Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Greenlight UnlockedDokument7 SeitenGreenlight UnlockedZerohedgeNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- 'Long Term or Confidential (KIG Special) 2015Dokument12 Seiten'Long Term or Confidential (KIG Special) 2015CanadianValueNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- Stan Druckenmiller Sohn TranscriptDokument8 SeitenStan Druckenmiller Sohn Transcriptmarketfolly.com100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Stan Druckenmiller The Endgame SohnDokument10 SeitenStan Druckenmiller The Endgame SohnCanadianValueNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- OakTree Real EstateDokument13 SeitenOakTree Real EstateCanadianValue100% (1)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- 2015 q4 Crescent Webcast For Website With WatermarkDokument38 Seiten2015 q4 Crescent Webcast For Website With WatermarkCanadianValueNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500Dokument6 SeitenThe Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500dpbasicNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Charlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFDokument18 SeitenCharlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFaakashshah85Noch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- KaseFundannualletter 2015Dokument20 SeitenKaseFundannualletter 2015CanadianValueNoch keine Bewertungen

- Fpa Crescent FundDokument51 SeitenFpa Crescent FundCanadianValueNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Fairholme 2016 Investor Call TranscriptDokument20 SeitenFairholme 2016 Investor Call TranscriptCanadianValueNoch keine Bewertungen

- Market Macro Myths Debts Deficits and DelusionsDokument13 SeitenMarket Macro Myths Debts Deficits and DelusionsCanadianValueNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Tilson March 2016 Berkshire ValuationDokument26 SeitenTilson March 2016 Berkshire ValuationCanadianValue100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Hussman Funds Semi-Annual ReportDokument84 SeitenHussman Funds Semi-Annual ReportCanadianValueNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- Munger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16Dokument12 SeitenMunger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16CanadianValueNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- UDF Overview Presentation 1-28-16Dokument18 SeitenUDF Overview Presentation 1-28-16CanadianValueNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Gmo Quarterly LetterDokument26 SeitenGmo Quarterly LetterCanadianValueNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- Weitz - 4Q2015 Analyst CornerDokument2 SeitenWeitz - 4Q2015 Analyst CornerCanadianValueNoch keine Bewertungen

- 2015Q3 Webcast Transcript LLDokument26 Seiten2015Q3 Webcast Transcript LLCanadianValueNoch keine Bewertungen

- Einhorn Consol PresentationDokument107 SeitenEinhorn Consol PresentationCanadianValueNoch keine Bewertungen

- Einhorn Q4 2015Dokument7 SeitenEinhorn Q4 2015CanadianValueNoch keine Bewertungen

- IEP Aug 2015 - Investor Presentation FINALDokument41 SeitenIEP Aug 2015 - Investor Presentation FINALCanadianValueNoch keine Bewertungen

- Hayman Capital Management LP - Clovis Oncology Inc VFINAL HarvestDokument20 SeitenHayman Capital Management LP - Clovis Oncology Inc VFINAL HarvestCanadianValue100% (1)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Einhorn Consol PresentationDokument107 SeitenEinhorn Consol PresentationCanadianValueNoch keine Bewertungen

- Kase Q3&Oct 15 LtrsDokument21 SeitenKase Q3&Oct 15 LtrsCanadianValueNoch keine Bewertungen

- Whitney Tilson Favorite Long and Short IdeasDokument103 SeitenWhitney Tilson Favorite Long and Short IdeasCanadianValueNoch keine Bewertungen

- Steve Romick FPA Crescent Fund Q3 Investor PresentationDokument32 SeitenSteve Romick FPA Crescent Fund Q3 Investor PresentationCanadianValue100% (1)

- Investors Title InsuranceDokument55 SeitenInvestors Title InsuranceCanadianValueNoch keine Bewertungen

- Fpa Crescent Fund (Fpacx)Dokument46 SeitenFpa Crescent Fund (Fpacx)CanadianValueNoch keine Bewertungen

- PTS Morning Call 12-14-09Dokument4 SeitenPTS Morning Call 12-14-09PrismtradingschoolNoch keine Bewertungen

- Stock Market IndicesDokument15 SeitenStock Market IndicesSIdhu SimmiNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- WSJ - Li Lu ProfileDokument5 SeitenWSJ - Li Lu ProfilezemblaNoch keine Bewertungen

- Joint VentureDokument2 SeitenJoint VentureAries Gonzales CaraganNoch keine Bewertungen

- IFFSSAFinal Report 2 May 22Dokument133 SeitenIFFSSAFinal Report 2 May 22Tom CochranNoch keine Bewertungen

- Cup 1 FA 1 and FA 2Dokument16 SeitenCup 1 FA 1 and FA 2Thony Danielle LabradorNoch keine Bewertungen

- OFOD7 e Test Bank CH 03Dokument2 SeitenOFOD7 e Test Bank CH 03Danny NgNoch keine Bewertungen

- Fipb Review 2011-13Dokument100 SeitenFipb Review 2011-13mailnevadaNoch keine Bewertungen

- Fsa Practical Record ProblemsDokument12 SeitenFsa Practical Record ProblemsPriyanka GuptaNoch keine Bewertungen

- Recession Normal ExpansionDokument3 SeitenRecession Normal ExpansionAshish BhallaNoch keine Bewertungen

- Annexure 2Dokument13 SeitenAnnexure 2Shalini SrivastavNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Investors Perception Towards Real Estate InvestmentDokument38 SeitenInvestors Perception Towards Real Estate InvestmentMohd Fahd Kapadia25% (4)

- LCCI Level I (Book-Keeping) : Course OutlineDokument5 SeitenLCCI Level I (Book-Keeping) : Course OutlineGergana DraganovaNoch keine Bewertungen

- Chapter 4 Financial Statement AnalysisDokument7 SeitenChapter 4 Financial Statement AnalysisAnnaNoch keine Bewertungen

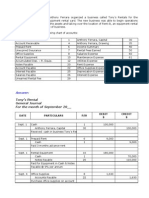

- Tony's Rentals General Journal For September 20Dokument17 SeitenTony's Rentals General Journal For September 20Rehan Mehmood63% (8)

- Jawaban Buku ALK Subramanyam Bab 7Dokument8 SeitenJawaban Buku ALK Subramanyam Bab 7Must Joko100% (1)

- T1 Importance of Mutual FundsDokument2 SeitenT1 Importance of Mutual Fundsharsh agarwalNoch keine Bewertungen

- Prob Set 1Dokument6 SeitenProb Set 1Nikki BulanteNoch keine Bewertungen

- Mosaic - Perspectives On Investing Download - Tìm Với GoogleDokument2 SeitenMosaic - Perspectives On Investing Download - Tìm Với GooglefdsafasfNoch keine Bewertungen

- To Analyze The Financial Performance of Axis Bank by Using RatiosDokument16 SeitenTo Analyze The Financial Performance of Axis Bank by Using RatiosPrasad S. NayakNoch keine Bewertungen

- 57-The Last-Hour Trading Technique PDFDokument4 Seiten57-The Last-Hour Trading Technique PDFNavin Chandar100% (1)

- Liquidity, Risk and Profitability AnalysisDokument13 SeitenLiquidity, Risk and Profitability AnalysisMichael Neal100% (1)

- Capital Adequacy Ratio - Wikipedia, The Free EncyclopediaDokument4 SeitenCapital Adequacy Ratio - Wikipedia, The Free EncyclopediaTrần Kim ChungNoch keine Bewertungen

- COST OF CAPITAL - Basic FinanceDokument21 SeitenCOST OF CAPITAL - Basic FinanceAqib IshtiaqNoch keine Bewertungen

- Acca Paper F3 Financial Accounting Mock Exam Prepared By: MR Yeo Hong AnnDokument23 SeitenAcca Paper F3 Financial Accounting Mock Exam Prepared By: MR Yeo Hong AnnRajeshwar Nagaisar50% (2)

- Profitable Short Term Trading StrategiesDokument196 SeitenProfitable Short Term Trading Strategiessupriya79% (29)

- Topic 30 Cross Reference To GARP Assigned Reading - The Institute For Financial Markets, Chapter 1Dokument1 SeiteTopic 30 Cross Reference To GARP Assigned Reading - The Institute For Financial Markets, Chapter 1Rehan GanatraNoch keine Bewertungen

- Dhana - Accounting For Managers - Ass1Dokument7 SeitenDhana - Accounting For Managers - Ass1Kiran Kumar MCNoch keine Bewertungen

- BA544 Chap 008Dokument50 SeitenBA544 Chap 008Abhay AgrawalNoch keine Bewertungen

- StockholdersDokument458 SeitenStockholdersMica Joy FajardoNoch keine Bewertungen

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaVon EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaBewertung: 3.5 von 5 Sternen3.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaVon EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaBewertung: 4.5 von 5 Sternen4.5/5 (14)

- Joy of Agility: How to Solve Problems and Succeed SoonerVon EverandJoy of Agility: How to Solve Problems and Succeed SoonerBewertung: 4 von 5 Sternen4/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialVon EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNoch keine Bewertungen

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistVon EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistBewertung: 4.5 von 5 Sternen4.5/5 (73)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsVon EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNoch keine Bewertungen