Das könnte Ihnen auch gefallen

- 0b.addendum and Corrigendum 5Dokument22 Seiten0b.addendum and Corrigendum 5Anonymous ufMAGXcskMNoch keine Bewertungen

- Status of Engineering /inspectionDokument1 SeiteStatus of Engineering /inspectionAnonymous ufMAGXcskMNoch keine Bewertungen

- ATTSDokument1 SeiteATTSAnonymous ufMAGXcskMNoch keine Bewertungen

- Distribution Side: The Transformers in Distribution Side Are Step Down TransformersDokument1 SeiteDistribution Side: The Transformers in Distribution Side Are Step Down TransformersAnonymous ufMAGXcskMNoch keine Bewertungen

- Distribution Side: The Transformers in Distribution Side Are Step Down TransformersDokument1 SeiteDistribution Side: The Transformers in Distribution Side Are Step Down TransformersAnonymous ufMAGXcskMNoch keine Bewertungen

- Tr. ConnectionsDokument34 SeitenTr. ConnectionsAnonymous ufMAGXcskMNoch keine Bewertungen

- SL No IS No TitleDokument1 SeiteSL No IS No TitleAnonymous ufMAGXcskMNoch keine Bewertungen

- SL No IS No TitleDokument1 SeiteSL No IS No TitleAnonymous ufMAGXcskMNoch keine Bewertungen

- Two Pelton (Vertical Axis) Turbines Used in This Project Whose Installed Capacity Is 16MWDokument1 SeiteTwo Pelton (Vertical Axis) Turbines Used in This Project Whose Installed Capacity Is 16MWAnonymous ufMAGXcskMNoch keine Bewertungen

- SL No IS No TitleDokument1 SeiteSL No IS No TitleAnonymous ufMAGXcskMNoch keine Bewertungen

- Construction Management & Construction Supervision of Main Civilworks of Rahughat Hydroelctric Project (32 MW)Dokument2 SeitenConstruction Management & Construction Supervision of Main Civilworks of Rahughat Hydroelctric Project (32 MW)Anonymous ufMAGXcskMNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Tim Redmer AccountingDokument204 SeitenTim Redmer AccountingDax100% (5)

- FinQuiz - Smart Summary - Study Session 1 - Reading 1Dokument17 SeitenFinQuiz - Smart Summary - Study Session 1 - Reading 1RafaelNoch keine Bewertungen

- Titman CH 09Dokument150 SeitenTitman CH 09Yenyensmile100% (1)

- Apollo Tyres and BKTDokument25 SeitenApollo Tyres and BKTKoushik G Sai100% (1)

- SRCL Research NotesDokument5 SeitenSRCL Research NotesMichael LoebNoch keine Bewertungen

- Deloitte - mini-eminences-DD-Finance-enDokument1 SeiteDeloitte - mini-eminences-DD-Finance-enKumar RitwikNoch keine Bewertungen

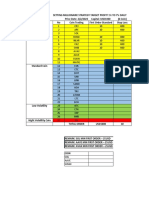

- Valuation of Asian PaintsDokument18 SeitenValuation of Asian Paintsaravindmenonm0% (3)

- Term Paper ID#19020010Dokument23 SeitenTerm Paper ID#19020010Uttam Kumar Ghosh100% (1)

- Thomas Blaisdell CVDokument3 SeitenThomas Blaisdell CVtjNoch keine Bewertungen

- IFM Sports Marketing Surveys - Our BusinessDokument8 SeitenIFM Sports Marketing Surveys - Our Businessmrvicq1982Noch keine Bewertungen

- Juniper Networks - A Sample Strategic Planning AnalysisDokument37 SeitenJuniper Networks - A Sample Strategic Planning AnalysisEly GamboaNoch keine Bewertungen

- Kyc Aml Master Key Module 4Dokument25 SeitenKyc Aml Master Key Module 4prashant pradhan100% (3)

- Chapter 10: Common Stock ValuationDokument7 SeitenChapter 10: Common Stock ValuationJhela HemarNoch keine Bewertungen

- Warren Buffet Value Investing Strategy Toolkit - OverviewDokument37 SeitenWarren Buffet Value Investing Strategy Toolkit - OverviewMaria AngelNoch keine Bewertungen

- @canotes - Ipcc AS BookDokument160 Seiten@canotes - Ipcc AS Booksamartha umbare100% (1)

- Company Acc B.com Sem Iv...Dokument8 SeitenCompany Acc B.com Sem Iv...Sarah ShelbyNoch keine Bewertungen

- Partnership Problems Partnership Problems: Accountancy (La Consolacion College) Accountancy (La Consolacion College)Dokument35 SeitenPartnership Problems Partnership Problems: Accountancy (La Consolacion College) Accountancy (La Consolacion College)MIKASA0% (1)

- Formula Cointech2u Setting Trading 1k To 200k Update 12 04 2023Dokument45 SeitenFormula Cointech2u Setting Trading 1k To 200k Update 12 04 2023AndhikaNoch keine Bewertungen

- IntaccDokument24 SeitenIntaccAngelKate MicabaniNoch keine Bewertungen

- Shahmurad Sugar Mills Limited: 1st Quarterly Results For The Period 1st October 2019 To 31st December, 2019Dokument19 SeitenShahmurad Sugar Mills Limited: 1st Quarterly Results For The Period 1st October 2019 To 31st December, 2019Hira wasiqNoch keine Bewertungen

- PR: Lombard Risk Demonstrates 32% Revenue Grown For 2011Dokument3 SeitenPR: Lombard Risk Demonstrates 32% Revenue Grown For 2011Lombard RiskNoch keine Bewertungen

- RC Equity Research Report Essentials CFA InstituteDokument3 SeitenRC Equity Research Report Essentials CFA InstitutetheakjNoch keine Bewertungen

- Harmonic LOI For InteQ Oct 7 2022Dokument5 SeitenHarmonic LOI For InteQ Oct 7 2022shashankNoch keine Bewertungen

- Merchant Banking Financial Services Two Marks Question BankDokument21 SeitenMerchant Banking Financial Services Two Marks Question BankGanesh Pandian50% (2)

- Frontiers of FinanceDokument236 SeitenFrontiers of Financead9292Noch keine Bewertungen

- 1 1 SLO Service Desc CCDokument18 Seiten1 1 SLO Service Desc CCSiva Kumar RamalingamNoch keine Bewertungen

- Icaew Audit Assurance Questions PDF FreeDokument39 SeitenIcaew Audit Assurance Questions PDF FreeAbdul ToheedNoch keine Bewertungen

- ADR Exam 2020 ABDokument10 SeitenADR Exam 2020 ABDARSHNANoch keine Bewertungen

- Markus Trading PlanDokument3 SeitenMarkus Trading PlanAmarrdiip KumaarrNoch keine Bewertungen

- Nestlé and Alcon-The Value of A ListingDokument6 SeitenNestlé and Alcon-The Value of A ListingRahul KumarNoch keine Bewertungen