Das könnte Ihnen auch gefallen

- Taxation Law I Case Digests 2Dokument45 SeitenTaxation Law I Case Digests 2Christopher G. Halnin75% (4)

- J.K. Lasser's Real Estate Investors Tax Edge: Top Secret Strategies of Millionaires ExposedVon EverandJ.K. Lasser's Real Estate Investors Tax Edge: Top Secret Strategies of Millionaires ExposedNoch keine Bewertungen

- Motions - in - Limine SampleDokument4 SeitenMotions - in - Limine Samplealexakos01100% (2)

- Cease and Desist Letter To Waco Police ChiefDokument1 SeiteCease and Desist Letter To Waco Police ChieflanashadwickNoch keine Bewertungen

- Labor Law Case DigestDokument95 SeitenLabor Law Case DigestInter_vivos100% (1)

- Hispanic Americans in Congress 1822-2012Dokument775 SeitenHispanic Americans in Congress 1822-2012LJ's infoDOCKET100% (1)

- Wrongful Foreclosure Appeal 11th Cir.Dokument33 SeitenWrongful Foreclosure Appeal 11th Cir.Janet and James100% (2)

- Case Digests TaxDokument10 SeitenCase Digests TaxAron PanturillaNoch keine Bewertungen

- Case Digest - StaconDokument56 SeitenCase Digest - StaconRICKY ALEGARBES100% (5)

- Conwi v. CTA FactsDokument37 SeitenConwi v. CTA Factsivan markNoch keine Bewertungen

- Conwi v. Court of Tax Appeals, G.R. No. 48532, August 31, 1992Dokument6 SeitenConwi v. Court of Tax Appeals, G.R. No. 48532, August 31, 1992zac100% (1)

- Tax 2 Digest (0406) GR 108576 012099 Cir Vs CaDokument3 SeitenTax 2 Digest (0406) GR 108576 012099 Cir Vs CaAudrey Deguzman100% (1)

- Afdal Vs Carlos 1Dokument1 SeiteAfdal Vs Carlos 1Keangela LouiseNoch keine Bewertungen

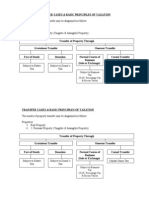

- Transfer TaxesDokument3 SeitenTransfer TaxesbeverlyrtanNoch keine Bewertungen

- Case Digest Finals 1Dokument5 SeitenCase Digest Finals 1kemsue1224Noch keine Bewertungen

- CRIM 2 People Vs KottingerDokument2 SeitenCRIM 2 People Vs Kottingerfollowthefishies50% (2)

- Rural Bank of Caloocan vs. CADokument3 SeitenRural Bank of Caloocan vs. CAElaine Atienza-Illescas100% (5)

- Conwi v. CTA, 213 SCRA 83Dokument2 SeitenConwi v. CTA, 213 SCRA 83Homer Simpson100% (2)

- Caso Diefenthal InglesDokument14 SeitenCaso Diefenthal InglesAnonymous KkZVCdSeJJNoch keine Bewertungen

- Republic of The Philippines Court of Tax Appeals Quezon CityDokument18 SeitenRepublic of The Philippines Court of Tax Appeals Quezon CityCJNoch keine Bewertungen

- United States v. William Giglio, Frank Livorsi, and Howard Lawn, Louis J. Roth and American Brands Corporation, 232 F.2d 589, 2d Cir. (1956)Dokument9 SeitenUnited States v. William Giglio, Frank Livorsi, and Howard Lawn, Louis J. Roth and American Brands Corporation, 232 F.2d 589, 2d Cir. (1956)Scribd Government DocsNoch keine Bewertungen

- Taxation CasesDokument30 SeitenTaxation CasesNelsonPolinarLaurdenNoch keine Bewertungen

- United States Court of Appeals, Eleventh CircuitDokument9 SeitenUnited States Court of Appeals, Eleventh CircuitScribd Government DocsNoch keine Bewertungen

- REJ Da Oi - SADokument38 SeitenREJ Da Oi - SAPablo HierroNoch keine Bewertungen

- Piedmont Minerals Company, Inc. v. United States, 429 F.2d 560, 4th Cir. (1970)Dokument6 SeitenPiedmont Minerals Company, Inc. v. United States, 429 F.2d 560, 4th Cir. (1970)Scribd Government DocsNoch keine Bewertungen

- YPF - Petersen ComplaintDokument30 SeitenYPF - Petersen ComplaintFilesDotComNoch keine Bewertungen

- 2-Fisher vs. TrinidadDokument8 Seiten2-Fisher vs. TrinidadRadel LlagasNoch keine Bewertungen

- 13-Fisher v. Trinidad G.R. No. L-17518 October 30, 1922Dokument13 Seiten13-Fisher v. Trinidad G.R. No. L-17518 October 30, 1922Jopan SJNoch keine Bewertungen

- Wrigley AR 2006Dokument21 SeitenWrigley AR 2006SteveMastersNoch keine Bewertungen

- Wm. Wrigley Jr. Company: Form 10-KDokument24 SeitenWm. Wrigley Jr. Company: Form 10-KSteveMastersNoch keine Bewertungen

- 0808 Tax CasesDokument13 Seiten0808 Tax CasesAnonymous K286lBXothNoch keine Bewertungen

- Lack IndictmentDokument24 SeitenLack Indictmentinfo476Noch keine Bewertungen

- ToysRUs March 2018Dokument124 SeitenToysRUs March 2018Ben SchultzNoch keine Bewertungen

- G.R. No. L-17518 October 30, 1922 FREDERICK C. FISHER, Plaintiff-Appellant, WENCESLAO TRINIDAD, Collector of Internal Revenue, Defendant-AppelleeDokument11 SeitenG.R. No. L-17518 October 30, 1922 FREDERICK C. FISHER, Plaintiff-Appellant, WENCESLAO TRINIDAD, Collector of Internal Revenue, Defendant-AppelleeMayNoch keine Bewertungen

- Guiguis IndictmentDokument21 SeitenGuiguis IndictmenthaleNoch keine Bewertungen

- Income Tax Law CasesDokument66 SeitenIncome Tax Law Casesjemaycabano18Noch keine Bewertungen

- Transfer Tax Case DigestDokument30 SeitenTransfer Tax Case DigestErneylou RanayNoch keine Bewertungen

- Commissioner of Internal Revenue Vs Bair NickelDokument9 SeitenCommissioner of Internal Revenue Vs Bair NickelARCHIE AJIASNoch keine Bewertungen

- The Study of The Japanese Economy: Macroeconomics For Business ExecutivesDokument14 SeitenThe Study of The Japanese Economy: Macroeconomics For Business ExecutivesUtkarsh JainNoch keine Bewertungen

- Fisher v. Trinidad, G.R. No. L-17518, 1922Dokument13 SeitenFisher v. Trinidad, G.R. No. L-17518, 1922BREL GOSIMATNoch keine Bewertungen

- Fisher v. Trinidad, G.R. No. L-17518, October 30, 1922Dokument13 SeitenFisher v. Trinidad, G.R. No. L-17518, October 30, 1922zacNoch keine Bewertungen

- Cases in TaxDokument26 SeitenCases in TaxJames Mier VictorianoNoch keine Bewertungen

- 2 Conwi vs. Court of Tax AppealsDokument9 Seiten2 Conwi vs. Court of Tax AppealsAriel Conrad MalimasNoch keine Bewertungen

- CIR Vs Baier-Nickel, GR 153793, Aug. 29, 2006Dokument8 SeitenCIR Vs Baier-Nickel, GR 153793, Aug. 29, 2006Dario G. TorresNoch keine Bewertungen

- G.R. No. 153793 August 29, 2006 Commissioner of Internal Revenue, Petitioner, JULIANE BAIER-NICKEL, As Represented by Marina Q. Guzman (Attorney-In-Fact) RespondentDokument43 SeitenG.R. No. 153793 August 29, 2006 Commissioner of Internal Revenue, Petitioner, JULIANE BAIER-NICKEL, As Represented by Marina Q. Guzman (Attorney-In-Fact) RespondentSon Gabriel UyNoch keine Bewertungen

- Capital Video v. Commissioner, 311 F.3d 458, 1st Cir. (2002)Dokument11 SeitenCapital Video v. Commissioner, 311 F.3d 458, 1st Cir. (2002)Scribd Government DocsNoch keine Bewertungen

- BIRD BOX DLONSOD TAX DIGESTS Concept of IncomeDokument5 SeitenBIRD BOX DLONSOD TAX DIGESTS Concept of IncomeRalph MondayNoch keine Bewertungen

- Matson Nav. Co. v. State Bd. of Equalization of Cal., 297 U.S. 441 (1936)Dokument4 SeitenMatson Nav. Co. v. State Bd. of Equalization of Cal., 297 U.S. 441 (1936)Scribd Government DocsNoch keine Bewertungen

- Fisher vs. TrinidadDokument10 SeitenFisher vs. TrinidadlexsoloNoch keine Bewertungen

- GR No. 153793Dokument9 SeitenGR No. 153793Milette Abadilla AngelesNoch keine Bewertungen

- 91f52d6b-a48b-4b90-ad4d-02dd572827fdDokument22 Seiten91f52d6b-a48b-4b90-ad4d-02dd572827fdHeather Timmons100% (1)

- 8 - SC - Batas.org - 1992 - G.R. No. 100401, August 24, 1992Dokument11 Seiten8 - SC - Batas.org - 1992 - G.R. No. 100401, August 24, 1992MarieNoch keine Bewertungen

- Toys R Us Debtors Motion For Entry of OrdersDokument124 SeitenToys R Us Debtors Motion For Entry of OrdersStephen LoiaconiNoch keine Bewertungen

- United States Court of Appeals, Fourth CircuitDokument10 SeitenUnited States Court of Appeals, Fourth CircuitScribd Government DocsNoch keine Bewertungen

- (G.R. No. 171054, January 26, 2021) Edgardo T. Yambao, Petitioner, vs. Republic of The Philippines, Represented by The Anti-Money Laundering Council, Respondent. Decision Gaerlan, J.Dokument12 Seiten(G.R. No. 171054, January 26, 2021) Edgardo T. Yambao, Petitioner, vs. Republic of The Philippines, Represented by The Anti-Money Laundering Council, Respondent. Decision Gaerlan, J.Ruby Anna TorresNoch keine Bewertungen

- Complaint For LIBEL PDFDokument16 SeitenComplaint For LIBEL PDFHannah Tolentino-DomantayNoch keine Bewertungen

- Bergersen v. Commissioner, 109 F.3d 56, 1st Cir. (1997)Dokument10 SeitenBergersen v. Commissioner, 109 F.3d 56, 1st Cir. (1997)Scribd Government DocsNoch keine Bewertungen

- Robert Maxwell Watts v. United States, 220 F.2d 483, 10th Cir. (1955)Dokument6 SeitenRobert Maxwell Watts v. United States, 220 F.2d 483, 10th Cir. (1955)Scribd Government DocsNoch keine Bewertungen

- Conwi Vs CtaDokument7 SeitenConwi Vs CtaJeff GomezNoch keine Bewertungen

- Fisher v. Trinidad G.R. No. L-17518 October 30, 1922Dokument10 SeitenFisher v. Trinidad G.R. No. L-17518 October 30, 1922aNoch keine Bewertungen

- Cir v. Nickel Case DigestDokument92 SeitenCir v. Nickel Case DigestCheryl OlivarezNoch keine Bewertungen

- Tax QuestionsDokument5 SeitenTax QuestionsDrizza FerrerNoch keine Bewertungen

- 59-Esso Standard Eastern, Inc. v. CIR G.R. Nos. L-28508-9 July 7, 1989Dokument5 Seiten59-Esso Standard Eastern, Inc. v. CIR G.R. Nos. L-28508-9 July 7, 1989Jopan SJNoch keine Bewertungen

- CONWI Vs CTADokument11 SeitenCONWI Vs CTAmichelledugsNoch keine Bewertungen

- Fisher Vs TrinidadDokument6 SeitenFisher Vs TrinidadAllen Mark Buljatin TacordaNoch keine Bewertungen

- Reagan v. Commissioner of Internal Revenue 30 SCRA 968Dokument3 SeitenReagan v. Commissioner of Internal Revenue 30 SCRA 968Kim Boyles FuentesNoch keine Bewertungen

- Report of Al Capone for the Bureau of Internal RevenueVon EverandReport of Al Capone for the Bureau of Internal RevenueNoch keine Bewertungen

- Purpura-Moran Initial Decision of ALJ MasinDokument9 SeitenPurpura-Moran Initial Decision of ALJ Masinpuzo1Noch keine Bewertungen

- Oracle v. Department of Labor ComplaintDokument48 SeitenOracle v. Department of Labor ComplaintWashington Free BeaconNoch keine Bewertungen

- Videocon Industries Ltd. Vs Union of India & Anr. On 11 May, 2011 (Supreme Court)Dokument13 SeitenVideocon Industries Ltd. Vs Union of India & Anr. On 11 May, 2011 (Supreme Court)vidhi8954Noch keine Bewertungen

- Indian Evidence ActDokument73 SeitenIndian Evidence Actsumitkumar_sumanNoch keine Bewertungen

- Velma Pridemore v. Usair, Incorporated, 98 F.3d 1335, 4th Cir. (1996)Dokument6 SeitenVelma Pridemore v. Usair, Incorporated, 98 F.3d 1335, 4th Cir. (1996)Scribd Government DocsNoch keine Bewertungen

- Labor 1 Polyfoam-RGC International Inc. vs. Concepcion: Supreme CourtDokument13 SeitenLabor 1 Polyfoam-RGC International Inc. vs. Concepcion: Supreme CourtthefiledetectorNoch keine Bewertungen

- Verizon v. OnlineNIC, Inc.Dokument13 SeitenVerizon v. OnlineNIC, Inc.Ben SheffnerNoch keine Bewertungen

- PATULA Vs PP DigestDokument1 SeitePATULA Vs PP DigestJumen Gamaru Tamayo0% (1)

- Supreme Court PaperDokument24 SeitenSupreme Court PaperShailesh Gandhi100% (1)

- Ku Chandan and Ors Vs Longa Bai and Anr 14071997 6980001COM576207Dokument17 SeitenKu Chandan and Ors Vs Longa Bai and Anr 14071997 6980001COM576207Raj ChouhanNoch keine Bewertungen

- Vithalbhai Vs Central On 30 January, 2008Dokument17 SeitenVithalbhai Vs Central On 30 January, 2008Sarita RaniNoch keine Bewertungen

- Consigna vs. PeopleDokument11 SeitenConsigna vs. PeopleElreen Pearl AgustinNoch keine Bewertungen

- Direct ExaminationDokument3 SeitenDirect ExaminationJane Erika VitugNoch keine Bewertungen

- State Bar of Georgia Requests Walter Moore's Disbarment - Filed Dec. 4, 2017.Dokument9 SeitenState Bar of Georgia Requests Walter Moore's Disbarment - Filed Dec. 4, 2017.Julie WolfeNoch keine Bewertungen

- People Vs DoriaDokument14 SeitenPeople Vs DoriaRon AceroNoch keine Bewertungen

- Sayo V Chief of PoliceDokument5 SeitenSayo V Chief of PoliceBrian Jonathan ParaanNoch keine Bewertungen

- Instructions For Florida Supreme Court Approved Family LAW FORMS 12.922 (A), MOTION FOR DEFAULT, AND 12.922 (B), DEFAULT (11/15)Dokument7 SeitenInstructions For Florida Supreme Court Approved Family LAW FORMS 12.922 (A), MOTION FOR DEFAULT, AND 12.922 (B), DEFAULT (11/15)Autochthon GazetteNoch keine Bewertungen

- Alabang Country Club Vs NLRCDokument8 SeitenAlabang Country Club Vs NLRCPaul PanuncioNoch keine Bewertungen

- United States v. Samuel Berger, Yvette Feinstein and Travis Levy, 433 F.2d 680, 2d Cir. (1970)Dokument9 SeitenUnited States v. Samuel Berger, Yvette Feinstein and Travis Levy, 433 F.2d 680, 2d Cir. (1970)Scribd Government DocsNoch keine Bewertungen

- FJC Patent Case Management Judicial Guide PDFDokument1.230 SeitenFJC Patent Case Management Judicial Guide PDFRyan ClarkNoch keine Bewertungen

- 10 Royal Plant Workers Union V Coca ColaDokument10 Seiten10 Royal Plant Workers Union V Coca ColaEugenioNoch keine Bewertungen