Das könnte Ihnen auch gefallen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Exponential DistributionDokument20 SeitenExponential DistributionAhmar NiaziNoch keine Bewertungen

- The Use of Comminution Testwork Results in SAG Mill DesignDokument16 SeitenThe Use of Comminution Testwork Results in SAG Mill DesignLevent ErgunNoch keine Bewertungen

- Chemical Hazards IdentificationDokument29 SeitenChemical Hazards IdentificationarmdsfNoch keine Bewertungen

- FII Investement Trend - 2004-09 (India)Dokument4 SeitenFII Investement Trend - 2004-09 (India)Girish RamachandraNoch keine Bewertungen

- Zylog SystemsDokument2 SeitenZylog SystemsGirish RamachandraNoch keine Bewertungen

- When India Population Becomes An Asset and Not A LiabilityDokument2 SeitenWhen India Population Becomes An Asset and Not A LiabilityGirish RamachandraNoch keine Bewertungen

- Date or Subtitle: Spiderlogic OverviewDokument31 SeitenDate or Subtitle: Spiderlogic OverviewGirish RamachandraNoch keine Bewertungen

- Telecom Sector IndiaDokument11 SeitenTelecom Sector IndiaGirish RamachandraNoch keine Bewertungen

- India Steel SectorDokument8 SeitenIndia Steel SectorGirish RamachandraNoch keine Bewertungen

- BhartiAndMTN FinancialsDokument10 SeitenBhartiAndMTN FinancialsGirish RamachandraNoch keine Bewertungen

- BhartiAndMTN FinancialsDokument10 SeitenBhartiAndMTN FinancialsGirish RamachandraNoch keine Bewertungen

- Balance Sheet (2009-2000) - Wipro (US Format)Dokument16 SeitenBalance Sheet (2009-2000) - Wipro (US Format)Girish RamachandraNoch keine Bewertungen

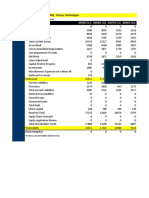

- Balance Sheet (2009-2000) - Infosys Technologies: All Numbers Are in INR and in x10MDokument18 SeitenBalance Sheet (2009-2000) - Infosys Technologies: All Numbers Are in INR and in x10MGirish RamachandraNoch keine Bewertungen

- Balance Sheet (2009-2003) of TCS (US Format)Dokument15 SeitenBalance Sheet (2009-2003) of TCS (US Format)Girish RamachandraNoch keine Bewertungen

- Balance Sheet (2009-2000) in US Format For Tata Motors: All Numbers Are in INR and in x10MDokument16 SeitenBalance Sheet (2009-2000) in US Format For Tata Motors: All Numbers Are in INR and in x10MGirish RamachandraNoch keine Bewertungen

- Balance Sheet (2009-2001) of Maruti Suzuki: All Numbers Are in INR and in x10MDokument16 SeitenBalance Sheet (2009-2001) of Maruti Suzuki: All Numbers Are in INR and in x10MGirish RamachandraNoch keine Bewertungen

- All Numbers Are in INR and in x10MDokument6 SeitenAll Numbers Are in INR and in x10MGirish RamachandraNoch keine Bewertungen

- Sensex To Touch 1800 in December 2009Dokument4 SeitenSensex To Touch 1800 in December 2009Girish RamachandraNoch keine Bewertungen

- Economics of Alternative Energy For IndiaDokument52 SeitenEconomics of Alternative Energy For IndiaGirish RamachandraNoch keine Bewertungen

- WhiteMonk HEG Equity Research ReportDokument15 SeitenWhiteMonk HEG Equity Research ReportGirish Ramachandra100% (1)

- Factor Analysis Source Code AppendixDokument20 SeitenFactor Analysis Source Code Appendixpratik zankeNoch keine Bewertungen

- Ual Project Proposal Year 1 Final ProductDokument7 SeitenUal Project Proposal Year 1 Final Productapi-531565793Noch keine Bewertungen

- Integrated Innovation and Hospitality Colleges, IncDokument7 SeitenIntegrated Innovation and Hospitality Colleges, IncJhoy MejaresNoch keine Bewertungen

- History of Campus Journalism in the PhilippinesDokument54 SeitenHistory of Campus Journalism in the PhilippinesRommel Angelo KirongNoch keine Bewertungen

- Submitted As Partial Fulfillment of Systemic Functional Linguistic Class AssignmentsDokument28 SeitenSubmitted As Partial Fulfillment of Systemic Functional Linguistic Class AssignmentsBhonechell GhokillNoch keine Bewertungen

- POMA - IM - Chapter 5Dokument28 SeitenPOMA - IM - Chapter 5Pham Phu Cuong B2108182Noch keine Bewertungen

- Jurnal Internasional Tentang ScabiesDokument9 SeitenJurnal Internasional Tentang ScabiesGalyNoch keine Bewertungen

- Supply Chain KPI-1-65Dokument65 SeitenSupply Chain KPI-1-65zinebNoch keine Bewertungen

- Good Thesis Statement About TechnologyDokument6 SeitenGood Thesis Statement About Technologybsr6hbaf100% (2)

- NCERT Solutions For Class 12th Maths Chapter 11 - Three Dimensional GeometryDokument51 SeitenNCERT Solutions For Class 12th Maths Chapter 11 - Three Dimensional Geometrydilip saxenaNoch keine Bewertungen

- MalladiDokument12 SeitenMalladiRaju VeluruNoch keine Bewertungen

- For Progress ReportDokument6 SeitenFor Progress ReportReine Chiara B. ConchaNoch keine Bewertungen

- Amity University Summer Internship Guidelines 2016-20Dokument31 SeitenAmity University Summer Internship Guidelines 2016-20Ilu Singh0% (1)

- Performance Appraisal Project of SAILDokument17 SeitenPerformance Appraisal Project of SAILHelpdesk81% (21)

- Patterns of Data Driven Decision Making - Apoorva R Oulkar & Atul MandalDokument8 SeitenPatterns of Data Driven Decision Making - Apoorva R Oulkar & Atul MandalAR OulkarNoch keine Bewertungen

- Dzurilla (1990) Development and Preliminary Evaluation of TheDokument8 SeitenDzurilla (1990) Development and Preliminary Evaluation of TheMourNoch keine Bewertungen

- 13 Calibration WassertheurerDokument7 Seiten13 Calibration WassertheurerYasmine AbbaouiNoch keine Bewertungen

- Final Synopsis On Food Adultreation and ControlDokument5 SeitenFinal Synopsis On Food Adultreation and ControlMohammad Bilal0% (1)

- Group A - Consolidated Article Critique - Managing Family Business TensionsDokument4 SeitenGroup A - Consolidated Article Critique - Managing Family Business TensionsRonelyCalairoNoch keine Bewertungen

- SotDokument74 SeitenSotvinna naralitaNoch keine Bewertungen

- Abatacept For Treatment of Adults Hospitalized With Moderate or Severe CovidDokument3 SeitenAbatacept For Treatment of Adults Hospitalized With Moderate or Severe CovidHoracioArizaNoch keine Bewertungen

- What I Have Learned: Activity 3 My Own Guide in Choosing A CareerDokument3 SeitenWhat I Have Learned: Activity 3 My Own Guide in Choosing A CareerJonrheym RemegiaNoch keine Bewertungen

- ANALYZE - The Influence of Social MediaDokument4 SeitenANALYZE - The Influence of Social MediaSvAnimeNoch keine Bewertungen

- Educational PsychologyDokument361 SeitenEducational PsychologyjalibkhanNoch keine Bewertungen

- 6 SigmaDokument13 Seiten6 SigmaThee BouyyNoch keine Bewertungen

- SW 3050 Miley Text Discussion Questions (For Reading Responses)Dokument6 SeitenSW 3050 Miley Text Discussion Questions (For Reading Responses)Ronie Enoc SugarolNoch keine Bewertungen