Das könnte Ihnen auch gefallen

- A Few Examples of How A Different Margin Could Affect Your Transaction FollowDokument6 SeitenA Few Examples of How A Different Margin Could Affect Your Transaction FollowAhmad Fauzi MehatNoch keine Bewertungen

- Authorized Letter For Verification of Fund-RMBDokument2 SeitenAuthorized Letter For Verification of Fund-RMBAhmad Fauzi MehatNoch keine Bewertungen

- U.S. DOT Federal Transit Administration Best Practices Procurement ManualDokument673 SeitenU.S. DOT Federal Transit Administration Best Practices Procurement ManualAhmad Fauzi MehatNoch keine Bewertungen

- Suggested End of Chapter 5 SolutionsDokument8 SeitenSuggested End of Chapter 5 SolutionsAhmad Fauzi MehatNoch keine Bewertungen

- Rentas ModuleDokument1 SeiteRentas ModuleAhmad Fauzi MehatNoch keine Bewertungen

- Exchange Control RulesDokument14 SeitenExchange Control RulesAhmad Fauzi Mehat100% (1)

- Bond Pricing in The MarketDokument53 SeitenBond Pricing in The MarketAhmad Fauzi MehatNoch keine Bewertungen

- Roll On or Roll of Process FlowsDokument11 SeitenRoll On or Roll of Process FlowsAhmad Fauzi MehatNoch keine Bewertungen

- Valuation of Debt Instruments: Debt Securities Are Government Securities (Government Bonds, Government BillsDokument13 SeitenValuation of Debt Instruments: Debt Securities Are Government Securities (Government Bonds, Government BillsJoslin FernandesNoch keine Bewertungen

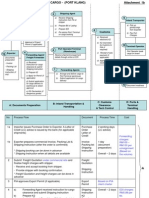

- Export + Import Process Flow - Break Bulk Cargo 27072010Dokument11 SeitenExport + Import Process Flow - Break Bulk Cargo 27072010Ahmad Fauzi Mehat100% (1)

- Welcome To The Gold Guidelines: Page 1 of 9Dokument9 SeitenWelcome To The Gold Guidelines: Page 1 of 9Ahmad Fauzi MehatNoch keine Bewertungen

- Malaysia Haulage Charges (Base On Point-Butterworth, Penang)Dokument2 SeitenMalaysia Haulage Charges (Base On Point-Butterworth, Penang)Ahmad Fauzi MehatNoch keine Bewertungen

- Contract c8Dokument9 SeitenContract c8Ahmad Fauzi MehatNoch keine Bewertungen

- World Bank Report FinalDokument76 SeitenWorld Bank Report FinalAhmad Fauzi MehatNoch keine Bewertungen

- Dry Bulk Cargo - (Import and Export)Dokument12 SeitenDry Bulk Cargo - (Import and Export)Ahmad Fauzi Mehat100% (1)

- BG and SBLCDokument1 SeiteBG and SBLCKwadwo AsaseNoch keine Bewertungen

- Mt100 To 199 (Customer Payments)Dokument286 SeitenMt100 To 199 (Customer Payments)Perez CorazaNoch keine Bewertungen

- World Financial Infrastructure and MoneyDokument129 SeitenWorld Financial Infrastructure and MoneyAhmad Fauzi MehatNoch keine Bewertungen

- Swift Standards Category 4 Collections Cash LettersDokument128 SeitenSwift Standards Category 4 Collections Cash LettersAhmad Fauzi MehatNoch keine Bewertungen

- Swift Standards Category 6 Treasury Markets Precious Metals MT600 MT699Dokument103 SeitenSwift Standards Category 6 Treasury Markets Precious Metals MT600 MT699Ahmad Fauzi Mehat100% (1)

- Samad and Gardner and Cook - Islamic Banking and Finance PDFDokument18 SeitenSamad and Gardner and Cook - Islamic Banking and Finance PDFAhmad Fauzi MehatNoch keine Bewertungen

- Bullion Coins BookletDokument17 SeitenBullion Coins BookletAhmad Fauzi MehatNoch keine Bewertungen

- Types of Credit Instruments & Its FeaturesDokument22 SeitenTypes of Credit Instruments & Its Featuresninpra94% (18)

- 30 Currencies Including The G7Dokument6 Seiten30 Currencies Including The G7Ahmad Fauzi MehatNoch keine Bewertungen

- Swift Standards Category 7 Documentary Credits & GuaranteesDokument209 SeitenSwift Standards Category 7 Documentary Credits & GuaranteesMEGHANALOKSHANoch keine Bewertungen

- Swift Standards Category 7 Documentary Credits & GuaranteesDokument209 SeitenSwift Standards Category 7 Documentary Credits & GuaranteesMEGHANALOKSHANoch keine Bewertungen

- Bank GuaranteeDokument6 SeitenBank GuaranteeAhmad Fauzi MehatNoch keine Bewertungen

- Financial StatementDokument6 SeitenFinancial StatementAhmad Fauzi MehatNoch keine Bewertungen

- Banking-Theory-Law and PracticeDokument151 SeitenBanking-Theory-Law and PracticeAhmad Fauzi MehatNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Certificate of Indigency (Emergency Philhealth)Dokument3 SeitenCertificate of Indigency (Emergency Philhealth)Barangay AmasNoch keine Bewertungen

- A4V Procedure - Trvth's Presentation of SFsDokument22 SeitenA4V Procedure - Trvth's Presentation of SFsBob Hurt100% (7)

- 06Dokument9 Seiten06Shubham RawatNoch keine Bewertungen

- Hugh Hendry Eclectica Nov09Dokument8 SeitenHugh Hendry Eclectica Nov09marketfolly.comNoch keine Bewertungen

- Statement 25197479 EUR 2024-02-02 2024-03-03Dokument4 SeitenStatement 25197479 EUR 2024-02-02 2024-03-03Gabriel BuitiNoch keine Bewertungen

- Indian Currency MarketDokument15 SeitenIndian Currency MarketSneha PatelNoch keine Bewertungen

- PSLE Maths Challenging Word Problems Set02Dokument10 SeitenPSLE Maths Challenging Word Problems Set02Smith100% (1)

- Macroeconomics 10th Edition Colander Test Bank Full Chapter PDFDokument66 SeitenMacroeconomics 10th Edition Colander Test Bank Full Chapter PDFcarlarodriquezajbns100% (10)

- Vitalik Buterin BiographyDokument3 SeitenVitalik Buterin BiographywilsonlariosNoch keine Bewertungen

- Value of Taxable Supply - Transaction ValueDokument36 SeitenValue of Taxable Supply - Transaction ValueArun JyothiNoch keine Bewertungen

- Oracle FLEXCUBE Universal Banking Primer - CoreDokument23 SeitenOracle FLEXCUBE Universal Banking Primer - CoremuruganandhanNoch keine Bewertungen

- Three Essays On Macroeconomic Management 2008Dokument214 SeitenThree Essays On Macroeconomic Management 2008Chan RithNoch keine Bewertungen

- Worded Problems: - Number - Coin - Age - Work - MixtureDokument37 SeitenWorded Problems: - Number - Coin - Age - Work - Mixturearnel cabesasNoch keine Bewertungen

- Tanzania civic education quizDokument2 SeitenTanzania civic education quizKANDONGA FARAJANoch keine Bewertungen

- Bank Abbreviations PDFDokument6 SeitenBank Abbreviations PDFVineeth VivekanandanNoch keine Bewertungen

- Zambia Kwacha Currency Rebasing Brochure BarclaysDokument12 SeitenZambia Kwacha Currency Rebasing Brochure BarclaysBen MusimaneNoch keine Bewertungen

- Guido Candela, Paolo Figini Auth. The Economics of Tourism Destinations PDFDokument626 SeitenGuido Candela, Paolo Figini Auth. The Economics of Tourism Destinations PDFMelania PaceNoch keine Bewertungen

- Janata BankDokument53 SeitenJanata BankAriful Islam FahimNoch keine Bewertungen

- Study of Impacts of Demonetization in IndiaDokument46 SeitenStudy of Impacts of Demonetization in IndiaSoumya RanjanNoch keine Bewertungen

- Microeconomics - Theory Through ApplicationsDokument828 SeitenMicroeconomics - Theory Through ApplicationsRunal Bhanamgi100% (1)

- ZTYRDokument6 SeitenZTYRshikhar singhNoch keine Bewertungen

- CyberPunk 2020 - Unofficial - Magazine - EdgeRunner Vol2 Issue01Dokument14 SeitenCyberPunk 2020 - Unofficial - Magazine - EdgeRunner Vol2 Issue01llokuniyahooesNoch keine Bewertungen

- Dinar To Naira - Google SearchDokument1 SeiteDinar To Naira - Google SearchJenna CarolineNoch keine Bewertungen

- Chapter 3 - Money and Credit: CBSE Notes Class 10 Social Science EconomicsDokument3 SeitenChapter 3 - Money and Credit: CBSE Notes Class 10 Social Science EconomicsWIN FACTSNoch keine Bewertungen

- Gold and Silver First Tetrarchic Issues From The Mint of Alexandria / D. Scott VanHornDokument33 SeitenGold and Silver First Tetrarchic Issues From The Mint of Alexandria / D. Scott VanHornDigital Library Numis (DLN)Noch keine Bewertungen

- Brazil's currency slides to new lowDokument2 SeitenBrazil's currency slides to new lowFunded FXNoch keine Bewertungen

- Cash Count SheetDokument5.468 SeitenCash Count SheetchrischuwaNoch keine Bewertungen

- Unit 1 PPT 1Dokument35 SeitenUnit 1 PPT 1Shristi SinhaNoch keine Bewertungen

- Lawful Money Defined: What It Is and How It Differs From Fiat CurrencyDokument4 SeitenLawful Money Defined: What It Is and How It Differs From Fiat CurrencyLedoNoch keine Bewertungen

- For Individuals and Sole Proprietorship (BALH)Dokument6 SeitenFor Individuals and Sole Proprietorship (BALH)Ghulam Hyder100% (1)