Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Jeankeat TreatiseDokument96 SeitenJeankeat Treatisereadit777100% (9)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- 5 - Corporate Governance AmendedDokument24 Seiten5 - Corporate Governance AmendednurhoneyzNoch keine Bewertungen

- AgileDokument2 SeitenAgileRitesh Kumar PatroNoch keine Bewertungen

- Business IntelligenceDokument2 SeitenBusiness IntelligenceRitesh Kumar PatroNoch keine Bewertungen

- Indian Depository ReceiptDokument9 SeitenIndian Depository ReceiptRitesh Kumar PatroNoch keine Bewertungen

- Kotakbank ChartDokument1 SeiteKotakbank ChartRitesh Kumar PatroNoch keine Bewertungen

- Value Research Online: The Calculations Are Based On Sips Made On The 1St of Every MonthDokument2 SeitenValue Research Online: The Calculations Are Based On Sips Made On The 1St of Every MonthRitesh Kumar PatroNoch keine Bewertungen

- Education Loan Amortization Table: Month EMI Amount (RS) Interest Amount (RS) Principal Reduction (RS) Balance Due (RS)Dokument4 SeitenEducation Loan Amortization Table: Month EMI Amount (RS) Interest Amount (RS) Principal Reduction (RS) Balance Due (RS)Ritesh Kumar PatroNoch keine Bewertungen

- Mnutes of Meeting - 1Dokument3 SeitenMnutes of Meeting - 1Ritesh Kumar PatroNoch keine Bewertungen

- Layout of HospitalDokument11 SeitenLayout of HospitalRitesh Kumar PatroNoch keine Bewertungen

- Urban Housing PresentationDokument27 SeitenUrban Housing PresentationRitesh Kumar Patro0% (1)

- Ritesh ResumeDokument2 SeitenRitesh ResumeRitesh Kumar PatroNoch keine Bewertungen

- Roles and Responsibilities of Central ManagementDokument13 SeitenRoles and Responsibilities of Central ManagementManmohanNoch keine Bewertungen

- Accounts ProjectDokument33 SeitenAccounts Projectaradhana chauhanNoch keine Bewertungen

- Imron Sahid NugrohoDokument7 SeitenImron Sahid NugrohoAnanda LukmanNoch keine Bewertungen

- Arcelor Undervaluation CaseDokument19 SeitenArcelor Undervaluation CaseJerry K Floater100% (1)

- Jetblue's Case Study by P.rai87@gmailDokument25 SeitenJetblue's Case Study by P.rai87@gmailPRAVEEN RAI67% (3)

- Millicon InternationalDokument18 SeitenMillicon InternationalDanielZambranoNoch keine Bewertungen

- Port Folio Number 2007 MASDokument8 SeitenPort Folio Number 2007 MASSasa LuNoch keine Bewertungen

- Costs of An Initial Public Offering-Grant ThorntonDokument7 SeitenCosts of An Initial Public Offering-Grant ThorntonSS CORPORATE SERVICESNoch keine Bewertungen

- Eight Best CandlesDokument4 SeitenEight Best CandlesJonathan DominguezNoch keine Bewertungen

- BO2 Case Digests 021212Dokument8 SeitenBO2 Case Digests 021212kumag2Noch keine Bewertungen

- 12 Entrepreneurship SP 1Dokument15 Seiten12 Entrepreneurship SP 1Ashish GangwalNoch keine Bewertungen

- STB Ar2015 en 1 PDFDokument272 SeitenSTB Ar2015 en 1 PDFHòa Trần VănNoch keine Bewertungen

- KKR Investor UpdateDokument8 SeitenKKR Investor Updatepucci23Noch keine Bewertungen

- TUI UniversityDokument9 SeitenTUI UniversityChris NailonNoch keine Bewertungen

- Pocket Money Course Material-MarathiDokument81 SeitenPocket Money Course Material-MarathiAbhieshek P GodhaNoch keine Bewertungen

- Analysis - Why Investing in PSUs Is A Good Idea - MoneycontrolDokument2 SeitenAnalysis - Why Investing in PSUs Is A Good Idea - Moneycontrollaloo01Noch keine Bewertungen

- No. 3 Mercantile Bar 2017Dokument2 SeitenNo. 3 Mercantile Bar 2017Venice SantibanezNoch keine Bewertungen

- Management Management Management ManagementDokument94 SeitenManagement Management Management Managementalizah khadarooNoch keine Bewertungen

- The Corporation Code ReviewerDokument28 SeitenThe Corporation Code Reviewernoorlaw100% (4)

- 2GO Group, Inc. - SMIC SEC Form 19-1 (Tender Offer Report) (Copy Furnished 2GO) 22march2021Dokument69 Seiten2GO Group, Inc. - SMIC SEC Form 19-1 (Tender Offer Report) (Copy Furnished 2GO) 22march2021Roze JustinNoch keine Bewertungen

- SelectedGlobalStocks - February 1 2017Dokument5 SeitenSelectedGlobalStocks - February 1 2017Tiso Blackstar GroupNoch keine Bewertungen

- Reliance Infrastructure 091113 01Dokument4 SeitenReliance Infrastructure 091113 01Vishakha KhannaNoch keine Bewertungen

- Case Study Barclays FinalDokument13 SeitenCase Study Barclays FinalShalini Senglo RajaNoch keine Bewertungen

- Barbeque Nation Hospitality Limited DRHP CompressedDokument515 SeitenBarbeque Nation Hospitality Limited DRHP Compressedsiddhant kohliNoch keine Bewertungen

- Ments Questions Corp-LawDokument7 SeitenMents Questions Corp-LawIan Ray PaglinawanNoch keine Bewertungen

- Intermediate Financial Accounting Part 1b by Zeus Millan Compress - CompressDokument174 SeitenIntermediate Financial Accounting Part 1b by Zeus Millan Compress - CompresswalsondevNoch keine Bewertungen

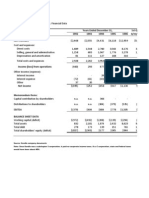

- Exhibit 1 Kendle International Inc. Financial Data Years Ended December 31Dokument12 SeitenExhibit 1 Kendle International Inc. Financial Data Years Ended December 31Kito Minying ChenNoch keine Bewertungen

- Session 2 - Board Effectiveness v1 - Chris RazookDokument29 SeitenSession 2 - Board Effectiveness v1 - Chris RazookEra HRNoch keine Bewertungen