Das könnte Ihnen auch gefallen

- The Indian ExpressDokument20 SeitenThe Indian ExpressPranav100% (1)

- Working Capital Management in Mahindra & Mahindra LTD: January 2008Dokument15 SeitenWorking Capital Management in Mahindra & Mahindra LTD: January 2008Haris AnsariNoch keine Bewertungen

- HR SoftwaresDokument40 SeitenHR SoftwaresGitanjali GadsingNoch keine Bewertungen

- Internship Project-1Dokument105 SeitenInternship Project-1ELECTRONICS COMMUNICATION ENGINEERING BRANCHNoch keine Bewertungen

- Summer Internship Project Report For MbaDokument84 SeitenSummer Internship Project Report For MbaAkhil KesharwaniNoch keine Bewertungen

- SIP ReportDokument41 SeitenSIP Reportkshitij patil100% (1)

- IMC TextbookDokument917 SeitenIMC TextbookRiyaaa MagarrrNoch keine Bewertungen

- SHUBHAM BHARDWAJ Mini ProjectDokument48 SeitenSHUBHAM BHARDWAJ Mini ProjectShubham TyagiNoch keine Bewertungen

- Portfolio Selection and Management Using Power BIDokument37 SeitenPortfolio Selection and Management Using Power BIKomal SharmaNoch keine Bewertungen

- Final FileDokument69 SeitenFinal FileGulshan kumarNoch keine Bewertungen

- A Study On Retail BankingDokument66 SeitenA Study On Retail Bankingshreyshaw210% (1)

- Mba - Financial Report TKRDokument60 SeitenMba - Financial Report TKRChandrakant Rana SinghNoch keine Bewertungen

- Au Small Finance Bank Research ReportDokument7 SeitenAu Small Finance Bank Research ReportKunika JaiswalNoch keine Bewertungen

- PPTP Programme 2 VCE CSIPDokument5 SeitenPPTP Programme 2 VCE CSIPBhumika AdlakNoch keine Bewertungen

- Summer Internship Project Swan Investmart LimitedDokument46 SeitenSummer Internship Project Swan Investmart LimitedAMAN PANDEYNoch keine Bewertungen

- UntitledDokument52 SeitenUntitledRahul SanasNoch keine Bewertungen

- A Comparative Study On Specific Mutual Funds Schemes of SBI & ICICI Mutual FundDokument99 SeitenA Comparative Study On Specific Mutual Funds Schemes of SBI & ICICI Mutual FundGanesh TiwariNoch keine Bewertungen

- Operations ProjectDokument69 SeitenOperations ProjectharshNoch keine Bewertungen

- Jasdeep SynopsisDokument8 SeitenJasdeep SynopsisNageshwar SinghNoch keine Bewertungen

- IPO Management Practice in NEPSEDokument82 SeitenIPO Management Practice in NEPSEमोबाईल सुचना केन्द्र100% (4)

- A Comparative Study On Mutual FundsDokument2 SeitenA Comparative Study On Mutual FundsEditor IJTSRDNoch keine Bewertungen

- Chaitanya India Fin Credit Private LimitedDokument22 SeitenChaitanya India Fin Credit Private LimitedAditi SharmaNoch keine Bewertungen

- Management Concepts and Organisational Behaviour: Module - 1Dokument45 SeitenManagement Concepts and Organisational Behaviour: Module - 1sakshiNoch keine Bewertungen

- Parvind GautamDokument101 SeitenParvind GautamRitesh pandey100% (1)

- Student, Institution and Industry Track (SIIT)Dokument31 SeitenStudent, Institution and Industry Track (SIIT)coolclash boy444Noch keine Bewertungen

- 1NH18MBA49Dokument95 Seiten1NH18MBA49AkashNoch keine Bewertungen

- Anurag - Choudhary - SIP - Report - Prof - Inderpal SinghDokument55 SeitenAnurag - Choudhary - SIP - Report - Prof - Inderpal SinghanuragNoch keine Bewertungen

- ISM-AYUSH BANSAL Practical file-BBA 212Dokument20 SeitenISM-AYUSH BANSAL Practical file-BBA 212Nimish BansalNoch keine Bewertungen

- Ardra - MBA FINAL PROJECTDokument90 SeitenArdra - MBA FINAL PROJECTKochuthresia JosephNoch keine Bewertungen

- A Study On Financial Statement Analysis of Lakshmigraha Worldwide IncDokument77 SeitenA Study On Financial Statement Analysis of Lakshmigraha Worldwide IncSurendra SkNoch keine Bewertungen

- STRV Report - Varsha BhojwaniDokument57 SeitenSTRV Report - Varsha BhojwaniVARSHA BHOJWANINoch keine Bewertungen

- Capital BudgetingDokument28 SeitenCapital BudgetingDivya AgarwalNoch keine Bewertungen

- Application of Advantage of Analytics in Mining Industry 2Dokument9 SeitenApplication of Advantage of Analytics in Mining Industry 2AKRUTI JENA 19111304Noch keine Bewertungen

- Finance and Project Management AssignmentDokument22 SeitenFinance and Project Management AssignmentMashaal FNoch keine Bewertungen

- Internship Report: N. M. Baki Billah Lecturer, BRAC Business School Brac UniversityDokument35 SeitenInternship Report: N. M. Baki Billah Lecturer, BRAC Business School Brac Universityanisul islamNoch keine Bewertungen

- Final Project 18bba86Dokument114 SeitenFinal Project 18bba86Hitesh SharmaNoch keine Bewertungen

- Behavioural Finance NotesDokument15 SeitenBehavioural Finance NotesHimanshi YadavNoch keine Bewertungen

- Jagan Verma FinalDokument70 SeitenJagan Verma FinalVarun ChauhanNoch keine Bewertungen

- Vinay Gadge A076 Updated ReportDokument49 SeitenVinay Gadge A076 Updated Reportlokesh dhagratwarNoch keine Bewertungen

- Summer Traning Program Mohit SinghDokument98 SeitenSummer Traning Program Mohit SinghMohit SinghNoch keine Bewertungen

- Panasonic VS LG Marketing Strategy Mba CheckingDokument49 SeitenPanasonic VS LG Marketing Strategy Mba Checkingsatyam computersNoch keine Bewertungen

- "Marketing For Educational Books at Arihant Publication": A Summer Training Project Report ONDokument92 Seiten"Marketing For Educational Books at Arihant Publication": A Summer Training Project Report ONPrints BindingsNoch keine Bewertungen

- TAPMI Summer Internship 2023Dokument13 SeitenTAPMI Summer Internship 2023Neeraj TakkalakiNoch keine Bewertungen

- Rohit SIP Final Proj. To PrintDokument74 SeitenRohit SIP Final Proj. To PrintGaurav WattamwarNoch keine Bewertungen

- An Agro-Based Industrial ProjectDokument110 SeitenAn Agro-Based Industrial ProjectMunirul IslamNoch keine Bewertungen

- Nilesh SIPDokument69 SeitenNilesh SIPNilesh JadhavNoch keine Bewertungen

- A Study On The Working of Hanu Reddy Realty PVT LimitedDokument53 SeitenA Study On The Working of Hanu Reddy Realty PVT LimitedCharitha CherryNoch keine Bewertungen

- Kotak To HDFC 1Dokument92 SeitenKotak To HDFC 1PRAKASHNoch keine Bewertungen

- SWOT Analysis Bharti AirtelDokument8 SeitenSWOT Analysis Bharti Airtelsemin_sam100% (1)

- Project ReportDokument94 SeitenProject ReportViral MakNoch keine Bewertungen

- MBA-I 414 Statistics For ManagementDokument2 SeitenMBA-I 414 Statistics For ManagementArchana RNoch keine Bewertungen

- Bhel ProjectDokument112 SeitenBhel Projectdeepak PannuNoch keine Bewertungen

- Myntra-Mini ProjectDokument40 SeitenMyntra-Mini ProjectAyush Sarda100% (1)

- EconomicsDokument44 SeitenEconomicsVishrut ChhajerNoch keine Bewertungen

- 9754 Pradnyesh Vitkar OSCMDokument57 Seiten9754 Pradnyesh Vitkar OSCMGaneshNoch keine Bewertungen

- Project Work On Post Marketing Surveillance of Pemazyre: For Partial Fulfilment of The Requirement For TheDokument45 SeitenProject Work On Post Marketing Surveillance of Pemazyre: For Partial Fulfilment of The Requirement For ThesalmanNoch keine Bewertungen

- "Potential of Life Insurance Industry in Surat Market": Under The Guidance ofDokument51 Seiten"Potential of Life Insurance Industry in Surat Market": Under The Guidance ofFreddy Savio D'souzaNoch keine Bewertungen

- Merchant Banking and Financial Services: University of MadrasDokument62 SeitenMerchant Banking and Financial Services: University of MadrasHema vijay sNoch keine Bewertungen

- Project Details Soumyadeep SarkarDokument19 SeitenProject Details Soumyadeep Sarkarvineet agarwalNoch keine Bewertungen

- Final MBA-suragDokument84 SeitenFinal MBA-suragSurag VsNoch keine Bewertungen

- Funds Flow StatementDokument101 SeitenFunds Flow StatementSakhamuri Ram'sNoch keine Bewertungen

- List of The Tables: SL NO NO Title of The Table Page NoDokument9 SeitenList of The Tables: SL NO NO Title of The Table Page NoSakhamuri Ram'sNoch keine Bewertungen

- Funds Flow Statement Tirumala MilkDokument101 SeitenFunds Flow Statement Tirumala MilkSakhamuri Ram's100% (3)

- Ancient Greek: Agriculture Agriculture, Also Called Farming or Husbandry, Is The Cultivation ofDokument4 SeitenAncient Greek: Agriculture Agriculture, Also Called Farming or Husbandry, Is The Cultivation ofSakhamuri Ram'sNoch keine Bewertungen

- "Funds Flow Statement": Eswar College of EngineeringDokument8 Seiten"Funds Flow Statement": Eswar College of EngineeringSakhamuri Ram'sNoch keine Bewertungen

- Eswar College of Engineering: "Financial Statement Analysis"Dokument6 SeitenEswar College of Engineering: "Financial Statement Analysis"Sakhamuri Ram'sNoch keine Bewertungen

- Performance AppraisalDokument85 SeitenPerformance AppraisalSakhamuri Ram'sNoch keine Bewertungen

- Emp Name Shaik Khadeer Emp Code 11366 Joining Date 16-03-2013 Working Branch Bapatla Gannavaram Warangal Month JAN FEB MAR TotalDokument2 SeitenEmp Name Shaik Khadeer Emp Code 11366 Joining Date 16-03-2013 Working Branch Bapatla Gannavaram Warangal Month JAN FEB MAR TotalSakhamuri Ram'sNoch keine Bewertungen

- Financial Reports of Devi Sea LTD: Profit & Loss Account For The Year Ended 31St March, 2009Dokument11 SeitenFinancial Reports of Devi Sea LTD: Profit & Loss Account For The Year Ended 31St March, 2009Sakhamuri Ram'sNoch keine Bewertungen

- Master of Business Administration: A Study On Ratio Analysis With Reference To Jocil LimitedDokument97 SeitenMaster of Business Administration: A Study On Ratio Analysis With Reference To Jocil LimitedSakhamuri Ram'sNoch keine Bewertungen

- Industry Indan Cotton Textile ProfileDokument30 SeitenIndustry Indan Cotton Textile ProfileSakhamuri Ram'sNoch keine Bewertungen

- Amaravathi 16 PointsdDokument16 SeitenAmaravathi 16 PointsdSakhamuri Ram'sNoch keine Bewertungen

- CottonDokument17 SeitenCottonSakhamuri Ram's100% (1)

- Industry Indan Cotton Textile ProfileDokument30 SeitenIndustry Indan Cotton Textile ProfileSakhamuri Ram'sNoch keine Bewertungen

- Cotton IndustryDokument18 SeitenCotton IndustrySakhamuri Ram'sNoch keine Bewertungen

- Training & Development TirumalaDokument103 SeitenTraining & Development TirumalaSakhamuri Ram's0% (1)

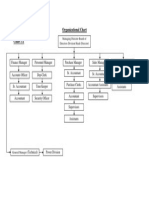

- Organizational Chart Chart 3.1: Managing Director-Board of Directors Division Head (Director)Dokument1 SeiteOrganizational Chart Chart 3.1: Managing Director-Board of Directors Division Head (Director)Sakhamuri Ram'sNoch keine Bewertungen

- Financial Statement Sivaswathi TEXTILESDokument103 SeitenFinancial Statement Sivaswathi TEXTILESSakhamuri Ram'sNoch keine Bewertungen

- Customer Satisfaction Nagarjuna FertilizersDokument97 SeitenCustomer Satisfaction Nagarjuna FertilizersSakhamuri Ram's100% (2)

- KCP Final Project - 2.1Dokument110 SeitenKCP Final Project - 2.1Sakhamuri Ram'sNoch keine Bewertungen

- Customer Satisfaction AmaravathiDokument84 SeitenCustomer Satisfaction AmaravathiSakhamuri Ram'sNoch keine Bewertungen

- Inventory Management PROJECTDokument47 SeitenInventory Management PROJECTSakhamuri Ram'sNoch keine Bewertungen

- Inventory Management SWATHIDokument96 SeitenInventory Management SWATHISakhamuri Ram'sNoch keine Bewertungen

- A Study On Consumer PerceptionDokument4 SeitenA Study On Consumer PerceptionSakhamuri Ram'sNoch keine Bewertungen

- Customer Satisfaction AmaravathiDokument84 SeitenCustomer Satisfaction AmaravathiSakhamuri Ram'sNoch keine Bewertungen

- Role of Energy Conservation in Spinning MillsDokument15 SeitenRole of Energy Conservation in Spinning MillsMufaddal BagwalaNoch keine Bewertungen

- Rahim Cotton Mills-InternshipDokument59 SeitenRahim Cotton Mills-InternshipJamal Uddin MahinNoch keine Bewertungen

- Compact Yarn: S.M. Farhana Iqbal Associate Prof. ButexDokument22 SeitenCompact Yarn: S.M. Farhana Iqbal Associate Prof. ButexSadia TabassumNoch keine Bewertungen

- Coc Project FinalDokument46 SeitenCoc Project FinalMYTHRIYA DEVANANDHANNoch keine Bewertungen

- BSL PrintDokument62 SeitenBSL Printrishi100% (1)

- Sutlej Textiles and Industries Summer Training Report-SPINNINGDokument119 SeitenSutlej Textiles and Industries Summer Training Report-SPINNINGSmriti Singh100% (2)

- TSC Q0202 PDFDokument52 SeitenTSC Q0202 PDFpraveen nairNoch keine Bewertungen

- Spinning Rings and TravellersDokument6 SeitenSpinning Rings and TravellersDinesh J KeswaniNoch keine Bewertungen

- MC Ring Frame Tenter RevisedDokument20 SeitenMC Ring Frame Tenter RevisedSumeet GillNoch keine Bewertungen

- R&F TravellerDokument51 SeitenR&F TravellerRanjan ChaudharyNoch keine Bewertungen

- Modern Spinning Machineries Maintenance PracticalDokument116 SeitenModern Spinning Machineries Maintenance Practicalmasum_austNoch keine Bewertungen

- Raymond TextileDokument8 SeitenRaymond Textilepgdm1315100% (1)

- Safety in Textile Industry: Chapter - 21Dokument49 SeitenSafety in Textile Industry: Chapter - 21Abhishek100% (1)

- Final Supervised Industrial Internship Report 1Dokument33 SeitenFinal Supervised Industrial Internship Report 1Mudassar AliNoch keine Bewertungen

- Lab Report 10Dokument8 SeitenLab Report 10ziauddinNoch keine Bewertungen

- Zinnat 171-23-4956Dokument44 SeitenZinnat 171-23-4956Md. Zinnat Hossain 171-23-4956Noch keine Bewertungen

- Process Parameters in SimplexDokument3 SeitenProcess Parameters in SimplexTanvir Alam100% (5)

- INTERNSHIP REPORT-Arvind Ltd-Arushi Srivastava-Vaishali Rai NIFT Delhi PDFDokument110 SeitenINTERNSHIP REPORT-Arvind Ltd-Arushi Srivastava-Vaishali Rai NIFT Delhi PDFRonak Joshi0% (1)

- Doffer in Carding Machine - Types, Specification, Functions & MaintenanceDokument5 SeitenDoffer in Carding Machine - Types, Specification, Functions & MaintenanceRaj BistNoch keine Bewertungen

- Project Report On Employee Absenteeism: An Empirical Study of Workers at Aarti InternationalDokument93 SeitenProject Report On Employee Absenteeism: An Empirical Study of Workers at Aarti InternationalkulveerNoch keine Bewertungen

- Rings & Ring Travellers DetDokument12 SeitenRings & Ring Travellers DetArchana ParidaNoch keine Bewertungen

- SpinningDokument19 SeitenSpinningGayathiri KannanNoch keine Bewertungen

- Yarn Manufacturing ProcessDokument92 SeitenYarn Manufacturing ProcessUjjwal Anand50% (2)

- Processing From Gin To Fabric PDFDokument12 SeitenProcessing From Gin To Fabric PDFKannan KrishnamurthyNoch keine Bewertungen

- SpinningDokument8 SeitenSpinningAishee BhowmickNoch keine Bewertungen

- Btech Syllabus Textile EngineeringDokument68 SeitenBtech Syllabus Textile EngineeringShubham BansalNoch keine Bewertungen

- Ring Spinning Machine LR 6/S Specification and Question AnswerDokument15 SeitenRing Spinning Machine LR 6/S Specification and Question AnswerPramod SonbarseNoch keine Bewertungen

- Ratio Analysis 1012Dokument74 SeitenRatio Analysis 1012Sakhamuri Ram'sNoch keine Bewertungen

- A Review of Current Yarn Production Me-L. Introducction Thods - Their Scope, Advantage and Future PotentialDokument7 SeitenA Review of Current Yarn Production Me-L. Introducction Thods - Their Scope, Advantage and Future PotentialAditya ShrivastavaNoch keine Bewertungen

- Control Startup BreakageDokument4 SeitenControl Startup BreakageAnish ak100% (5)