Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Difference Between Family Takaful and General TakafulDokument2 SeitenDifference Between Family Takaful and General TakafulIbn Bashir Ar-Raisi100% (5)

- Derivative Instruments: in The Financial Marketplace Some Instruments Are Regarded AsDokument53 SeitenDerivative Instruments: in The Financial Marketplace Some Instruments Are Regarded AsRita NyairoNoch keine Bewertungen

- IRDA PresentationDokument22 SeitenIRDA PresentationSamhitha KandlakuntaNoch keine Bewertungen

- CH12Dokument39 SeitenCH12Z pristinNoch keine Bewertungen

- Manonmaniam Sundaranar University: Insurance and Risk ManagementDokument190 SeitenManonmaniam Sundaranar University: Insurance and Risk ManagementDevanshu JulkaNoch keine Bewertungen

- FINMAN ReviewerDokument45 SeitenFINMAN ReviewerGadfrey Doy-acNoch keine Bewertungen

- Health Recharge - Single SheeterDokument2 SeitenHealth Recharge - Single SheeterChinmoy BaruahNoch keine Bewertungen

- NISM-Series V-A MFD CPE Material-Nov-2019Dokument202 SeitenNISM-Series V-A MFD CPE Material-Nov-2019sushilalewa1Noch keine Bewertungen

- Questions 1, 2 and 3 AnswersDokument5 SeitenQuestions 1, 2 and 3 Answerseeyang2Noch keine Bewertungen

- ICICI Prudential Life Insurance Project Report Internship PDFDokument37 SeitenICICI Prudential Life Insurance Project Report Internship PDFu2love50% (2)

- Delphi CorpDokument4 SeitenDelphi Corpadrian_lozano_zNoch keine Bewertungen

- Summary of Mitra CaseDokument2 SeitenSummary of Mitra CaseAayush AgrawalNoch keine Bewertungen

- Insurance Companies-Nepalese PerspectiveDokument29 SeitenInsurance Companies-Nepalese PerspectiveNiraj ShresthaNoch keine Bewertungen

- Cost of Capital - To SendDokument44 SeitenCost of Capital - To SendTejaswini VashisthaNoch keine Bewertungen

- Bwi-Cfq-2013 Portfolio Management QuestionnaireDokument11 SeitenBwi-Cfq-2013 Portfolio Management QuestionnaireShravani Kanagala100% (1)

- ACCA FM TuitionExam CBE 2021-2022 As JG21Jan SPi15MarDokument14 SeitenACCA FM TuitionExam CBE 2021-2022 As JG21Jan SPi15MarchimbanguraNoch keine Bewertungen

- SAPm CIADokument34 SeitenSAPm CIAkan078bct017Noch keine Bewertungen

- Paper - 2: Strategic Financial Management: Alfa Ltd. Beta LTDDokument23 SeitenPaper - 2: Strategic Financial Management: Alfa Ltd. Beta LTDDinesh MaheshwariNoch keine Bewertungen

- JMD Tutorials TYBBI - Revision Sheet Question Bank Prelim Papers With SolutionDokument14 SeitenJMD Tutorials TYBBI - Revision Sheet Question Bank Prelim Papers With Solutionpranil43067% (3)

- Systematic Credit InvestingDokument16 SeitenSystematic Credit Investingbfortuna94Noch keine Bewertungen

- Gary AntonacciDokument106 SeitenGary Antonaccigeorgez111Noch keine Bewertungen

- RCDC SWOT Analysis - Tech Manufacturing FirmsDokument6 SeitenRCDC SWOT Analysis - Tech Manufacturing FirmsPaul Michael AngeloNoch keine Bewertungen

- Insurance ScribdDokument8 SeitenInsurance ScribdAnonymous ZJAXUnNoch keine Bewertungen

- Re InsuranceDokument57 SeitenRe InsuranceSnehal Sawant100% (5)

- Insurance AssignmentDokument15 SeitenInsurance AssignmentRashdullah Shah 133Noch keine Bewertungen

- Ôn Tập Cuối Kỳ - Trắc NghiệmDokument35 SeitenÔn Tập Cuối Kỳ - Trắc Nghiệmthaoluhan456Noch keine Bewertungen

- KIM - Kotak Multi Asset Allocator Fund of Fund - DynamicDokument17 SeitenKIM - Kotak Multi Asset Allocator Fund of Fund - DynamicTedtNoch keine Bewertungen

- Guided Notes - Investment Risks and ReturnsDokument4 SeitenGuided Notes - Investment Risks and ReturnsrebaamoshyNoch keine Bewertungen

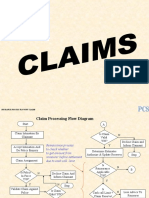

- Insurance Process Flow PPT ClaimsDokument11 SeitenInsurance Process Flow PPT ClaimsSaurabh Maheshwari100% (1)

- BNL Reviewer QuestionnaireDokument29 SeitenBNL Reviewer QuestionnaireKent Mathew BacusNoch keine Bewertungen