Das könnte Ihnen auch gefallen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

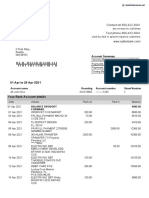

- Sutton Bank StatementDokument2 SeitenSutton Bank StatementNadiia AvetisianNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Social Game Studies: A Workshop ReportDokument35 SeitenSocial Game Studies: A Workshop ReportSebastian Deterding100% (1)

- Bank Interview QuestionsDokument8 SeitenBank Interview Questionsfyod100% (1)

- Suture ManufacturerDokument7 SeitenSuture ManufacturerVishal ThakkarNoch keine Bewertungen

- Garage Locator PDFDokument134 SeitenGarage Locator PDFMCS SBINoch keine Bewertungen

- Final ProjectDokument23 SeitenFinal ProjectsahilsardanaNoch keine Bewertungen

- RENAULT InternshipDokument32 SeitenRENAULT InternshipSushil kumarNoch keine Bewertungen

- Project Profile ON Roasted Rice FlakesDokument7 SeitenProject Profile ON Roasted Rice FlakesPrafulla ChandraNoch keine Bewertungen

- Ikhlayel 2018Dokument41 SeitenIkhlayel 2018Biswajit Debnath OffcNoch keine Bewertungen

- Double Taxation Relief: Tax SupplementDokument5 SeitenDouble Taxation Relief: Tax SupplementlalitbhatiNoch keine Bewertungen

- West Jet Encore Porter 5 Forces AnalysisDokument4 SeitenWest Jet Encore Porter 5 Forces Analysisle duyNoch keine Bewertungen

- 2023 - Forecast George FriedmanDokument17 Seiten2023 - Forecast George FriedmanGeorge BestNoch keine Bewertungen

- A Study On Customer Satisfaction Towards Idbi Fortis Life Insurance Company Ltd.Dokument98 SeitenA Study On Customer Satisfaction Towards Idbi Fortis Life Insurance Company Ltd.Md MubashirNoch keine Bewertungen

- Tanzania Mortgage Market Update 2014Dokument7 SeitenTanzania Mortgage Market Update 2014Anonymous FnM14a0Noch keine Bewertungen

- Annexure V Bidder Response SheetDokument2 SeitenAnnexure V Bidder Response SheetAshishNoch keine Bewertungen

- Managerial EconomicsDokument3 SeitenManagerial EconomicsBhavani Singh Rathore100% (2)

- KONTRAK KERJA 2 BahasaDokument12 SeitenKONTRAK KERJA 2 BahasaStanley RusliNoch keine Bewertungen

- CH 16Dokument7 SeitenCH 16shabirishaq141Noch keine Bewertungen

- Avtex W270TSDokument1 SeiteAvtex W270TSAre GeeNoch keine Bewertungen

- Registration of PropertyDokument13 SeitenRegistration of PropertyambonulanNoch keine Bewertungen

- RMC 17-02Dokument4 SeitenRMC 17-02racheltanuy6557Noch keine Bewertungen

- Why Europe Planned The Great Bank RobberyDokument2 SeitenWhy Europe Planned The Great Bank RobberyRakesh SimhaNoch keine Bewertungen

- Country Ranking Analysis TemplateDokument12 SeitenCountry Ranking Analysis Templatesendano 0Noch keine Bewertungen

- Grant of IR17JulDokument2 SeitenGrant of IR17JulAshwani BhallaNoch keine Bewertungen

- Hansen Aise Im Ch02Dokument39 SeitenHansen Aise Im Ch02FirlanaSubekti100% (1)

- Working Capital NumericalsDokument3 SeitenWorking Capital NumericalsShriya SajeevNoch keine Bewertungen

- Assignment - Engro CorpDokument18 SeitenAssignment - Engro CorpUmar ButtNoch keine Bewertungen

- New Almarai Presentation Jan 09Dokument55 SeitenNew Almarai Presentation Jan 09Renato AbalosNoch keine Bewertungen

- Econometrics Assignment Summary and TableDokument4 SeitenEconometrics Assignment Summary and TableG Murtaza DarsNoch keine Bewertungen

- Province of AklanDokument3 SeitenProvince of AklanDada N. NahilNoch keine Bewertungen