Das könnte Ihnen auch gefallen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Brief Therapy - A Problem Solving Model of ChangeDokument4 SeitenBrief Therapy - A Problem Solving Model of ChangeLameuneNoch keine Bewertungen

- Butterfly EconomicsDokument5 SeitenButterfly EconomicsLameuneNoch keine Bewertungen

- Eyde LandDokument54 SeitenEyde LandLameuneNoch keine Bewertungen

- Dispersion TradesDokument41 SeitenDispersion TradesLameune100% (1)

- A Course On Asymptotic Methods, Choice of Model in Regression and CausalityDokument1 SeiteA Course On Asymptotic Methods, Choice of Model in Regression and CausalityLameuneNoch keine Bewertungen

- Network of Options For International Coal & Freight BusinessesDokument20 SeitenNetwork of Options For International Coal & Freight BusinessesLameuneNoch keine Bewertungen

- Tristam ScottDokument24 SeitenTristam ScottLameuneNoch keine Bewertungen

- Pricing Storable Commodities and Associated Derivatives: Dorje C. BrodyDokument32 SeitenPricing Storable Commodities and Associated Derivatives: Dorje C. BrodyLameuneNoch keine Bewertungen

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDokument44 SeitenReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneNoch keine Bewertungen

- Andrea RoncoroniDokument27 SeitenAndrea RoncoroniLameuneNoch keine Bewertungen

- Day3 Session2B StoneDokument11 SeitenDay3 Session2B StoneLameuneNoch keine Bewertungen

- Commodity Hybrids Trading: James Groves, Barclays CapitalDokument21 SeitenCommodity Hybrids Trading: James Groves, Barclays CapitalLameuneNoch keine Bewertungen

- Jacob BeharallDokument19 SeitenJacob BeharallLameuneNoch keine Bewertungen

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDokument44 SeitenReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneNoch keine Bewertungen

- Valuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingDokument25 SeitenValuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingLameuneNoch keine Bewertungen

- Prmia 20111103 NyholmDokument24 SeitenPrmia 20111103 NyholmLameuneNoch keine Bewertungen

- Emmanuel GincbergDokument37 SeitenEmmanuel GincbergLameuneNoch keine Bewertungen

- Marcel ProkopczukDokument28 SeitenMarcel ProkopczukLameuneNoch keine Bewertungen

- Tristam ScottDokument24 SeitenTristam ScottLameuneNoch keine Bewertungen

- Day3 Session 2APaulDokument11 SeitenDay3 Session 2APaulLameuneNoch keine Bewertungen

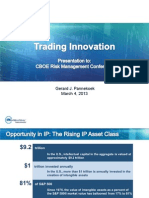

- Gerard J. Pannekoek March 4, 2013Dokument12 SeitenGerard J. Pannekoek March 4, 2013LameuneNoch keine Bewertungen

- Day3 Session 1BSternberg PresentationforWebDokument11 SeitenDay3 Session 1BSternberg PresentationforWebLameuneNoch keine Bewertungen

- Day1 Session3 ColeDokument36 SeitenDay1 Session3 ColeLameuneNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- 2202 Infantilization Essay - Quinn WilsonDokument11 Seiten2202 Infantilization Essay - Quinn Wilsonapi-283151250Noch keine Bewertungen

- FinTech and Banking DisruptionDokument13 SeitenFinTech and Banking DisruptionMaru MasNoch keine Bewertungen

- DHS/ICE (ICEPIC) Information Sharing Status: Enforcement Systems BranchDokument22 SeitenDHS/ICE (ICEPIC) Information Sharing Status: Enforcement Systems BranchImpello_TyrannisNoch keine Bewertungen

- Human Resource Management in The Hospitality Industry Is FullyDokument14 SeitenHuman Resource Management in The Hospitality Industry Is FullykiahNoch keine Bewertungen

- Course: Business Communication Course Code: COM 402 Submitted To: Mr. Nasirullah Khan Submission Date: 12Dokument18 SeitenCourse: Business Communication Course Code: COM 402 Submitted To: Mr. Nasirullah Khan Submission Date: 12Wahaj noor SiddiqueNoch keine Bewertungen

- CWTS Narrative ReportDokument10 SeitenCWTS Narrative ReportJa Rich100% (1)

- Scrabble Scrabble Is A Word Game in Which Two or Four Players Score Points by Placing Tiles, EachDokument4 SeitenScrabble Scrabble Is A Word Game in Which Two or Four Players Score Points by Placing Tiles, EachNathalie Faye De PeraltaNoch keine Bewertungen

- Services Marketing-Unit-Ii-ModifiedDokument48 SeitenServices Marketing-Unit-Ii-Modifiedshiva12mayNoch keine Bewertungen

- Stock Control Management SyestemDokument12 SeitenStock Control Management SyestemJohn YohansNoch keine Bewertungen

- Naskah IschialgiaDokument9 SeitenNaskah IschialgiaPuspo Wardoyo100% (1)

- Model Control System in Triforma: Mcs GuideDokument183 SeitenModel Control System in Triforma: Mcs GuideFabio SchiaffinoNoch keine Bewertungen

- EY Global Hospitality Insights 2016Dokument24 SeitenEY Global Hospitality Insights 2016Anonymous BkmsKXzwyKNoch keine Bewertungen

- Mechanical Engineering Research PapersDokument8 SeitenMechanical Engineering Research Papersfvfzfa5d100% (1)

- Polymer ConcreteDokument15 SeitenPolymer ConcreteHew LockNoch keine Bewertungen

- Working Capital Management by Birla GroupDokument39 SeitenWorking Capital Management by Birla GroupHajra ShahNoch keine Bewertungen

- US. Peace Corps Tetun Language CourseDokument305 SeitenUS. Peace Corps Tetun Language CoursePeter W Gossner100% (1)

- Learn Spoken English QuicklyDokument20 SeitenLearn Spoken English QuicklyPoulami DeNoch keine Bewertungen

- Amazon PrimeDokument27 SeitenAmazon PrimeMohamedNoch keine Bewertungen

- Archive Purge Programs in Oracle EBS R12Dokument7 SeitenArchive Purge Programs in Oracle EBS R12Pritesh MoganeNoch keine Bewertungen

- MLHP Final ListDokument36 SeitenMLHP Final Listswapnitha tummaNoch keine Bewertungen

- Flokulan Air Limbah PDFDokument21 SeitenFlokulan Air Limbah PDFanggunNoch keine Bewertungen

- 5 Example of Intensive Pronoun in SentenceDokument2 Seiten5 Example of Intensive Pronoun in SentenceRaúl Javier Gambe CapoteNoch keine Bewertungen

- Research ProposalDokument14 SeitenResearch ProposalMhal Dane DinglasaNoch keine Bewertungen

- FSU7533 Digital Marketing & Social Media Career Advancement Certification (Including Voucher) ETPDokument2 SeitenFSU7533 Digital Marketing & Social Media Career Advancement Certification (Including Voucher) ETPcNoch keine Bewertungen

- Odyssey Marine Exploration, Inc. v. The Unidentified, Shipwrecked Vessel or Vessels - Document No. 3Dokument11 SeitenOdyssey Marine Exploration, Inc. v. The Unidentified, Shipwrecked Vessel or Vessels - Document No. 3Justia.comNoch keine Bewertungen

- RPS Spare CatalogDokument25 SeitenRPS Spare Catalogसुरेश चंद Suresh ChandNoch keine Bewertungen

- Silent Reading With Graph1Dokument2 SeitenSilent Reading With Graph1JonaldSamueldaJoseNoch keine Bewertungen

- Discuss Both Views Introduction PracticeDokument3 SeitenDiscuss Both Views Introduction PracticeSang NguyễnNoch keine Bewertungen

- Entrep 1st PerioDokument5 SeitenEntrep 1st PerioMargarette FajardoNoch keine Bewertungen

- Preview ISO+15613-2004Dokument6 SeitenPreview ISO+15613-2004Brijith0% (1)