Das könnte Ihnen auch gefallen

- Handling Your Sex DriveDokument9 SeitenHandling Your Sex DriveSamuel DwumfourNoch keine Bewertungen

- NewGRE WordsDokument7 SeitenNewGRE WordsMatt Daemon Jr.Noch keine Bewertungen

- Section 12 LymphaticsDokument5 SeitenSection 12 LymphaticsSamuel DwumfourNoch keine Bewertungen

- How To Create A CompanyDokument30 SeitenHow To Create A CompanySamuel DwumfourNoch keine Bewertungen

- Chapter08 002 PricingDokument71 SeitenChapter08 002 PricingSamuel DwumfourNoch keine Bewertungen

- Section 2 SKINDokument48 SeitenSection 2 SKINSamuel DwumfourNoch keine Bewertungen

- Section 1 General ProblemsDokument44 SeitenSection 1 General ProblemsSamuel DwumfourNoch keine Bewertungen

- 1000 Most Common Words (SAT)Dokument70 Seiten1000 Most Common Words (SAT)grellian95% (20)

- Section 16 PoisonsDokument60 SeitenSection 16 PoisonsSamuel DwumfourNoch keine Bewertungen

- Section 7 RespiratoryDokument26 SeitenSection 7 RespiratorySamuel DwumfourNoch keine Bewertungen

- Break Even AnalysisDokument18 SeitenBreak Even AnalysisSamuel DwumfourNoch keine Bewertungen

- Liver Cleasing TherapyDokument31 SeitenLiver Cleasing TherapySamuel DwumfourNoch keine Bewertungen

- Section 3 ExtremitiesDokument19 SeitenSection 3 ExtremitiesSamuel DwumfourNoch keine Bewertungen

- Section 6 UrinaryDokument18 SeitenSection 6 UrinarySamuel DwumfourNoch keine Bewertungen

- Section 2 SKINDokument48 SeitenSection 2 SKINSamuel DwumfourNoch keine Bewertungen

- Audit ReportsDokument5 SeitenAudit ReportsSamuel DwumfourNoch keine Bewertungen

- Chapter 16 Financial Assets and Liabilities: 1. ObjectivesDokument13 SeitenChapter 16 Financial Assets and Liabilities: 1. Objectivessamuel_dwumfourNoch keine Bewertungen

- Receivable 1Dokument4 SeitenReceivable 1Samuel DwumfourNoch keine Bewertungen

- Chapter 16 Financial AssetsDokument3 SeitenChapter 16 Financial AssetsSamuel DwumfourNoch keine Bewertungen

- Chapter 19 Consolidated Statement of Financial Position With Consolidated AdjustmentsDokument3 SeitenChapter 19 Consolidated Statement of Financial Position With Consolidated AdjustmentsSamuel DwumfourNoch keine Bewertungen

- Chapter 17 Accounting for Taxation and Deferred TaxesDokument23 SeitenChapter 17 Accounting for Taxation and Deferred TaxesSamuel DwumfourNoch keine Bewertungen

- Ch17 AnsDokument13 SeitenCh17 AnsSamuel DwumfourNoch keine Bewertungen

- Chapter 19 Consolidated Statement of Financial Position With Consolidated AdjustmentsDokument3 SeitenChapter 19 Consolidated Statement of Financial Position With Consolidated AdjustmentsSamuel DwumfourNoch keine Bewertungen

- Ch18 AnsDokument5 SeitenCh18 AnsSamuel DwumfourNoch keine Bewertungen

- Solution Financial Reporting May 2011Dokument12 SeitenSolution Financial Reporting May 2011Samuel DwumfourNoch keine Bewertungen

- Solution Corporate Reporting Strategy May 2007Dokument10 SeitenSolution Corporate Reporting Strategy May 2007Samuel DwumfourNoch keine Bewertungen

- Associates Chapter 21 SummaryDokument6 SeitenAssociates Chapter 21 SummarySamuel DwumfourNoch keine Bewertungen

- Associates Chapter 21 SummaryDokument6 SeitenAssociates Chapter 21 SummarySamuel DwumfourNoch keine Bewertungen

- Solution Public Sector Accounting May 2010Dokument10 SeitenSolution Public Sector Accounting May 2010Samuel DwumfourNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5783)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Wage and Tax Statement: Page 1 / 4Dokument4 SeitenWage and Tax Statement: Page 1 / 4blon majorsNoch keine Bewertungen

- Nashville State Community College Payroll Accounting - ACCT 2200Dokument9 SeitenNashville State Community College Payroll Accounting - ACCT 2200Bryan Derick Rivad Rafanan0% (1)

- En-PP - 78-Year 2015Dokument24 SeitenEn-PP - 78-Year 2015Eko SanjayaNoch keine Bewertungen

- Guide To The Cambodian Labour Law For The Garment Industry: (Revised 2020)Dokument69 SeitenGuide To The Cambodian Labour Law For The Garment Industry: (Revised 2020)Lay TekchhayNoch keine Bewertungen

- SAP Human Resources: Personnel AdministrationDokument24 SeitenSAP Human Resources: Personnel AdministrationManzar AlamNoch keine Bewertungen

- 13 December 2017 Ordinary Council Meeting Agenda With Attachments RedactedDokument450 Seiten13 December 2017 Ordinary Council Meeting Agenda With Attachments Redactedjolyon AttwoollNoch keine Bewertungen

- 20190924TB PDFDokument40 Seiten20190924TB PDFdddibalNoch keine Bewertungen

- Integrating Personnel and Organizational Management in SAPDokument89 SeitenIntegrating Personnel and Organizational Management in SAPnaren_3456Noch keine Bewertungen

- 2022 HO 49 Labor Law Labor StandardsDokument10 Seiten2022 HO 49 Labor Law Labor Standardskat perezNoch keine Bewertungen

- Calculating Daily Rates and Monthly Salaries FairlyDokument3 SeitenCalculating Daily Rates and Monthly Salaries FairlyDerixk StarNoch keine Bewertungen

- ProjectDokument64 SeitenProjectkamsyNoch keine Bewertungen

- 19732ipcc CA Vol2 Cp3Dokument43 Seiten19732ipcc CA Vol2 Cp3PALADUGU MOUNIKANoch keine Bewertungen

- SC rules RA 9504 exemptions apply for full 2008Dokument38 SeitenSC rules RA 9504 exemptions apply for full 2008Darrel John SombilonNoch keine Bewertungen

- Cost Accounting - ch10Dokument33 SeitenCost Accounting - ch10Nur RezzaNoch keine Bewertungen

- Chapter 7 Employee BenefitsDokument21 SeitenChapter 7 Employee BenefitsPahrol RoziNoch keine Bewertungen

- Mba Iv, Ir-Gratuity ActDokument19 SeitenMba Iv, Ir-Gratuity Actmanu KartikayNoch keine Bewertungen

- Resolving A Wage Distortion DisputeDokument5 SeitenResolving A Wage Distortion DisputeLynette OmNoch keine Bewertungen

- MinimumwagesactDokument24 SeitenMinimumwagesactRamandeep KaurNoch keine Bewertungen

- Wage Code SummaryDokument7 SeitenWage Code Summaryqubrex1100% (1)

- Factories Act Working HoursDokument11 SeitenFactories Act Working HoursViraj SinghNoch keine Bewertungen

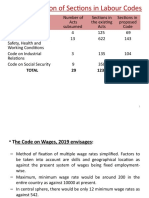

- Rationalization of Sections in Labour Codes: Total 29 1232 480Dokument49 SeitenRationalization of Sections in Labour Codes: Total 29 1232 480AadhityaNoch keine Bewertungen

- Metropolitan V NPWCDokument2 SeitenMetropolitan V NPWCGui EshNoch keine Bewertungen

- SJR 382Dokument5 SeitenSJR 382Thomas MatesNoch keine Bewertungen

- LaborDokument78 SeitenLaborReyes BeeNoch keine Bewertungen

- Compensation BCIDokument44 SeitenCompensation BCIBacquial, Phil Gio E. (Phil Gio)Noch keine Bewertungen

- PROJECT Final Vaishali MamDokument51 SeitenPROJECT Final Vaishali MamSanket MhetreNoch keine Bewertungen

- Payment of Gratuity ActDokument7 SeitenPayment of Gratuity ActUttaraVijayakumaranNoch keine Bewertungen

- Eagle Security v. NLRCDokument7 SeitenEagle Security v. NLRCApa MendozaNoch keine Bewertungen

- Cases. 12. III. D.2-5Dokument127 SeitenCases. 12. III. D.2-5Lecdiee Nhojiezz Tacissea SalnackyiNoch keine Bewertungen

- Labor Digest Summary: Univ of Pangasinan Faculty v. Univ of PangasinanDokument9 SeitenLabor Digest Summary: Univ of Pangasinan Faculty v. Univ of PangasinanKarla BeeNoch keine Bewertungen