Das könnte Ihnen auch gefallen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Financial Management Service Contact Directory 2008Dokument4 SeitenFinancial Management Service Contact Directory 2008api-19731109100% (4)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Accounting Workbook Section 4 AnswersDokument49 SeitenAccounting Workbook Section 4 AnswersAhmed Zeeshan100% (22)

- PMP Test Ex1Dokument45 SeitenPMP Test Ex1mp272Noch keine Bewertungen

- Unit 1 Comprehensive ProjectDokument21 SeitenUnit 1 Comprehensive ProjectJanet Rosario13% (8)

- Castillo V PascoDokument2 SeitenCastillo V PascoSui50% (2)

- Chapters 6-7 and DerivativesDokument68 SeitenChapters 6-7 and DerivativesLouise0% (1)

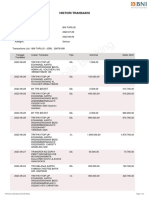

- Histori TransaksiDokument3 SeitenHistori TransaksiIyan SiwuNoch keine Bewertungen

- Experienced CFO in Multi-Entity Environments. Seventeen Years' Experience in Executive Financial Roles Including VP, FD and CFO DesignationsDokument4 SeitenExperienced CFO in Multi-Entity Environments. Seventeen Years' Experience in Executive Financial Roles Including VP, FD and CFO DesignationsVikram Raj SinghNoch keine Bewertungen

- xoIPV9pH45 PDFDokument1 SeitexoIPV9pH45 PDFhalloarnabNoch keine Bewertungen

- Dynamics of The Panchayati Raj System in KeralaDokument41 SeitenDynamics of The Panchayati Raj System in KeralaAjay SudhakaranNoch keine Bewertungen

- Long Test Part 2 QuestionnaireDokument6 SeitenLong Test Part 2 QuestionnaireHarold FilomenoNoch keine Bewertungen

- User ManualDokument51 SeitenUser ManualaNoch keine Bewertungen

- CAT ArithmeticDokument11 SeitenCAT Arithmetichoney1002Noch keine Bewertungen

- Final Case Study 0506Dokument25 SeitenFinal Case Study 0506Namit Nahar67% (3)

- Homework - Week 1 AnswersDokument9 SeitenHomework - Week 1 AnswersDamalie IzaulaNoch keine Bewertungen

- Muhammad Nafiz Ihsan Bin Muhammad: Lembaga Hasil Dalam Negeri Malaysia Borang Permohonan Nombor Pin E-Filing IndividuDokument1 SeiteMuhammad Nafiz Ihsan Bin Muhammad: Lembaga Hasil Dalam Negeri Malaysia Borang Permohonan Nombor Pin E-Filing IndividuLangit CerahNoch keine Bewertungen

- BTS Accounting Firm Trial Balance December 31, 2014Dokument4 SeitenBTS Accounting Firm Trial Balance December 31, 2014Trisha AlaNoch keine Bewertungen

- Mis and Cost AuditDokument12 SeitenMis and Cost AuditFarhanAhmedChowdharyNoch keine Bewertungen

- Working Capital Estimation ProblemsDokument3 SeitenWorking Capital Estimation ProblemsBunny MathaiNoch keine Bewertungen

- Formula Sheet - Time Value of MoneyDokument4 SeitenFormula Sheet - Time Value of MoneyJainil ShahNoch keine Bewertungen

- Unit 3: Indian Accounting Standard 108: Operating SegmentsDokument25 SeitenUnit 3: Indian Accounting Standard 108: Operating SegmentsgauravNoch keine Bewertungen

- SMEDA Research Journal 2015Dokument60 SeitenSMEDA Research Journal 2015Hamid RehmanNoch keine Bewertungen

- Sime Darby Annual Report 2018Dokument348 SeitenSime Darby Annual Report 2018Jia LeNoch keine Bewertungen

- The Dividend Policies of Private Firms - Insights Into Smoothing, Agency Costs, and Information AsymmetryDokument60 SeitenThe Dividend Policies of Private Firms - Insights Into Smoothing, Agency Costs, and Information AsymmetryhhhhhhhNoch keine Bewertungen

- Distance Learning - Regulatory Risk Reporting 2020Dokument9 SeitenDistance Learning - Regulatory Risk Reporting 2020Ashish MathurNoch keine Bewertungen

- FinMan WORKING CAPITAL MANAGEMENT - For PrintingDokument46 SeitenFinMan WORKING CAPITAL MANAGEMENT - For PrintingLito Jose Perez LalantaconNoch keine Bewertungen

- AE 25 Module 1 Lesson 1Dokument99 SeitenAE 25 Module 1 Lesson 1Queeny Mae Cantre ReutaNoch keine Bewertungen

- Imtsons Investments LTDDokument18 SeitenImtsons Investments LTDAakashNoch keine Bewertungen

- The University of DodomaDokument4 SeitenThe University of DodomaMesack SerekiNoch keine Bewertungen

- CourseraDokument23 SeitenCourseraBeatriz LopesNoch keine Bewertungen