Das könnte Ihnen auch gefallen

- Flipping The Burger InfographicDokument1 SeiteFlipping The Burger InfographiclehighsolutionsNoch keine Bewertungen

- Sterne Agee On Brinker - EATDokument5 SeitenSterne Agee On Brinker - EATlehighsolutionsNoch keine Bewertungen

- Piper Jaffray On BAGL 8.14Dokument4 SeitenPiper Jaffray On BAGL 8.14lehighsolutionsNoch keine Bewertungen

- Sterne Agee On Red RobinDokument9 SeitenSterne Agee On Red RobinlehighsolutionsNoch keine Bewertungen

- Sterne Agee On DardenDokument4 SeitenSterne Agee On DardenlehighsolutionsNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Process of Environmental Clerance and The Involve inDokument9 SeitenProcess of Environmental Clerance and The Involve inCharchil SainiNoch keine Bewertungen

- Aggregate Demand and Aggregate Supply PDFDokument18 SeitenAggregate Demand and Aggregate Supply PDFAsif WarsiNoch keine Bewertungen

- BFSI Chronicle 3rd Annual Issue (14th Edition) September 2023Dokument132 SeitenBFSI Chronicle 3rd Annual Issue (14th Edition) September 2023amanchauhanNoch keine Bewertungen

- Special Economic ZoneDokument7 SeitenSpecial Economic ZoneAnonymous cRMw8feac8Noch keine Bewertungen

- Annexure V Bidder Response SheetDokument2 SeitenAnnexure V Bidder Response SheetAshishNoch keine Bewertungen

- SWOT AnalysisDokument12 SeitenSWOT AnalysisSam LaiNoch keine Bewertungen

- Garage Locator PDFDokument134 SeitenGarage Locator PDFMCS SBINoch keine Bewertungen

- Section 1: Introduction About FirmDokument1 SeiteSection 1: Introduction About FirmAhmadDaimNoch keine Bewertungen

- 2019 Apr 20 Dms Aiu MasterDokument25 Seiten2019 Apr 20 Dms Aiu MasterIrsyad ArifiantoNoch keine Bewertungen

- Economy of Pakistan Course OutlineDokument2 SeitenEconomy of Pakistan Course OutlineFarhan Sarwar100% (1)

- Volvo Trucks CaseDokument33 SeitenVolvo Trucks Caseravichauhan18100% (3)

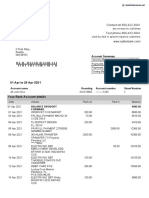

- Sutton Bank StatementDokument2 SeitenSutton Bank StatementNadiia AvetisianNoch keine Bewertungen

- Jai Guru Dev Maharishi Vidya Mandir, Hyderabad E-Learning Subject: Mathematics Class6Dokument4 SeitenJai Guru Dev Maharishi Vidya Mandir, Hyderabad E-Learning Subject: Mathematics Class6shuvanNoch keine Bewertungen

- Chapter 7Dokument6 SeitenChapter 7jobhihtihjrNoch keine Bewertungen

- Lean Remediation - Azimuth1Dokument1 SeiteLean Remediation - Azimuth1Jason DaltonNoch keine Bewertungen

- Ioriatti Resume PDFDokument1 SeiteIoriatti Resume PDFnioriatti8924Noch keine Bewertungen

- Steger Cooper ReadingGuideDokument2 SeitenSteger Cooper ReadingGuideRicardo DíazNoch keine Bewertungen

- AgricultureDokument40 SeitenAgricultureLouise Maccloud100% (2)

- SaleDokument1 SeiteSaleMegan HerreraNoch keine Bewertungen

- Ikhlayel 2018Dokument41 SeitenIkhlayel 2018Biswajit Debnath OffcNoch keine Bewertungen

- Project 4 Sem 3 Danda Yoga KrishnaDokument70 SeitenProject 4 Sem 3 Danda Yoga Krishnadanda yoga krishnaNoch keine Bewertungen

- Dao29 2004Dokument17 SeitenDao29 2004Quinnee VallejosNoch keine Bewertungen

- KONTRAK KERJA 2 BahasaDokument12 SeitenKONTRAK KERJA 2 BahasaStanley RusliNoch keine Bewertungen

- 2023 - Forecast George FriedmanDokument17 Seiten2023 - Forecast George FriedmanGeorge BestNoch keine Bewertungen

- Extrajudicial Settlement With SaleDokument2 SeitenExtrajudicial Settlement With SalePrince Rayner RoblesNoch keine Bewertungen

- Income CertificateDokument1 SeiteIncome CertificatedeepakbadimundaNoch keine Bewertungen

- Airbus A3XX: Developing The World's Largest Commercial JetDokument31 SeitenAirbus A3XX: Developing The World's Largest Commercial JetRishi Bajaj100% (1)

- 2017 Hu Spence Why Globalization Stalled and How To Restart ItDokument11 Seiten2017 Hu Spence Why Globalization Stalled and How To Restart Itmilan_ig81Noch keine Bewertungen

- What Are The Difference Between Governme PDFDokument2 SeitenWhat Are The Difference Between Governme PDFIndira IndiraNoch keine Bewertungen

- At 5906 Audit ReportDokument11 SeitenAt 5906 Audit ReportZyl Diez MagnoNoch keine Bewertungen