Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- FIN310 Module 3 Excel AssignmentDokument27 SeitenFIN310 Module 3 Excel AssignmentJonathan BurgosNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Chapter 7Dokument46 SeitenChapter 7Awrangzeb AwrangNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Module 3Dokument22 SeitenModule 3Suprita Karajgi100% (1)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Risk Assessment Worksheet BlankDokument5 SeitenRisk Assessment Worksheet BlankisolongNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Capital Allocation Across RiskyDokument23 SeitenCapital Allocation Across RiskyVaidyanathan RavichandranNoch keine Bewertungen

- Account Statement BY90MTBK30140008000003271543Dokument1 SeiteAccount Statement BY90MTBK30140008000003271543savasdvsdavsadvdNoch keine Bewertungen

- Taxation, Types of Taxation, Main Objectives of TaxationDokument4 SeitenTaxation, Types of Taxation, Main Objectives of TaxationKc Cassandra RosalNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- U.S. Individual Income Tax Return: Filing StatusDokument14 SeitenU.S. Individual Income Tax Return: Filing StatusDavid Dautel100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Company ProfileDokument15 SeitenCompany ProfileAslam HossainNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- G Izekf - KR FD K TKRK Gs FD BL Foi DK Vko' D Bunzkt DS'K CQD O Fmiksftv JFTLVJ Esa DJ FN K X K GsaaDokument4 SeitenG Izekf - KR FD K TKRK Gs FD BL Foi DK Vko' D Bunzkt DS'K CQD O Fmiksftv JFTLVJ Esa DJ FN K X K GsaaRakesh AryaNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- A Company Is An Artificial Person Created by LawDokument5 SeitenA Company Is An Artificial Person Created by LawNeelabhNoch keine Bewertungen

- Course OutlineDokument13 SeitenCourse OutlineKabile MwitaNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- 1109021 (1)Dokument1 Seite1109021 (1)Cms Stl CmsNoch keine Bewertungen

- EPS Bootstrapping Bootstrap Earnings e EctDokument2 SeitenEPS Bootstrapping Bootstrap Earnings e Ecthyba ben helalNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Screenshot 2021-06-22 at 12.21.23 PMDokument18 SeitenScreenshot 2021-06-22 at 12.21.23 PMHarshad130Noch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Exchange Rate Exposure and Its Determinants Evidence From Indian FirmsDokument16 SeitenExchange Rate Exposure and Its Determinants Evidence From Indian Firmsswapnil tyagiNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Advanced Global Trading - AGT Arena #1Dokument38 SeitenAdvanced Global Trading - AGT Arena #1advanceglobaltradingNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Cash Flow Estimation and Capital BudgetingDokument29 SeitenCash Flow Estimation and Capital BudgetingShehroz Saleem QureshiNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Negotiable InstrumentsQ&ADokument11 SeitenNegotiable InstrumentsQ&AMelgen100% (1)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- MTQS Investment Appraisal Test AnsDokument5 SeitenMTQS Investment Appraisal Test AnsChoudhristNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Pefindo'S Corporate Default and Rating Transition Study (1996 - 2010)Dokument21 SeitenPefindo'S Corporate Default and Rating Transition Study (1996 - 2010)Theo VladimirNoch keine Bewertungen

- Sale and Purchase Agreement OSCAR ALEJANDRO GALVIS SANTIAGODokument6 SeitenSale and Purchase Agreement OSCAR ALEJANDRO GALVIS SANTIAGOTinktas pcsNoch keine Bewertungen

- Difference Between IMF and World BankDokument4 SeitenDifference Between IMF and World BankSourabh ShuklaNoch keine Bewertungen

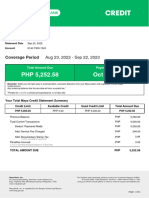

- MayaCredit SoA 2023SEPDokument3 SeitenMayaCredit SoA 2023SEPjepoy palaruanNoch keine Bewertungen

- Walt Disney Financial StatementDokument8 SeitenWalt Disney Financial StatementShaReyNoch keine Bewertungen

- Commerce Class 12 Semester2Dokument31 SeitenCommerce Class 12 Semester2Tesmon MathewNoch keine Bewertungen

- Frauds-in-Indian-Banking SectorDokument61 SeitenFrauds-in-Indian-Banking SectorPranav ViraNoch keine Bewertungen

- Payroll Management SystemDokument8 SeitenPayroll Management SystemMayur Jondhale MJNoch keine Bewertungen

- Ch17 - Analysis of Bonds W Embedded Options.ADokument25 SeitenCh17 - Analysis of Bonds W Embedded Options.Akerenkang100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- New Zealand 2009 Financial Knowledge SurveyDokument11 SeitenNew Zealand 2009 Financial Knowledge SurveywmhuthnanceNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)