Das könnte Ihnen auch gefallen

- A Brief History of Panics and Their Periodical Occurrence in the United StatesVon EverandA Brief History of Panics and Their Periodical Occurrence in the United StatesNoch keine Bewertungen

- Wide Moat Investing - CFA Cleveland May 2016Dokument40 SeitenWide Moat Investing - CFA Cleveland May 2016Jeff TargaryaenNoch keine Bewertungen

- Klarman Yield PigDokument2 SeitenKlarman Yield Pigalexg6Noch keine Bewertungen

- Hayman Bass 20081017Dokument3 SeitenHayman Bass 20081017dylan555100% (1)

- Austrian Economics & InvestingDokument20 SeitenAustrian Economics & InvestingRaj KumarNoch keine Bewertungen

- Decision-Making For Investors: Theory, Practice, and PitfallsDokument20 SeitenDecision-Making For Investors: Theory, Practice, and PitfallsGaurav JainNoch keine Bewertungen

- Keynes Investment LessonsDokument5 SeitenKeynes Investment LessonskwongNoch keine Bewertungen

- Amitabh Singhvi L MOI Interview L JUNE-2011Dokument6 SeitenAmitabh Singhvi L MOI Interview L JUNE-2011Wayne GonsalvesNoch keine Bewertungen

- Aquamarine Fund PresentationDokument25 SeitenAquamarine Fund PresentationVijay MalikNoch keine Bewertungen

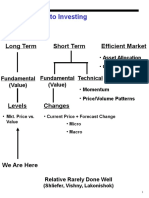

- Approaches To Investing: Long Term Short Term Efficient MarketDokument71 SeitenApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeNoch keine Bewertungen

- Investing classics & business biographiesDokument2 SeitenInvesting classics & business biographiesdanawhite2Noch keine Bewertungen

- Tobin - Commercial Banks As Creators of MoneyDokument12 SeitenTobin - Commercial Banks As Creators of MoneyJung ZorndikeNoch keine Bewertungen

- Lisa Rapuano Finding Your Way Along The Many Paths of ValueDokument29 SeitenLisa Rapuano Finding Your Way Along The Many Paths of ValueValueWalk100% (1)

- Stephen Hawking and The Prophets of A Scientific AgeDokument17 SeitenStephen Hawking and The Prophets of A Scientific Agebhav2501100% (1)

- Bob Robotti - Navigating Deep WatersDokument35 SeitenBob Robotti - Navigating Deep WatersCanadianValueNoch keine Bewertungen

- Graham - Doddsville - Issue 40 - v19 PDFDokument61 SeitenGraham - Doddsville - Issue 40 - v19 PDFRofiq 4 NugrohoNoch keine Bewertungen

- Tiananmen Square To Wall Street - ArticleDokument3 SeitenTiananmen Square To Wall Street - ArticleGabe FarajollahNoch keine Bewertungen

- Boyar's Intrinsic Value Research Forgotten FourtyDokument49 SeitenBoyar's Intrinsic Value Research Forgotten FourtyValueWalk100% (1)

- Guru Focus Interview With Arnold VandenbergDokument16 SeitenGuru Focus Interview With Arnold VandenbergVu Latticework Poet100% (2)

- Transcription of David Tepper's 2007 Presentation to Carnegie Mellon Undergraduate StudentsDokument7 SeitenTranscription of David Tepper's 2007 Presentation to Carnegie Mellon Undergraduate StudentsPattyPattersonNoch keine Bewertungen

- Mahony - Soros S SecretsDokument2 SeitenMahony - Soros S SecretssimvanonNoch keine Bewertungen

- Warren Buffett's Case Study in Mid-Continent Tabulating CompanyDokument19 SeitenWarren Buffett's Case Study in Mid-Continent Tabulating CompanyAhmad DamasantoNoch keine Bewertungen

- Dylan Grice - GoodbyeDokument7 SeitenDylan Grice - Goodbyevineet_bmNoch keine Bewertungen

- AVM Ranger Returns 29.1% in 2016Dokument6 SeitenAVM Ranger Returns 29.1% in 2016ChrisNoch keine Bewertungen

- Murray Stahl Discusses Value Investing Approach and Top Stock IdeasDokument10 SeitenMurray Stahl Discusses Value Investing Approach and Top Stock IdeaskdwcapitalNoch keine Bewertungen

- Graham Doddsville Issue 24Dokument61 SeitenGraham Doddsville Issue 24CanadianValueNoch keine Bewertungen

- Max Heine Forbes March 29 1982Dokument2 SeitenMax Heine Forbes March 29 1982jkusnan3341100% (2)

- George Soros - Reflections On The Crash of 2008 and What It Means - An Ebook Update To The New Paradigm For Financial Markets PDFDokument88 SeitenGeorge Soros - Reflections On The Crash of 2008 and What It Means - An Ebook Update To The New Paradigm For Financial Markets PDFJoao Alves Monteiro NetoNoch keine Bewertungen

- Aquamarine - 2013Dokument84 SeitenAquamarine - 2013sb86Noch keine Bewertungen

- Ed Thorp - A Mathematician on Wall StreetDokument3 SeitenEd Thorp - A Mathematician on Wall StreetgjangNoch keine Bewertungen

- Graham Doddsville Issue 31 0Dokument37 SeitenGraham Doddsville Issue 31 0marketfolly.comNoch keine Bewertungen

- The Boom of 2021Dokument4 SeitenThe Boom of 2021Jeff McGinnNoch keine Bewertungen

- Hedge Papers No.6: Daniel LoebDokument21 SeitenHedge Papers No.6: Daniel LoebHedge Clippers100% (1)

- Who's A Pretty Boy Then? or Beauty Contests, Rationality and Greater FoolsDokument16 SeitenWho's A Pretty Boy Then? or Beauty Contests, Rationality and Greater FoolsOld School ValueNoch keine Bewertungen

- Graham and Doddsville - Issue 9 - Spring 2010Dokument33 SeitenGraham and Doddsville - Issue 9 - Spring 2010g4nz0Noch keine Bewertungen

- HBR Article Explains Increasing Returns and Two Worlds of BusinessDokument11 SeitenHBR Article Explains Increasing Returns and Two Worlds of BusinessLuis Gonzalo Trigo SotoNoch keine Bewertungen

- Edition 1Dokument2 SeitenEdition 1Angelia ThomasNoch keine Bewertungen

- Daily Journal Meeting Detailed Notes From Charlie MungerDokument29 SeitenDaily Journal Meeting Detailed Notes From Charlie MungerGary Ribe100% (1)

- How Open Societies Can Stabilize CapitalismDokument5 SeitenHow Open Societies Can Stabilize CapitalismShaun FantauzzoNoch keine Bewertungen

- Thomas Russo: Global Value Investing - Richard Ivey School of Business, 2013Dokument34 SeitenThomas Russo: Global Value Investing - Richard Ivey School of Business, 2013Hedge Fund ConversationsNoch keine Bewertungen

- ONE-WAY POCKETS: The Book of Books on Wall Street SpeculationVon EverandONE-WAY POCKETS: The Book of Books on Wall Street SpeculationNoch keine Bewertungen

- Seasonal Stock Market Trends: The Definitive Guide to Calendar-Based Stock Market TradingVon EverandSeasonal Stock Market Trends: The Definitive Guide to Calendar-Based Stock Market TradingNoch keine Bewertungen

- 8th Annual New York: Value Investing CongressDokument46 Seiten8th Annual New York: Value Investing CongressVALUEWALK LLCNoch keine Bewertungen

- Debunkery (Review and Analysis of Fisher and Hoffmans' Book)Von EverandDebunkery (Review and Analysis of Fisher and Hoffmans' Book)Noch keine Bewertungen

- Popular Delusions Issue December 2019 PDFDokument16 SeitenPopular Delusions Issue December 2019 PDFfx2009Noch keine Bewertungen

- Graham & Doddsville - Issue 15 - Spring 2012Dokument64 SeitenGraham & Doddsville - Issue 15 - Spring 2012Filipe DurandNoch keine Bewertungen

- Marcato Capital 4Q14 Letter To InvestorsDokument38 SeitenMarcato Capital 4Q14 Letter To InvestorsValueWalk100% (1)

- Summary of Marc Levinson's The Great A&P And The Struggle For Small Business In AmericaVon EverandSummary of Marc Levinson's The Great A&P And The Struggle For Small Business In AmericaNoch keine Bewertungen

- High Conviction Barrons Talks With RiverParkWedgewood Fund Portfolio Manager David RolfeDokument3 SeitenHigh Conviction Barrons Talks With RiverParkWedgewood Fund Portfolio Manager David RolfebernhardfNoch keine Bewertungen

- Benjamin Graham's Impact on the Financial Analysis ProfessionDokument1 SeiteBenjamin Graham's Impact on the Financial Analysis Professionpjs15Noch keine Bewertungen

- The Successful InvestorDokument12 SeitenThe Successful InvestorRahul Ohri100% (1)

- Distressed Debt InvestingDokument5 SeitenDistressed Debt Investingjt322Noch keine Bewertungen

- From The Bronx To Wall Street: My Fifty Years in Finance and PhilanthropyVon EverandFrom The Bronx To Wall Street: My Fifty Years in Finance and PhilanthropyNoch keine Bewertungen

- Brian Spector Leaving Baupost Letter - Business InsiderDokument4 SeitenBrian Spector Leaving Baupost Letter - Business InsiderHedge Fund ConversationsNoch keine Bewertungen

- Grant's Interest Rate Observer X-Mas IssueDokument27 SeitenGrant's Interest Rate Observer X-Mas IssueCanadianValueNoch keine Bewertungen

- Distressed Debt Investing: Seth KlarmanDokument5 SeitenDistressed Debt Investing: Seth Klarmanjt322Noch keine Bewertungen

- Siegal CAPEDokument10 SeitenSiegal CAPEJeffrey WilliamsNoch keine Bewertungen

- CLR 2 Review of SpitznagelDokument8 SeitenCLR 2 Review of SpitznagelAnonymous HtDbszqtNoch keine Bewertungen

- Short Selling: Strategies, Risks, and RewardsVon EverandShort Selling: Strategies, Risks, and RewardsBewertung: 4.5 von 5 Sternen4.5/5 (2)

- 1987 Washington Post Article On Lou SimpsonDokument4 Seiten1987 Washington Post Article On Lou SimpsonAdrian KachmarNoch keine Bewertungen

- 2013.03 - NYSSA - Pres by Insurance Info Inst PDFDokument168 Seiten2013.03 - NYSSA - Pres by Insurance Info Inst PDFAdrian KachmarNoch keine Bewertungen

- 2007.01.22 - VF Corp - Mackey McDonald WSJ InterviewDokument5 Seiten2007.01.22 - VF Corp - Mackey McDonald WSJ InterviewAdrian KachmarNoch keine Bewertungen

- 2011 - 16 Minetta Lane Sales BrochureDokument20 Seiten2011 - 16 Minetta Lane Sales BrochureAdrian KachmarNoch keine Bewertungen

- KYC checklist for filling formDokument35 SeitenKYC checklist for filling formAjay Kumar MattupalliNoch keine Bewertungen

- Interim Report On Devolved GovernmentDokument341 SeitenInterim Report On Devolved GovernmentSpartacus OwinoNoch keine Bewertungen

- EF2A1 HDT Budget Upto Direct Taxes PCB4 1629376359978Dokument30 SeitenEF2A1 HDT Budget Upto Direct Taxes PCB4 1629376359978Mamta Patel100% (1)

- AnnualReport 2016-17Dokument232 SeitenAnnualReport 2016-17arunNoch keine Bewertungen

- Assignment PDFDokument31 SeitenAssignment PDFjjNoch keine Bewertungen

- Paper Accountingandcultureandmarket Zarzeski 1996.Dokument20 SeitenPaper Accountingandcultureandmarket Zarzeski 1996.SorayaNoch keine Bewertungen

- RFBT-04: LAW ON Credit Transactions: - T R S ADokument10 SeitenRFBT-04: LAW ON Credit Transactions: - T R S AAdan Nada100% (1)

- Republic of Austria Investor Information PDFDokument48 SeitenRepublic of Austria Investor Information PDFMi JpNoch keine Bewertungen

- KPMG Nppa New Payments Platform Minimising Payments FraudDokument16 SeitenKPMG Nppa New Payments Platform Minimising Payments FrauddavemacbrainNoch keine Bewertungen

- Analysis and Interpretation of Financial Statements: Christine Talimongan ABM - BezosDokument37 SeitenAnalysis and Interpretation of Financial Statements: Christine Talimongan ABM - BezostineNoch keine Bewertungen

- Rothschild in Japan: Expert Advisory Services and Landmark DealsDokument4 SeitenRothschild in Japan: Expert Advisory Services and Landmark DealsTiago PinheiroNoch keine Bewertungen

- SPT PPH BDN 2009 English OrtaxDokument29 SeitenSPT PPH BDN 2009 English OrtaxCoba SajaNoch keine Bewertungen

- Income StatementsDokument23 SeitenIncome StatementsJuan FrivaldoNoch keine Bewertungen

- Risk Management Options and DerivativesDokument13 SeitenRisk Management Options and DerivativesAbdu0% (1)

- Barrons 3.8Dokument3 SeitenBarrons 3.8alireza shahinNoch keine Bewertungen

- Chapter 4 Assignment Recording TransactionsDokument6 SeitenChapter 4 Assignment Recording TransactionsjepsyutNoch keine Bewertungen

- SyllabusDokument45 SeitenSyllabusPrachi PNoch keine Bewertungen

- A Project Report On TaxationDokument71 SeitenA Project Report On TaxationHveeeeNoch keine Bewertungen

- EquityDokument29 SeitenEquityThuy Linh DoNoch keine Bewertungen

- Booklet 2Dokument127 SeitenBooklet 2alok pandeyNoch keine Bewertungen

- The Asian Financial Crisis of 1997 1998 Revisited Causes Recovery and The Path Going ForwardDokument10 SeitenThe Asian Financial Crisis of 1997 1998 Revisited Causes Recovery and The Path Going Forwardgreenam 14Noch keine Bewertungen

- Investment Decision MakingDokument16 SeitenInvestment Decision MakingDhruvNoch keine Bewertungen

- Multinational Capital BudgetingDokument20 SeitenMultinational Capital BudgetingBibiNoch keine Bewertungen

- International Taxation of Hybrid EntitiesDokument11 SeitenInternational Taxation of Hybrid EntitiesNilormi MukherjeeNoch keine Bewertungen

- TCCB Revision - ProblemsDokument4 SeitenTCCB Revision - ProblemsDiễm Quỳnh 1292 Vũ ĐặngNoch keine Bewertungen

- Accounts - Past Years Que CompilationDokument393 SeitenAccounts - Past Years Que CompilationSavya SachiNoch keine Bewertungen

- SBI Focused Equity Fund (1) 09162022Dokument4 SeitenSBI Focused Equity Fund (1) 09162022chandana kumarNoch keine Bewertungen

- Day 3 PDFDokument14 SeitenDay 3 PDFDinesh GadkariNoch keine Bewertungen

- Case Study Currency SwapsDokument2 SeitenCase Study Currency SwapsSourav Maity100% (2)

- 2014 Tax TablesDokument1 Seite2014 Tax Tableszimbo2Noch keine Bewertungen