Das könnte Ihnen auch gefallen

- D&D 3.5 Edition - Fiendish Codex I - Hordes of The Abyss PDFDokument191 SeitenD&D 3.5 Edition - Fiendish Codex I - Hordes of The Abyss PDFIgnacio Peralta93% (15)

- Basics of Petroleum GeologyDokument23 SeitenBasics of Petroleum GeologyShahnawaz MustafaNoch keine Bewertungen

- Mechanics of Materials 7th Edition Beer Johnson Chapter 6Dokument134 SeitenMechanics of Materials 7th Edition Beer Johnson Chapter 6Riston Smith95% (96)

- Principal Component Analysis I ToDokument298 SeitenPrincipal Component Analysis I ToSuleyman Kale100% (1)

- LhiannanDokument6 SeitenLhiannanGreybornNoch keine Bewertungen

- Robert Egby - DecreesDokument9 SeitenRobert Egby - DecreesmuzickaueNoch keine Bewertungen

- Fabric DefectsDokument30 SeitenFabric Defectsaparna_ftNoch keine Bewertungen

- Major Stakeholders in Health Care SystemDokument5 SeitenMajor Stakeholders in Health Care SystemANITTA S100% (1)

- Exam Ref 70 483 Programming in C by Wouter de Kort PDFDokument2 SeitenExam Ref 70 483 Programming in C by Wouter de Kort PDFPhilNoch keine Bewertungen

- SchedulingDokument47 SeitenSchedulingKonark PatelNoch keine Bewertungen

- Detailed Lesson Plan in Mathematics (Pythagorean Theorem)Dokument6 SeitenDetailed Lesson Plan in Mathematics (Pythagorean Theorem)Carlo DascoNoch keine Bewertungen

- Jurnal KORELASI ANTARA STATUS GIZI IBU MENYUSUI DENGAN KECUKUPAN ASIDokument9 SeitenJurnal KORELASI ANTARA STATUS GIZI IBU MENYUSUI DENGAN KECUKUPAN ASIMarsaidNoch keine Bewertungen

- Aspen HYSYS - Steady States and Dynamic Simulator (Introduction) PDFDokument24 SeitenAspen HYSYS - Steady States and Dynamic Simulator (Introduction) PDFtuan.huu2007Noch keine Bewertungen

- Chapter 14-01-15 FinalDokument17 SeitenChapter 14-01-15 FinalGörkem VarolNoch keine Bewertungen

- Improved Incremental Orthogonal Centroid Algorithm For Visualising Pipeline Sensor DatasetsDokument13 SeitenImproved Incremental Orthogonal Centroid Algorithm For Visualising Pipeline Sensor DatasetstecnicoengenNoch keine Bewertungen

- Mehrkanoon 2012Dokument12 SeitenMehrkanoon 2012yalocim666Noch keine Bewertungen

- Numerical Methods For Partial Differential Equations ThesisDokument7 SeitenNumerical Methods For Partial Differential Equations Thesissydneynoriegadenton100% (1)

- MATHSCSDokument3 SeitenMATHSCStonystark93115Noch keine Bewertungen

- Brunel Thesis GuidelinesDokument6 SeitenBrunel Thesis GuidelinesAnna Landers100% (2)

- Theory of Structures V-Combined PDFDokument90 SeitenTheory of Structures V-Combined PDFRotich VincentNoch keine Bewertungen

- Seminar On D.O.EDokument33 SeitenSeminar On D.O.ERaunak Gupta100% (1)

- Discrete Element Modelling of Large Scale Particle Systems-I: Exact Scaling LawsDokument11 SeitenDiscrete Element Modelling of Large Scale Particle Systems-I: Exact Scaling LawsMuhammad Adnan LaghariNoch keine Bewertungen

- Probabilistic Load FlowDokument66 SeitenProbabilistic Load FlowMuhammad Usama Muhammad Saleem100% (1)

- JWRPMWR22551 Final VersionDokument57 SeitenJWRPMWR22551 Final VersionValentin VeselinovNoch keine Bewertungen

- Ology Driven EUR PredictionDokument10 SeitenOlogy Driven EUR PredictionĐỗ AnhNoch keine Bewertungen

- From Physics To Medical Imaging, Through Electronics and DetectorsDokument110 SeitenFrom Physics To Medical Imaging, Through Electronics and Detectorsmahdi123456789Noch keine Bewertungen

- A New Approach of Principal Component Regression EDokument8 SeitenA New Approach of Principal Component Regression ERosihan SuandiNoch keine Bewertungen

- Robust Decision TreesDokument6 SeitenRobust Decision TreesjrodascNoch keine Bewertungen

- Skrehota Presentation Dtedi 2012-04 16Dokument23 SeitenSkrehota Presentation Dtedi 2012-04 16Krishanarju VenkatesanNoch keine Bewertungen

- 09,10 - Facility Location Models For Distribution System DesignDokument26 Seiten09,10 - Facility Location Models For Distribution System DesignPedro BragaNoch keine Bewertungen

- Special Session On Convex Optimization For System IdentificationDokument60 SeitenSpecial Session On Convex Optimization For System Identificationalex240574Noch keine Bewertungen

- Iaor - P1 PDFDokument43 SeitenIaor - P1 PDFkhawla2789Noch keine Bewertungen

- Economics 2018 4Dokument33 SeitenEconomics 2018 4Hufzi KhanNoch keine Bewertungen

- DataDokument11 SeitenDataShrey ShahNoch keine Bewertungen

- Applied Statistics - IntroductionDokument113 SeitenApplied Statistics - Introductionrandkofahi2004Noch keine Bewertungen

- Model Order Reduction ThesisDokument4 SeitenModel Order Reduction Thesisvaleriemejiabakersfield100% (2)

- ElectronicsDokument12 SeitenElectronicsSaransh MittalNoch keine Bewertungen

- Ntu Eee PHD Thesis SubmissionDokument5 SeitenNtu Eee PHD Thesis Submissionjedod0nelit3100% (2)

- CHAPTER 1 TheoremDokument20 SeitenCHAPTER 1 Theoremhahoang33322Noch keine Bewertungen

- Researchpaper Ordinary Differential Equations MATLAB Simulink SolutionsDokument8 SeitenResearchpaper Ordinary Differential Equations MATLAB Simulink SolutionsAbnet EthiopiaNoch keine Bewertungen

- Gustavo Stas PCA GenericDokument52 SeitenGustavo Stas PCA GenericMohammad Nahid MiaNoch keine Bewertungen

- Accepted For Publication in Journal of Operations Management DOI: 10.1016/j.jom.2016.05.002Dokument72 SeitenAccepted For Publication in Journal of Operations Management DOI: 10.1016/j.jom.2016.05.002mateomejia741Noch keine Bewertungen

- Partial Least Squares Path Modeling Using Ordinal Categorical IndicatorsDokument27 SeitenPartial Least Squares Path Modeling Using Ordinal Categorical IndicatorsHung PhanNoch keine Bewertungen

- K SMHHHDBDokument5 SeitenK SMHHHDBTjeripo Ray KahuureNoch keine Bewertungen

- 19MA217 Random Processes and StatisticsDokument3 Seiten19MA217 Random Processes and StatisticsMukesh MugiNoch keine Bewertungen

- Locally Linear Embedding AlgorithmDokument127 SeitenLocally Linear Embedding Algorithmp1muellerNoch keine Bewertungen

- Bachelor Thesis Eth MavtDokument8 SeitenBachelor Thesis Eth Mavtafcmqldsw100% (2)

- Chapter 1Dokument24 SeitenChapter 1hahoang33322Noch keine Bewertungen

- Illumination of Lighting PipesDokument153 SeitenIllumination of Lighting PipesTommyc1024Noch keine Bewertungen

- Tabu Search Heuristic For A Two-Echelon Location-Routing ProblemDokument42 SeitenTabu Search Heuristic For A Two-Echelon Location-Routing ProblemJuan Sebastián Poveda GulfoNoch keine Bewertungen

- ChamPock AnDokument160 SeitenChamPock Analejandro.david1642Noch keine Bewertungen

- Ame2223 SyllabusDokument5 SeitenAme2223 SyllabusErmita YusidaNoch keine Bewertungen

- Concepts and Techniques: Data MiningDokument78 SeitenConcepts and Techniques: Data MiningAnshul SinghNoch keine Bewertungen

- 11 Measurement and Data ProcessingDokument7 Seiten11 Measurement and Data ProcessingMichaelNoch keine Bewertungen

- Eth Bachelor ThesisDokument5 SeitenEth Bachelor Thesisbk4pfxb7100% (2)

- Study and Generation of Optimal Speckle Patterns For DIC: January 2007Dokument8 SeitenStudy and Generation of Optimal Speckle Patterns For DIC: January 2007FUN SCIENCENoch keine Bewertungen

- ! Pedestrian DetectionDokument20 Seiten! Pedestrian DetectionMohamed Hechmi JERIDINoch keine Bewertungen

- Customer Management Tutorial 2 Charting Data: An Introduction To VariationDokument12 SeitenCustomer Management Tutorial 2 Charting Data: An Introduction To VariationShahin MohamedNoch keine Bewertungen

- Takane&Young 1977Dokument61 SeitenTakane&Young 1977Miguel Cruz RamírezNoch keine Bewertungen

- Peak Indexing and Lattice Parameter RefinementDokument14 SeitenPeak Indexing and Lattice Parameter RefinementSepehr Bagheri100% (1)

- Partial Least Squares Path Modeling Using Ordinal Categorical Indicators PDFDokument28 SeitenPartial Least Squares Path Modeling Using Ordinal Categorical Indicators PDFAurangzeb ChaudharyNoch keine Bewertungen

- ROI DeepLearningDokument11 SeitenROI DeepLearningdas.sandipan5102002Noch keine Bewertungen

- FM Ch4 Lecture AASTU.Dokument81 SeitenFM Ch4 Lecture AASTU.Abenezer KassahunNoch keine Bewertungen

- Incorporating Plain English Driller Comments Into Machine Learning Drilling OptimizationDokument22 SeitenIncorporating Plain English Driller Comments Into Machine Learning Drilling OptimizationSaba SuhailNoch keine Bewertungen

- Ohdsi 2016 Cerner Etl v1Dokument2 SeitenOhdsi 2016 Cerner Etl v1abbas.fadhail5dNoch keine Bewertungen

- Data Envelo P Ment Analy Si S - Basi C Mo Dels and Thei R Uti Li Zati o NDokument7 SeitenData Envelo P Ment Analy Si S - Basi C Mo Dels and Thei R Uti Li Zati o NAdarsh VarmaNoch keine Bewertungen

- MB0032 Operations ResearchDokument38 SeitenMB0032 Operations ResearchSaurabh MIshra12100% (1)

- How to Find Inter-Groups Differences Using Spss/Excel/Web Tools in Common Experimental Designs: Book 1Von EverandHow to Find Inter-Groups Differences Using Spss/Excel/Web Tools in Common Experimental Designs: Book 1Noch keine Bewertungen

- A Discrete-Time Approach for system AnalysisVon EverandA Discrete-Time Approach for system AnalysisMichel CuenodNoch keine Bewertungen

- Ontogeny of Skull Size and Shape Changes Within A Framework of Biphasic Lifestyle: A Case Study in Six Triturus Species (Amphibia, Salamandridae)Dokument11 SeitenOntogeny of Skull Size and Shape Changes Within A Framework of Biphasic Lifestyle: A Case Study in Six Triturus Species (Amphibia, Salamandridae)mikimaricNoch keine Bewertungen

- Lab4 NaiveBayesDokument17 SeitenLab4 NaiveBayeshitesh_dhingra1987Noch keine Bewertungen

- Postupak Konfiguracije ADSL Modema ZTEDokument8 SeitenPostupak Konfiguracije ADSL Modema ZTEAdis ZenNoch keine Bewertungen

- Journal of Visual Communication and Image Representation Volume 24 Issue 2 2013 (Doi 10.1016/j.jvcir.2012.08.002) Barzigar, Nafise Roozgard, Aminmohammad Cheng, Samuel Verma, - SCoBeP - Dense ImaDokument11 SeitenJournal of Visual Communication and Image Representation Volume 24 Issue 2 2013 (Doi 10.1016/j.jvcir.2012.08.002) Barzigar, Nafise Roozgard, Aminmohammad Cheng, Samuel Verma, - SCoBeP - Dense ImamikimaricNoch keine Bewertungen

- Paw Patrol Pin The Badge On SkyeDokument5 SeitenPaw Patrol Pin The Badge On SkyemikimaricNoch keine Bewertungen

- Choo Chart 82255418560Dokument6 SeitenChoo Chart 82255418560mikimaricNoch keine Bewertungen

- Piezo FilmDokument89 SeitenPiezo Filmmcu_power100% (1)

- Dimension Ali Tyre Duct IonDokument28 SeitenDimension Ali Tyre Duct IonGiorgio De NunzioNoch keine Bewertungen

- A Review On Neural Network-Based Image Segmentation TechniquesDokument23 SeitenA Review On Neural Network-Based Image Segmentation TechniquesmikimaricNoch keine Bewertungen

- Tl-wr941nd v3 UgDokument113 SeitenTl-wr941nd v3 UgJosé Manuel Murillo RiveraNoch keine Bewertungen

- FLTK TutorialDokument31 SeitenFLTK TutorialDiego RojasNoch keine Bewertungen

- Lecture 2: Transformations and Histograms: H (K) Number of Pixels Whose Shade Equals K (U (I, J) K)Dokument12 SeitenLecture 2: Transformations and Histograms: H (K) Number of Pixels Whose Shade Equals K (U (I, J) K)mikimaricNoch keine Bewertungen

- Graphs Breadth First SearchDokument5 SeitenGraphs Breadth First SearchmikimaricNoch keine Bewertungen

- 10318Dokument9 Seiten10318mikimaricNoch keine Bewertungen

- Newton-Raphson Power Flow ImplementationDokument17 SeitenNewton-Raphson Power Flow ImplementationmikimaricNoch keine Bewertungen

- Convol 3 D 16 BitDokument14 SeitenConvol 3 D 16 BitmikimaricNoch keine Bewertungen

- High-Performance Cone Beam Reconstruction Using Cuda Compatible GpusDokument22 SeitenHigh-Performance Cone Beam Reconstruction Using Cuda Compatible GpusmikimaricNoch keine Bewertungen

- BL FilterDokument10 SeitenBL FiltermikimaricNoch keine Bewertungen

- 3 Widgets and LayoutsDokument69 Seiten3 Widgets and LayoutsmikimaricNoch keine Bewertungen

- An Adaptive K-Means Clustering Algorithm For Breast Image SegmentationDokument4 SeitenAn Adaptive K-Means Clustering Algorithm For Breast Image SegmentationmikimaricNoch keine Bewertungen

- Paper FinalDokument10 SeitenPaper FinalmikimaricNoch keine Bewertungen

- Swath An Thir A KumarDokument120 SeitenSwath An Thir A KumarmikimaricNoch keine Bewertungen

- 10 Mentiras AudioDokument2 Seiten10 Mentiras AudiomrchakaNoch keine Bewertungen

- ITK HandoutDokument100 SeitenITK HandoutmikimaricNoch keine Bewertungen

- Lesson 3 - Adaptation AssignmentDokument3 SeitenLesson 3 - Adaptation AssignmentEmmy RoseNoch keine Bewertungen

- 42ld340h Commercial Mode Setup Guide PDFDokument59 Seiten42ld340h Commercial Mode Setup Guide PDFGanesh BabuNoch keine Bewertungen

- Matrix CPP CombineDokument14 SeitenMatrix CPP CombineAbhinav PipalNoch keine Bewertungen

- 1Dokument14 Seiten1Cecille GuillermoNoch keine Bewertungen

- Study of Subsonic Wind Tunnel and Its Calibration: Pratik V. DedhiaDokument8 SeitenStudy of Subsonic Wind Tunnel and Its Calibration: Pratik V. DedhiaPratikDedhia99Noch keine Bewertungen

- Damage To Bottom Ash Handling SysDokument6 SeitenDamage To Bottom Ash Handling SyssanjeevchhabraNoch keine Bewertungen

- Submitted By: S.M. Tajuddin Group:245Dokument18 SeitenSubmitted By: S.M. Tajuddin Group:245KhurshidbuyamayumNoch keine Bewertungen

- Suggestions On How To Prepare The PortfolioDokument2 SeitenSuggestions On How To Prepare The PortfolioPeter Pitas DalocdocNoch keine Bewertungen

- 8A L31 Phiếu BTDokument7 Seiten8A L31 Phiếu BTviennhuNoch keine Bewertungen

- Malaybalay CityDokument28 SeitenMalaybalay CityCalvin Wong, Jr.Noch keine Bewertungen

- 3-CHAPTER-1 - Edited v1Dokument32 Seiten3-CHAPTER-1 - Edited v1Michael Jaye RiblezaNoch keine Bewertungen

- Actara (5 24 01) PDFDokument12 SeitenActara (5 24 01) PDFBand Dvesto Plus CrepajaNoch keine Bewertungen

- Aryan Civilization and Invasion TheoryDokument60 SeitenAryan Civilization and Invasion TheorySaleh Mohammad Tarif 1912343630Noch keine Bewertungen

- CA Level 2Dokument50 SeitenCA Level 2Cikya ComelNoch keine Bewertungen

- INDUSTRIAL PHD POSITION - Sensor Fusion Enabled Indoor PositioningDokument8 SeitenINDUSTRIAL PHD POSITION - Sensor Fusion Enabled Indoor Positioningzeeshan ahmedNoch keine Bewertungen

- Product 97 File1Dokument2 SeitenProduct 97 File1Stefan StefanNoch keine Bewertungen

- New KitDokument195 SeitenNew KitRamu BhandariNoch keine Bewertungen

- NHD Process PaperDokument2 SeitenNHD Process Paperapi-122116050Noch keine Bewertungen

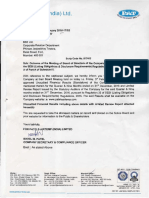

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Dokument4 SeitenStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNoch keine Bewertungen