Das könnte Ihnen auch gefallen

- CMA II 2016 Study Materials CMA Part 2 MDokument37 SeitenCMA II 2016 Study Materials CMA Part 2 Mkopy brayntNoch keine Bewertungen

- Beat The MarketDokument13 SeitenBeat The Marketquantext100% (3)

- SBI Mutual FundDokument25 SeitenSBI Mutual FundNarendra Singh100% (1)

- Alibaba Company AnalysisDokument47 SeitenAlibaba Company AnalysisAsh100% (1)

- Strategic Control and Corporate Governance: Because Learning Changes EverythingDokument35 SeitenStrategic Control and Corporate Governance: Because Learning Changes EverythingHazim HafizNoch keine Bewertungen

- Customer Satisfaction Survey On BanksDokument32 SeitenCustomer Satisfaction Survey On BanksAnkit Singh81% (21)

- Pairs Trading G GRDokument31 SeitenPairs Trading G GRSrinu BonuNoch keine Bewertungen

- Chapter 12: Leverage and Capital StructureDokument26 SeitenChapter 12: Leverage and Capital Structuredebate ddNoch keine Bewertungen

- Magic Formula Tesed by Paiboon On SETDokument13 SeitenMagic Formula Tesed by Paiboon On SETmytheeNoch keine Bewertungen

- Joint VenturesDokument13 SeitenJoint VenturesNori LolaNoch keine Bewertungen

- Value Investing in ThailandDokument14 SeitenValue Investing in ThailandOhm BussarakulNoch keine Bewertungen

- Fraud Detection and Expected ReturnsDokument53 SeitenFraud Detection and Expected Returnssarah.price19766985Noch keine Bewertungen

- Study of Multiple Year Holding Period Equity Model and Its Application On Stock Price Valuation: With Special Reference To FMCG SectorDokument8 SeitenStudy of Multiple Year Holding Period Equity Model and Its Application On Stock Price Valuation: With Special Reference To FMCG SectorTamalNoch keine Bewertungen

- LR 10 ReportsDokument10 SeitenLR 10 ReportsHari PriyaNoch keine Bewertungen

- Objectives: TITLE: Size and Return A Study On Indian Stock Market COMPANY NAME: SharewealthDokument5 SeitenObjectives: TITLE: Size and Return A Study On Indian Stock Market COMPANY NAME: Sharewealthanon_578178848Noch keine Bewertungen

- Share Price Behaviour-Pre and Post DividendDokument15 SeitenShare Price Behaviour-Pre and Post DividendjazzymastNoch keine Bewertungen

- Review of LiteratureDokument8 SeitenReview of LiteratureChandruNoch keine Bewertungen

- Llorente 2002-ExmDokument43 SeitenLlorente 2002-ExmAndrei Boti FutoNoch keine Bewertungen

- Baker and Wurgler - Market Timing and CSDokument33 SeitenBaker and Wurgler - Market Timing and CSIvana JovanovskaNoch keine Bewertungen

- Are Institutions Momentum Traders?Dokument39 SeitenAre Institutions Momentum Traders?mirando93Noch keine Bewertungen

- Introduction (Muhammad Amin - 1735237)Dokument7 SeitenIntroduction (Muhammad Amin - 1735237)Amin H. HamdaniNoch keine Bewertungen

- Share Price Performance Following Actual Share RepurchasesDokument25 SeitenShare Price Performance Following Actual Share RepurchasesblacksmithMGNoch keine Bewertungen

- 11 Chapter-5Dokument155 Seiten11 Chapter-5Shazaf KhanNoch keine Bewertungen

- Kraft Schwartz 11 WPDokument43 SeitenKraft Schwartz 11 WPSalah AyoubiNoch keine Bewertungen

- Literature Review On Stock Market EfficiencyDokument4 SeitenLiterature Review On Stock Market Efficiencyafmzslnxmqrjom100% (1)

- Research ReportDokument17 SeitenResearch Reportapi-317623686Noch keine Bewertungen

- Do Investors Mistake A Good Company For A Good Investment?Dokument40 SeitenDo Investors Mistake A Good Company For A Good Investment?CristianNoch keine Bewertungen

- Chapter 2Dokument52 SeitenChapter 2Alok SinghNoch keine Bewertungen

- Do Behavioral Biases Affect Prices?: Joshua D. Coval and Tyler ShumwayDokument34 SeitenDo Behavioral Biases Affect Prices?: Joshua D. Coval and Tyler Shumwaysafa haddadNoch keine Bewertungen

- Lit ReviewDokument5 SeitenLit ReviewsriharshagNoch keine Bewertungen

- 1 - Literature Review IPODokument26 Seiten1 - Literature Review IPOFatouma Ahmed IbrahimNoch keine Bewertungen

- BAJRA Ujkan & HASANI Burim - Event Study On Stock SplitsDokument7 SeitenBAJRA Ujkan & HASANI Burim - Event Study On Stock SplitsKenan DaciNoch keine Bewertungen

- 2Dokument67 Seiten2Rahul AnandNoch keine Bewertungen

- Khawaja Synopsis ResearchDokument12 SeitenKhawaja Synopsis ResearchObaid RehmanNoch keine Bewertungen

- Investment Banks in India & IPO Under Pricing - Case StudyDokument17 SeitenInvestment Banks in India & IPO Under Pricing - Case StudyAkshay BhatnagarNoch keine Bewertungen

- Can Mutual Fund Managers Pick Stocks? Evidence From Their Trades Prior To Earnings AnnouncementsDokument34 SeitenCan Mutual Fund Managers Pick Stocks? Evidence From Their Trades Prior To Earnings AnnouncementsHendri AnjayantoNoch keine Bewertungen

- Project On IPO of Cafe Coffee DayDokument45 SeitenProject On IPO of Cafe Coffee DayVinit Dawane100% (1)

- 2613 10450 1 PB PDFDokument10 Seiten2613 10450 1 PB PDFEngr Fizza AkbarNoch keine Bewertungen

- SSRN Id2126478Dokument38 SeitenSSRN Id2126478nghks1Noch keine Bewertungen

- Kallapur 1999Dokument15 SeitenKallapur 1999Puspita NingtyasNoch keine Bewertungen

- Are Ipos UnderpricedDokument38 SeitenAre Ipos UnderpricedéricNoch keine Bewertungen

- Fond PerformanteDokument5 SeitenFond PerformanteAura ŞtefănescuNoch keine Bewertungen

- Project Financial ManagementDokument12 SeitenProject Financial ManagementMuhamamd Haris RanaNoch keine Bewertungen

- The Relationship Between Fundamental Analysis and Stock Returns Based On The Panel Data Analysis Evidence From Karachi Stock Exchange (KSE)Dokument13 SeitenThe Relationship Between Fundamental Analysis and Stock Returns Based On The Panel Data Analysis Evidence From Karachi Stock Exchange (KSE)Cristina CiobanuNoch keine Bewertungen

- The Impact of Free Cash Flow On Market Value of Firm: Abdul Nafea Al Zararee and Abdulrahman Al-AzzawiDokument8 SeitenThe Impact of Free Cash Flow On Market Value of Firm: Abdul Nafea Al Zararee and Abdulrahman Al-AzzawibagusNoch keine Bewertungen

- Investment AnalysisDokument9 SeitenInvestment AnalysisEric AwinoNoch keine Bewertungen

- Zarraree PDFDokument8 SeitenZarraree PDFkshitijsaxenaNoch keine Bewertungen

- Haugen BakerDokument39 SeitenHaugen Bakerjared46Noch keine Bewertungen

- Chapter - Ii Review of Literature & Research MethodologyDokument32 SeitenChapter - Ii Review of Literature & Research Methodologypratik0909100% (1)

- LR Insider TradingDokument4 SeitenLR Insider TradingAsif Khan NiaziNoch keine Bewertungen

- Li380892 AcceptedDokument31 SeitenLi380892 AcceptedGenta AnnaNoch keine Bewertungen

- Pairs Trading - Performance of A Relative-Value Arbitrage RuleDokument31 SeitenPairs Trading - Performance of A Relative-Value Arbitrage RulemateusfmpetryNoch keine Bewertungen

- 379 756 1 PBDokument7 Seiten379 756 1 PBfakrijal bsiNoch keine Bewertungen

- Investigating The Performance of Selected Real Estate CompaniesDokument12 SeitenInvestigating The Performance of Selected Real Estate CompaniesggsitmsNoch keine Bewertungen

- 47 CastaterDokument14 Seiten47 CastatercarminatNoch keine Bewertungen

- Thesis FinalDokument16 SeitenThesis FinalAlagon, Justine Lloyd H.Noch keine Bewertungen

- Stock Market Analysis: A Review and Taxonomy of Prediction TechniquesDokument22 SeitenStock Market Analysis: A Review and Taxonomy of Prediction TechniquesSadeen MobinNoch keine Bewertungen

- Stock Market Analysis: A Review and Taxonomy of Prediction TechniquesDokument22 SeitenStock Market Analysis: A Review and Taxonomy of Prediction TechniquesNikhil AroraNoch keine Bewertungen

- Результаты регрессий примерDokument12 SeitenРезультаты регрессий примерМаксим НовакNoch keine Bewertungen

- Review of LiteratureDokument4 SeitenReview of LiteratureYogeshWarNoch keine Bewertungen

- Chapter-3 Share Price BehaviourDokument18 SeitenChapter-3 Share Price BehaviourDeepak SinghalNoch keine Bewertungen

- Behavior Pattern of Individual InvestorsDokument16 SeitenBehavior Pattern of Individual InvestorsAnamika BaugNoch keine Bewertungen

- A Modified Price-Sales Ratio: A Useful Tool For Investors?Dokument10 SeitenA Modified Price-Sales Ratio: A Useful Tool For Investors?Theodoros MaragakisNoch keine Bewertungen

- Chapter - 2 Review of LiteratureDokument39 SeitenChapter - 2 Review of LiteratureMannuNoch keine Bewertungen

- Dynamics and Determinants of Dividend Policy in Pakistan (Evidence From Karachi Stock Exchange Non-Financial Listed Firms)Dokument4 SeitenDynamics and Determinants of Dividend Policy in Pakistan (Evidence From Karachi Stock Exchange Non-Financial Listed Firms)Junejo MichaelNoch keine Bewertungen

- Quantum Strategy II: Winning Strategies of Professional InvestmentVon EverandQuantum Strategy II: Winning Strategies of Professional InvestmentNoch keine Bewertungen

- Quantum Strategy: Winning Strategies of Professional InvestmentVon EverandQuantum Strategy: Winning Strategies of Professional InvestmentNoch keine Bewertungen

- Sample Questions: InstructionDokument1 SeiteSample Questions: InstructionShaguftaNoch keine Bewertungen

- Gen of WasteDokument34 SeitenGen of WasteShaguftaNoch keine Bewertungen

- AbcdDokument3 SeitenAbcdShaguftaNoch keine Bewertungen

- 45 ..Islamic BankingDokument47 Seiten45 ..Islamic BankingShaguftaNoch keine Bewertungen

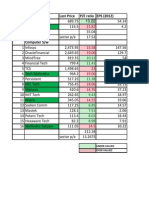

- Sr. No Company Last Price P/E Ratio EPS (2012) : Under Valued Over ValuedDokument5 SeitenSr. No Company Last Price P/E Ratio EPS (2012) : Under Valued Over ValuedShaguftaNoch keine Bewertungen

- Banking Sector ReformsDokument9 SeitenBanking Sector ReformsShaguftaNoch keine Bewertungen

- Lateral Thinking Puzzles IDokument2 SeitenLateral Thinking Puzzles IShaguftaNoch keine Bewertungen

- Republic Planters Bank v. Agana, SR (1997)Dokument11 SeitenRepublic Planters Bank v. Agana, SR (1997)Serve The PeopleNoch keine Bewertungen

- Gene Levoff ComplaintDokument18 SeitenGene Levoff ComplaintGMG EditorialNoch keine Bewertungen

- BG American Equity Segregated Fund - 2023 - SepDokument1 SeiteBG American Equity Segregated Fund - 2023 - Sepsmartinvest2011Noch keine Bewertungen

- Arvind Chaudhary CVDokument3 SeitenArvind Chaudhary CVchaudharyarvindNoch keine Bewertungen

- Corporation General Principles What Is A Corporation?Dokument5 SeitenCorporation General Principles What Is A Corporation?Mirela VerzosaNoch keine Bewertungen

- 2021 CFA Level II Mock Exam - PM Session Victoria Novak Case ScenarioDokument71 Seiten2021 CFA Level II Mock Exam - PM Session Victoria Novak Case ScenarioAstanaNoch keine Bewertungen

- General Mathematics: Quarter 2 - Module 10: Market Indices For Stocks and BondsDokument32 SeitenGeneral Mathematics: Quarter 2 - Module 10: Market Indices For Stocks and BondsDon't mind meNoch keine Bewertungen

- Chapter 3 - Financial Ratio and AnalysisDokument28 SeitenChapter 3 - Financial Ratio and AnalysisSarifah SaidsaripudinNoch keine Bewertungen

- Merger & Acquisition: RequiredDokument19 SeitenMerger & Acquisition: RequiredBKS SannyasiNoch keine Bewertungen

- Lecture 4 (Efficient Market Hypothesis)Dokument46 SeitenLecture 4 (Efficient Market Hypothesis)Devyansh GuptaNoch keine Bewertungen

- Inclusions To Gross Income Illustrative ExamplesDokument5 SeitenInclusions To Gross Income Illustrative ExamplesMary Rose CredoNoch keine Bewertungen

- G1 (Sanket Awate) Pem PFSDokument5 SeitenG1 (Sanket Awate) Pem PFSNirank JadhavNoch keine Bewertungen

- 02 14 CorpoDokument69 Seiten02 14 CorpoFelip MatNoch keine Bewertungen

- Kotak Platinum Sales BrochureDokument24 SeitenKotak Platinum Sales BrochureLogeshParthasarathyNoch keine Bewertungen

- Chap 001Dokument14 SeitenChap 001Adi Susilo100% (1)

- Grade 12 Accounting Case StudyDokument4 SeitenGrade 12 Accounting Case StudyJeff BrookerNoch keine Bewertungen

- Babajide A. A. and Adetiloye K.ADokument29 SeitenBabajide A. A. and Adetiloye K.ATosin JohnsonNoch keine Bewertungen

- Economic and Legal StructuresDokument47 SeitenEconomic and Legal StructuresOckouri BarnesNoch keine Bewertungen

- Crim Pro SyllabusDokument303 SeitenCrim Pro SyllabusAling KinaiNoch keine Bewertungen

- IBM According To Warren Buffett's Annual Letters To ShareholdersDokument15 SeitenIBM According To Warren Buffett's Annual Letters To Shareholdersvahss_11Noch keine Bewertungen

- Imp Accounts KnowledgeDokument17 SeitenImp Accounts KnowledgenomanshafiqueNoch keine Bewertungen

- MCQ Bcom Finance & Tax Financial ServicesDokument29 SeitenMCQ Bcom Finance & Tax Financial Servicesabhishek9763Noch keine Bewertungen

- Sai Kiran Final Project MbaDokument101 SeitenSai Kiran Final Project Mbachethan.chetz95Noch keine Bewertungen

- Poli Law Velasco Cases by Dean Candelaria PDFDokument10 SeitenPoli Law Velasco Cases by Dean Candelaria PDFdemosrea0% (1)