Das könnte Ihnen auch gefallen

- Sarfaesi Act in India: IILM GSM (BATCH: 2011-13)Dokument20 SeitenSarfaesi Act in India: IILM GSM (BATCH: 2011-13)Krishnendu ChowdhuryNoch keine Bewertungen

- PIB 2-14 MarchDokument122 SeitenPIB 2-14 MarchgaganNoch keine Bewertungen

- PR - SEBI Board MeetingDokument3 SeitenPR - SEBI Board MeetingShyam SunderNoch keine Bewertungen

- NPA Recovery ManagementDokument31 SeitenNPA Recovery ManagementSantoshi AravindNoch keine Bewertungen

- Guidelines For Compromise Settlement of Dues of Banks and Financial Institutions Through Lok AdalatsDokument3 SeitenGuidelines For Compromise Settlement of Dues of Banks and Financial Institutions Through Lok AdalatsMahesh Prasad PandeyNoch keine Bewertungen

- Bnmit College ProjectDokument21 SeitenBnmit College ProjectIMAM JAVOORNoch keine Bewertungen

- Study of The Insolvency and Bankruptcy Code 2016Dokument15 SeitenStudy of The Insolvency and Bankruptcy Code 2016Devansh DoshiNoch keine Bewertungen

- X - Financial Regulation and SupervisionDokument31 SeitenX - Financial Regulation and SupervisionjksharanNoch keine Bewertungen

- Chapter-Iii Review of LiteratureDokument41 SeitenChapter-Iii Review of LiteratureAnonymous FUvuOyuTNoch keine Bewertungen

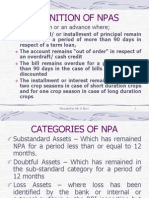

- Definition of Npas: A NPA Is A Loan or An Advance WhereDokument30 SeitenDefinition of Npas: A NPA Is A Loan or An Advance WheremulchandranaNoch keine Bewertungen

- Act, 1993:-The Procedure For Recovery of Debts To The Banks and FinancialDokument7 SeitenAct, 1993:-The Procedure For Recovery of Debts To The Banks and FinancialK KOTHAND RAMI REDDYNoch keine Bewertungen

- Chapter-Iii Review of LiteratureDokument41 SeitenChapter-Iii Review of LiteratureBitecl MesraNoch keine Bewertungen

- Corporate LawDokument36 SeitenCorporate LawJahnnavi SarkhelNoch keine Bewertungen

- Khanna Committee IonsDokument15 SeitenKhanna Committee Ionsvikas1978Noch keine Bewertungen

- Enhanced Regulatory Power To Supersede Board of DirectorsDokument6 SeitenEnhanced Regulatory Power To Supersede Board of DirectorsAnonymous uurrtSaNoch keine Bewertungen

- Anual ReportDokument8 SeitenAnual ReportjanuNoch keine Bewertungen

- Various Recovery Measures Adopted by Banks and Financial InstitutionsDokument19 SeitenVarious Recovery Measures Adopted by Banks and Financial InstitutionsjasmeetNoch keine Bewertungen

- RBI Governor On IBCDokument15 SeitenRBI Governor On IBCyashs-pgdm-2022-24Noch keine Bewertungen

- CA Jan 09Dokument8 SeitenCA Jan 09ElvisPresliiNoch keine Bewertungen

- Banking Sector ReformsDokument6 SeitenBanking Sector ReformsM Abdul MoidNoch keine Bewertungen

- One Time Settlement Scheme - : 3. Corporate RestructuringDokument4 SeitenOne Time Settlement Scheme - : 3. Corporate Restructuringprajay birlaNoch keine Bewertungen

- Difference Between Banks & NBFCDokument8 SeitenDifference Between Banks & NBFCSajesh BelmanNoch keine Bewertungen

- NBFC Project ReportDokument55 SeitenNBFC Project Reportujranchaman64% (11)

- Asg 3Dokument4 SeitenAsg 3Mrugaja Gokhale AurangabadkarNoch keine Bewertungen

- Management of Non-Performing Assets: Presentation by Mr. S. RaviDokument29 SeitenManagement of Non-Performing Assets: Presentation by Mr. S. RaviRajesh MaddiNoch keine Bewertungen

- Working Capital Finance-Recommendations of Various Committees.Dokument33 SeitenWorking Capital Finance-Recommendations of Various Committees.Ranaque JahanNoch keine Bewertungen

- Banking Sector ReformsDokument27 SeitenBanking Sector ReformsArghadeep ChandaNoch keine Bewertungen

- Loan RecoveryDokument62 SeitenLoan RecoveryKaran Thakur100% (1)

- BR Act 1949Dokument25 SeitenBR Act 1949dranita@yahoo.comNoch keine Bewertungen

- Asset ReconstructionDokument20 SeitenAsset Reconstructionlukeskywalker100Noch keine Bewertungen

- Non Banking Financial Company1Dokument7 SeitenNon Banking Financial Company1Prakansha PandeyNoch keine Bewertungen

- Objectives of Bank RegulationDokument15 SeitenObjectives of Bank RegulationParul RamaniNoch keine Bewertungen

- Audit of Accounts of Non-Corporate Entities (Bank Borrowers)Dokument50 SeitenAudit of Accounts of Non-Corporate Entities (Bank Borrowers)Manikandan ManoharNoch keine Bewertungen

- What Is The Role of The Financial System in Economic DevelopmentDokument3 SeitenWhat Is The Role of The Financial System in Economic DevelopmentBasappaSarkarNoch keine Bewertungen

- Assets Reconstruction CompanyDokument8 SeitenAssets Reconstruction CompanyKartik VariyaNoch keine Bewertungen

- SARFAESI Act Management of NPADokument4 SeitenSARFAESI Act Management of NPAsuchethatiaNoch keine Bewertungen

- Mutual FundsDokument4 SeitenMutual FundsSaumya SomanNoch keine Bewertungen

- Proposals For Financial Sector Reforms in India: An AppraisalDokument7 SeitenProposals For Financial Sector Reforms in India: An Appraisalabha_manakNoch keine Bewertungen

- What Does Nonperforming Asset Mean?Dokument17 SeitenWhat Does Nonperforming Asset Mean?parth8101Noch keine Bewertungen

- Name: Jinal M. MistryDokument10 SeitenName: Jinal M. MistryjinnymistNoch keine Bewertungen

- Reforms in Money MarketDokument5 SeitenReforms in Money MarketKNOWLEDGE CREATORS100% (1)

- Audit of Bank Mcom Part 2Dokument20 SeitenAudit of Bank Mcom Part 2sumi1992Noch keine Bewertungen

- Recovery PolicyDokument83 SeitenRecovery Policymanish kumarNoch keine Bewertungen

- CHAPTERDokument55 SeitenCHAPTERwashimNoch keine Bewertungen

- Recovery Management CDR Bifr Oct, 13Dokument9 SeitenRecovery Management CDR Bifr Oct, 13Amit GiriNoch keine Bewertungen

- B BB Bbanking Anking Anking Anking Anking: U Uu Uupdate Pdate Pdate Pdate PdateDokument20 SeitenB BB Bbanking Anking Anking Anking Anking: U Uu Uupdate Pdate Pdate Pdate PdateGuruswami PrakashNoch keine Bewertungen

- Finance Presentation ReformsDokument10 SeitenFinance Presentation ReformsVaibhav SethNoch keine Bewertungen

- Mid-Term Review of The Annual Policy For The Year 2007-08 - Recovery Agents Engaged by BanksDokument4 SeitenMid-Term Review of The Annual Policy For The Year 2007-08 - Recovery Agents Engaged by BanksGajendra AuodichyaNoch keine Bewertungen

- Corporate Banking: 11/04/21 Om All Rights Reserved. 1Dokument180 SeitenCorporate Banking: 11/04/21 Om All Rights Reserved. 1Pravah ShuklaNoch keine Bewertungen

- RBI Master Circular On Wilful Defaulters (As On July - 2015)Dokument21 SeitenRBI Master Circular On Wilful Defaulters (As On July - 2015)Saikat ChakrabortyNoch keine Bewertungen

- 03 - IntroductionDokument50 Seiten03 - IntroductionVirendra JhaNoch keine Bewertungen

- Value Addition Notes - Indian EconomyDokument6 SeitenValue Addition Notes - Indian Economynikitash1222Noch keine Bewertungen

- Assignment FinancialSectorReforms1991Dokument4 SeitenAssignment FinancialSectorReforms1991Swathi SriNoch keine Bewertungen

- Audit of BanksDokument13 SeitenAudit of BanksAniket NirantaleNoch keine Bewertungen

- Commercial Banks: Roup Members: Kiran Faiz Sumera Razaque Danish Ali Geeta BaiDokument45 SeitenCommercial Banks: Roup Members: Kiran Faiz Sumera Razaque Danish Ali Geeta BaiAdeel RanaNoch keine Bewertungen

- Sources of Funds: Savings DepositsDokument15 SeitenSources of Funds: Savings DepositsRavi D S VeeraNoch keine Bewertungen

- Frauds in Micro FinanceDokument6 SeitenFrauds in Micro FinanceSyed MohammedNoch keine Bewertungen

- Auditing Unit 4 NotesDokument19 SeitenAuditing Unit 4 NotesUjjwal MalhotraNoch keine Bewertungen

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Von EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Noch keine Bewertungen

- Mental Chemistry PDFDokument68 SeitenMental Chemistry PDFSK MishraNoch keine Bewertungen

- Securitisation Companies and Reconstruction Companies (SCRC) DRDokument31 SeitenSecuritisation Companies and Reconstruction Companies (SCRC) DRSK MishraNoch keine Bewertungen

- Securitisation Companies and Reconstruction Companies (SCRC) DRDokument31 SeitenSecuritisation Companies and Reconstruction Companies (SCRC) DRSK MishraNoch keine Bewertungen

- Mental Chemistry PDFDokument68 SeitenMental Chemistry PDFSK MishraNoch keine Bewertungen

- Am I Good at CommunicationDokument2 SeitenAm I Good at CommunicationSK MishraNoch keine Bewertungen

- Guidelines For Rehabilitation of Sick Small Scale Industrial UnitsDokument15 SeitenGuidelines For Rehabilitation of Sick Small Scale Industrial UnitsIed UPNoch keine Bewertungen

- Am I Good at CommunicationDokument2 SeitenAm I Good at CommunicationSK MishraNoch keine Bewertungen

- MRG MantraDokument2 SeitenMRG MantraSK MishraNoch keine Bewertungen

- Guidelines For Rehabilitation of Sick Small Scale Industrial UnitsDokument15 SeitenGuidelines For Rehabilitation of Sick Small Scale Industrial UnitsIed UPNoch keine Bewertungen

- Health Awarness NewDokument50 SeitenHealth Awarness NewSK MishraNoch keine Bewertungen

- Interpersonal CommunicationDokument7 SeitenInterpersonal CommunicationSK MishraNoch keine Bewertungen

- NLP IntroductionDokument5 SeitenNLP IntroductionSK MishraNoch keine Bewertungen

- UBDDokument7 SeitenUBDSK MishraNoch keine Bewertungen

- TenPrayers StudyGuide PDFDokument39 SeitenTenPrayers StudyGuide PDFSK MishraNoch keine Bewertungen

- 90 Year OldDokument4 Seiten90 Year OldSK MishraNoch keine Bewertungen

- TenPrayers StudyGuide PDFDokument39 SeitenTenPrayers StudyGuide PDFSK MishraNoch keine Bewertungen

- UBDDokument7 SeitenUBDSK MishraNoch keine Bewertungen

- ManifestingDokument65 SeitenManifestingahmedekram100% (12)

- UBDDokument7 SeitenUBDSK MishraNoch keine Bewertungen

- The Magic of Making Up PDFDokument11 SeitenThe Magic of Making Up PDFSK Mishra33% (6)

- Central Banking PDFDokument112 SeitenCentral Banking PDFSK Mishra100% (2)

- Central Banking PDFDokument112 SeitenCentral Banking PDFSK Mishra100% (2)

- ManifestingDokument65 SeitenManifestingahmedekram100% (12)

- PEL PakistanDokument27 SeitenPEL Pakistanjutt707100% (1)

- BMC Colg WorkDokument3 SeitenBMC Colg Workvishal sinhaNoch keine Bewertungen

- Nestle GlobalizationDokument30 SeitenNestle GlobalizationDaryll Peter Griffith60% (5)

- Case Study Analysis Graphic OrganizerDokument3 SeitenCase Study Analysis Graphic OrganizerAshwinKumarNoch keine Bewertungen

- Kisi-Kisi Uts Enterprise System Tipe I - Kemungkinan Bisa KeluarDokument16 SeitenKisi-Kisi Uts Enterprise System Tipe I - Kemungkinan Bisa KeluarwahyuNoch keine Bewertungen

- Chapter 2 - Analyzing The External Environment of The FirmDokument30 SeitenChapter 2 - Analyzing The External Environment of The FirmLEVI RUTH ADUNANoch keine Bewertungen

- Ms. Nivedita Ganiger Phone No: 6362273614Dokument2 SeitenMs. Nivedita Ganiger Phone No: 6362273614niveditaNoch keine Bewertungen

- Learning Objectives - VAT (FINAL)Dokument2 SeitenLearning Objectives - VAT (FINAL)Pranay GovenderNoch keine Bewertungen

- Maruti Suzuki India LTDDokument8 SeitenMaruti Suzuki India LTDRushikesh PawarNoch keine Bewertungen

- Lecture 1 - Introduction of Financial ManagementDokument18 SeitenLecture 1 - Introduction of Financial ManagementMaazNoch keine Bewertungen

- RFP Template Government ModelDokument19 SeitenRFP Template Government ModellgdkulclsubucvhgdjNoch keine Bewertungen

- Methods of Software AcquisitionDokument12 SeitenMethods of Software AcquisitionSimranjeet Singh100% (4)

- Example of Break Even AnalysisDokument1 SeiteExample of Break Even AnalysisCarmella BalboaNoch keine Bewertungen

- Cola WarsDokument24 SeitenCola WarsPradIpta Kaphle100% (3)

- Income Taxation Quick NotesDokument3 SeitenIncome Taxation Quick NotesKathNoch keine Bewertungen

- SM Prime Holdings, Inc. - Sec Form 17-A-2020Dokument265 SeitenSM Prime Holdings, Inc. - Sec Form 17-A-2020Lorraine AlboNoch keine Bewertungen

- 2221 - Acct6328039 - Lkfa - TP1-W2-S3-R2 - 2602285150 - Amama Ira Amalia PriyonoDokument11 Seiten2221 - Acct6328039 - Lkfa - TP1-W2-S3-R2 - 2602285150 - Amama Ira Amalia PriyonoAmama AI APNoch keine Bewertungen

- SaurabhDokument16 SeitenSaurabhAkshay Singh100% (1)

- Statement IbblDokument1 SeiteStatement Ibblmamunkhan1216jNoch keine Bewertungen

- Chapter 18 ControllingDokument24 SeitenChapter 18 ControllingAsad Uz Jaman100% (2)

- Impact of Digitalization On Procurement The Case of Robotic Process AutomationDokument11 SeitenImpact of Digitalization On Procurement The Case of Robotic Process AutomationNassMezNoch keine Bewertungen

- Balance Sheet For Mahindra & Mahindra Pvt. LTD.: Assets Amount (In Crores) Non-Current AssetsDokument32 SeitenBalance Sheet For Mahindra & Mahindra Pvt. LTD.: Assets Amount (In Crores) Non-Current AssetsAniketNoch keine Bewertungen

- Paperwork Simulation PacketDokument11 SeitenPaperwork Simulation PacketHadi P.Noch keine Bewertungen

- Capital Budgeting Project ReportDokument97 SeitenCapital Budgeting Project ReportPriyanshu Singh0% (1)

- The 60 Minute Startup PDFDokument3 SeitenThe 60 Minute Startup PDFtawatchai limNoch keine Bewertungen

- TOGAF 9.1 - Level 1 and 2 Student Handbook - ITpreneurs PDFDokument64 SeitenTOGAF 9.1 - Level 1 and 2 Student Handbook - ITpreneurs PDFZain AtifNoch keine Bewertungen

- T3TMD - Miscellaneous Deals - R10Dokument78 SeitenT3TMD - Miscellaneous Deals - R10KLB USERNoch keine Bewertungen

- Sample FS PDFDokument20 SeitenSample FS PDFCjls KthyNoch keine Bewertungen

- Product Management Final ExamDokument25 SeitenProduct Management Final ExamAnthony OpesNoch keine Bewertungen

- G12 Principles of Marketing Week 3Dokument9 SeitenG12 Principles of Marketing Week 3Glychalyn Abecia 23Noch keine Bewertungen