long Examination Cash Set ADokument3 SeitenLong Examination Cash Set AprechuteNoch keine Bewertungen

- Uti Mutual FundDokument23 SeitenUti Mutual Fundgeethrk120% (1)

- MIB, Semester 1 Accounting and Finance Luvnica Rastogi: Amity International Business SchoolDokument25 SeitenMIB, Semester 1 Accounting and Finance Luvnica Rastogi: Amity International Business SchoolRatika GuptaNoch keine Bewertungen

- Agricultural and Rural DevelopmentDokument6 SeitenAgricultural and Rural DevelopmentArchie TonogNoch keine Bewertungen

- Asst. Commissioner (U/T), HOSHIARPUR, PUNJABDokument6 SeitenAsst. Commissioner (U/T), HOSHIARPUR, PUNJABpvbadhranNoch keine Bewertungen

- Ts English Course Tution Payment Sheet Ts English Course Tution Payment SheetDokument2 SeitenTs English Course Tution Payment Sheet Ts English Course Tution Payment Sheetmuchlis rahmatNoch keine Bewertungen

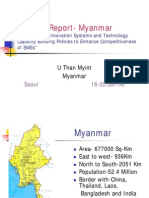

- Country Report MyanmarDokument34 SeitenCountry Report MyanmarAchit zaw tun myatNoch keine Bewertungen

- AN Analysis of Impact of Crude Oil Prices On Indian EconomyDokument28 SeitenAN Analysis of Impact of Crude Oil Prices On Indian EconomySrijan SaxenaNoch keine Bewertungen

- 1 Industrial Revolution PDFDokument14 Seiten1 Industrial Revolution PDFKiaraNoch keine Bewertungen

- 6 Stocks Double Investors' Wealth Since Last Ganesh ChaturthiDokument8 Seiten6 Stocks Double Investors' Wealth Since Last Ganesh ChaturthiJayaprakash MuthuvatNoch keine Bewertungen

- SSUSH 17: The Student Will Analyze The Causes and Consequences of The Great DepressionDokument18 SeitenSSUSH 17: The Student Will Analyze The Causes and Consequences of The Great DepressionDewanshu GuptaNoch keine Bewertungen

- Gap Analysis of IRCTCDokument37 SeitenGap Analysis of IRCTCHitesh SethiNoch keine Bewertungen

- 0040 Jugal BakersDokument3 Seiten0040 Jugal BakersVarghese PDNoch keine Bewertungen

- Ethiopia Public Debt Portfolio Analysis No 21 - 2019-20Dokument82 SeitenEthiopia Public Debt Portfolio Analysis No 21 - 2019-20Mk FisihaNoch keine Bewertungen

- Pension Plan Reporting of Foreign Bank and Financial AccountsDokument3 SeitenPension Plan Reporting of Foreign Bank and Financial AccountsCorey Slagle100% (1)

- Bir Hisar Reject Kharif 2022 Insured PolicyDokument2 SeitenBir Hisar Reject Kharif 2022 Insured PolicyJ StudioNoch keine Bewertungen

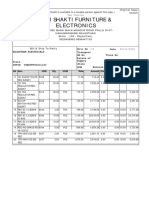

- Shri Shakti Furniture & Electronics: Credit OrginalDokument1 SeiteShri Shakti Furniture & Electronics: Credit OrginalRahul BansalNoch keine Bewertungen

- The Great DepressionDokument15 SeitenThe Great DepressionRAahvi RAahnaNoch keine Bewertungen

- PEZA Reportorial RequirementsDokument4 SeitenPEZA Reportorial RequirementsMV FadsNoch keine Bewertungen

- Welcome To Indian Railway Passenger Reservation EnquiryDokument2 SeitenWelcome To Indian Railway Passenger Reservation EnquiryChhaviNoch keine Bewertungen

- Acctg 303Dokument9 SeitenAcctg 303Anonymous IsEZYR1Noch keine Bewertungen

- Ray Dalio - The CycleDokument20 SeitenRay Dalio - The CyclePhương LộcNoch keine Bewertungen

- DCPD Editorial Ebook Till Sep 29, 19Dokument181 SeitenDCPD Editorial Ebook Till Sep 29, 19segnumutraNoch keine Bewertungen