Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Inclusion and Exclusion of GIDokument14 SeitenInclusion and Exclusion of GIRoxanne Dela Cruz100% (1)

- Gida - Industrial Plot Allotment Scheme - 2020Dokument4 SeitenGida - Industrial Plot Allotment Scheme - 2020VIJAY PAREEKNoch keine Bewertungen

- Wholesale Credit AppDokument3 SeitenWholesale Credit AppReload GamingNoch keine Bewertungen

- Binder1 PDFDokument5 SeitenBinder1 PDFSaad Raza KhanNoch keine Bewertungen

- Bangladesh's Cross Border Transaction in Chinese RMBDokument3 SeitenBangladesh's Cross Border Transaction in Chinese RMBMohammad Shahjahan SiddiquiNoch keine Bewertungen

- How To Upgrade Bangladesh's Banking AlmanacDokument4 SeitenHow To Upgrade Bangladesh's Banking AlmanacMohammad Shahjahan SiddiquiNoch keine Bewertungen

- IMF and Reforms in BangladeshDokument4 SeitenIMF and Reforms in BangladeshMohammad Shahjahan SiddiquiNoch keine Bewertungen

- How Insiders Are Manipulating Dollar RatesDokument4 SeitenHow Insiders Are Manipulating Dollar RatesMohammad Shahjahan SiddiquiNoch keine Bewertungen

- FTAs Instrumental To Sustained GrowthDokument4 SeitenFTAs Instrumental To Sustained GrowthMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Access To Finance For The Informal SectorDokument5 SeitenAccess To Finance For The Informal SectorMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Evaluation of Import Policy Order 2021-2024Dokument6 SeitenEvaluation of Import Policy Order 2021-2024Mohammad Shahjahan SiddiquiNoch keine Bewertungen

- Ongoing War On SemiconductorsDokument3 SeitenOngoing War On SemiconductorsMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Evaluation of Bangladesh's Data Protection BillDokument4 SeitenEvaluation of Bangladesh's Data Protection BillMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Chinese Dual Circulation Economic PolicyDokument4 SeitenChinese Dual Circulation Economic PolicyMohammad Shahjahan SiddiquiNoch keine Bewertungen

- About Doing Business' ReportDokument4 SeitenAbout Doing Business' ReportMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Bangladesh Needs Rules On Odourised LPGDokument2 SeitenBangladesh Needs Rules On Odourised LPGMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Some Thoughts On Pension SchemeDokument4 SeitenSome Thoughts On Pension SchemeMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Bangladesh Bank's Rules of Export Documents Require An AmendmentDokument3 SeitenBangladesh Bank's Rules of Export Documents Require An AmendmentMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Ad Free Channel Ends Unfair Privileges To Overseas ManufacturersDokument4 SeitenAd Free Channel Ends Unfair Privileges To Overseas ManufacturersMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Pandemic Recession and Employment CrisisDokument4 SeitenPandemic Recession and Employment CrisisMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Bangladesh - Last Option of Relocation of Chinese FactoryDokument4 SeitenBangladesh - Last Option of Relocation of Chinese FactoryMohammad Shahjahan SiddiquiNoch keine Bewertungen

- HSIA Needs Off-Doc WarehouseDokument4 SeitenHSIA Needs Off-Doc WarehouseMohammad Shahjahan SiddiquiNoch keine Bewertungen

- The Legal Impacts of The Coronavirus On RMG ContractsDokument4 SeitenThe Legal Impacts of The Coronavirus On RMG ContractsMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Spillover of Technology and CompetitivenessDokument4 SeitenSpillover of Technology and CompetitivenessMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Need For A Payment System ActDokument4 SeitenNeed For A Payment System ActMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Post Clearance Customs AuditDokument3 SeitenPost Clearance Customs AuditMohammad Shahjahan SiddiquiNoch keine Bewertungen

- The Inflow and Outflow of CapitalDokument4 SeitenThe Inflow and Outflow of CapitalMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Onions, Syndicates and PricesDokument3 SeitenOnions, Syndicates and PricesMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Transfer of Ownership of Export BillDokument3 SeitenTransfer of Ownership of Export BillMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Import Tax On Onion Is The Best SolutionDokument4 SeitenImport Tax On Onion Is The Best SolutionMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Weaknesses in SME Financing PolicyDokument4 SeitenWeaknesses in SME Financing PolicyMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Education To Develop Creativity and Analysing AbilityDokument4 SeitenEducation To Develop Creativity and Analysing AbilityMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Negative List For FDI in China and BangladeshDokument4 SeitenNegative List For FDI in China and BangladeshMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Bangladesh Media Busy With India's Decision About RCEPDokument3 SeitenBangladesh Media Busy With India's Decision About RCEPMohammad Shahjahan SiddiquiNoch keine Bewertungen

- Pan-Aarca9082e Pan-Aarca9082eDokument4 SeitenPan-Aarca9082e Pan-Aarca9082eDilip KumarNoch keine Bewertungen

- 00131369Dokument5 Seiten00131369Omprakash PipasaNoch keine Bewertungen

- Foreclosure Letter - 20 - 49 - 45Dokument3 SeitenForeclosure Letter - 20 - 49 - 45Suman KumarNoch keine Bewertungen

- Manila Mandarin Hotels Vs CommissionerDokument2 SeitenManila Mandarin Hotels Vs CommissionerEryl Yu100% (1)

- Lesson 14 Financial Literacy Andrea RDokument2 SeitenLesson 14 Financial Literacy Andrea Rapi-501679979Noch keine Bewertungen

- Local Purchase Order: Amount in WordsDokument1 SeiteLocal Purchase Order: Amount in WordsTina MillerNoch keine Bewertungen

- Exercise DrillDokument6 SeitenExercise DrillAbigail Ann PasiliaoNoch keine Bewertungen

- Case 84 in Re ZialcitaDokument4 SeitenCase 84 in Re ZialcitaAlexis Ailex Villamor Jr.Noch keine Bewertungen

- Country Specific Document XMLv3 Santander BrazilDokument21 SeitenCountry Specific Document XMLv3 Santander BrazilJimmy De la CruzNoch keine Bewertungen

- Fredrickson v. Starbucks CorporationDokument51 SeitenFredrickson v. Starbucks Corporationmary engNoch keine Bewertungen

- 3 Month Deferment Tax Instalment CP204Dokument1 Seite3 Month Deferment Tax Instalment CP204Alaya VirjaNoch keine Bewertungen

- PaypalDokument2 SeitenPaypala.shyamNoch keine Bewertungen

- Panasonic Communications Imaging Corp. v. CIRDokument3 SeitenPanasonic Communications Imaging Corp. v. CIRAbigayle RecioNoch keine Bewertungen

- PolicyDokument3 SeitenPolicyBhavsmeetforeverNoch keine Bewertungen

- BM2008I002097905Dokument6 SeitenBM2008I002097905Nishant MeghwalNoch keine Bewertungen

- Hire Purchase SystemDokument5 SeitenHire Purchase SystemMasoom Farishtah0% (1)

- Leed's Invoice # V10122828Dokument2 SeitenLeed's Invoice # V10122828Anil KumarNoch keine Bewertungen

- Invoice20200845240058CBN4514017082045 24005 8Dokument1 SeiteInvoice20200845240058CBN4514017082045 24005 8Ayu MangNoch keine Bewertungen

- Mr. Shyam Singh's bank account statement and detailsDokument3 SeitenMr. Shyam Singh's bank account statement and detailsShyamNoch keine Bewertungen

- Impact of Plastic Money On Paper MoneyDokument7 SeitenImpact of Plastic Money On Paper Moneymustafeez88% (8)

- Consumer Behaviour in The Credit Card MarketDokument9 SeitenConsumer Behaviour in The Credit Card Marketmrabie2004Noch keine Bewertungen

- Introduction to Plastic MoneyDokument70 SeitenIntroduction to Plastic MoneyParm Sidhu100% (12)

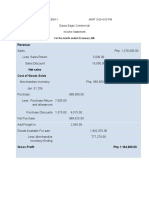

- Davao Eagle Commercial January Income StatementDokument6 SeitenDavao Eagle Commercial January Income Statementablay logeneNoch keine Bewertungen

- BSNL Telephone Bill DetailsDokument1 SeiteBSNL Telephone Bill DetailsSri DarNoch keine Bewertungen

- Tax Invoice: 36AADCM3491M1Z2 30AAACC6253G1Z6Dokument1 SeiteTax Invoice: 36AADCM3491M1Z2 30AAACC6253G1Z6VIDHI JAINENDRASINH RANANoch keine Bewertungen

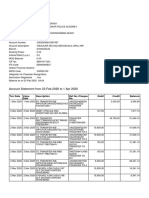

- Account Statement InsightsDokument14 SeitenAccount Statement InsightspoplolyNoch keine Bewertungen