Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Comparing Freight Rates for Chemical ShipmentsDokument2 SeitenComparing Freight Rates for Chemical ShipmentsNothing was0% (1)

- When India Population Becomes An Asset and Not A LiabilityDokument2 SeitenWhen India Population Becomes An Asset and Not A LiabilityGirish RamachandraNoch keine Bewertungen

- Balance Sheet (2009-2003) of TCS (US Format)Dokument15 SeitenBalance Sheet (2009-2003) of TCS (US Format)Girish RamachandraNoch keine Bewertungen

- Zylog SystemsDokument2 SeitenZylog SystemsGirish RamachandraNoch keine Bewertungen

- Date or Subtitle: Spiderlogic OverviewDokument31 SeitenDate or Subtitle: Spiderlogic OverviewGirish RamachandraNoch keine Bewertungen

- Balance Sheet (2009-2000) in US Format For Tata Motors: All Numbers Are in INR and in x10MDokument16 SeitenBalance Sheet (2009-2000) in US Format For Tata Motors: All Numbers Are in INR and in x10MGirish RamachandraNoch keine Bewertungen

- BhartiAndMTN FinancialsDokument10 SeitenBhartiAndMTN FinancialsGirish RamachandraNoch keine Bewertungen

- Telecom Sector IndiaDokument11 SeitenTelecom Sector IndiaGirish RamachandraNoch keine Bewertungen

- FII Investement Trend - 2004-09 (India)Dokument4 SeitenFII Investement Trend - 2004-09 (India)Girish RamachandraNoch keine Bewertungen

- BhartiAndMTN FinancialsDokument10 SeitenBhartiAndMTN FinancialsGirish RamachandraNoch keine Bewertungen

- Balance Sheet (2009-2001) of Maruti Suzuki: All Numbers Are in INR and in x10MDokument16 SeitenBalance Sheet (2009-2001) of Maruti Suzuki: All Numbers Are in INR and in x10MGirish RamachandraNoch keine Bewertungen

- Balance Sheet (2009-2000) - Wipro (US Format)Dokument16 SeitenBalance Sheet (2009-2000) - Wipro (US Format)Girish RamachandraNoch keine Bewertungen

- Economics of Alternative Energy For IndiaDokument52 SeitenEconomics of Alternative Energy For IndiaGirish RamachandraNoch keine Bewertungen

- All Numbers Are in INR and in x10MDokument6 SeitenAll Numbers Are in INR and in x10MGirish RamachandraNoch keine Bewertungen

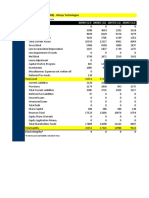

- Balance Sheet (2009-2000) - Infosys Technologies: All Numbers Are in INR and in x10MDokument18 SeitenBalance Sheet (2009-2000) - Infosys Technologies: All Numbers Are in INR and in x10MGirish RamachandraNoch keine Bewertungen

- Correlation Between Various US Indices and BSE SensexDokument3 SeitenCorrelation Between Various US Indices and BSE SensexGirish RamachandraNoch keine Bewertungen

- Sensex To Touch 1800 in December 2009Dokument4 SeitenSensex To Touch 1800 in December 2009Girish RamachandraNoch keine Bewertungen

- WhiteMonk HEG Equity Research ReportDokument15 SeitenWhiteMonk HEG Equity Research ReportGirish Ramachandra100% (1)

- QS World University Rankings 2020 - Las Mejores Universidades Mundiales - Universidades PrincipalesDokument36 SeitenQS World University Rankings 2020 - Las Mejores Universidades Mundiales - Universidades PrincipalesSamael AstarothNoch keine Bewertungen

- URC 2021 Annual Stockholders' Meeting Agenda and Voting DetailsDokument211 SeitenURC 2021 Annual Stockholders' Meeting Agenda and Voting DetailsRenier Palma CruzNoch keine Bewertungen

- MoebiusFinal PDFDokument26 SeitenMoebiusFinal PDFLéo LacerdaNoch keine Bewertungen

- JMM Promotion and Management vs Court of Appeals ruling on EIAC regulation validityDokument6 SeitenJMM Promotion and Management vs Court of Appeals ruling on EIAC regulation validityGui EshNoch keine Bewertungen

- Maha Durga Charitable Trust: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDokument6 SeitenMaha Durga Charitable Trust: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionNeeraj_Kumar_AgrawalNoch keine Bewertungen

- Exam Call Letter Clerk RecruitmentDokument2 SeitenExam Call Letter Clerk RecruitmentBala SubramanianNoch keine Bewertungen

- All You Need Is LoveDokument2 SeitenAll You Need Is LoveSir BülowNoch keine Bewertungen

- Chapter - 6. MCQDokument10 SeitenChapter - 6. MCQgamergeeeNoch keine Bewertungen

- Weathering With You OST Grand EscapeDokument3 SeitenWeathering With You OST Grand EscapeGabriel AnwarNoch keine Bewertungen

- S G Elion ComplaintDokument25 SeitenS G Elion Complainttimoth31Noch keine Bewertungen

- Pale Digests Part 1Dokument24 SeitenPale Digests Part 1dingNoch keine Bewertungen

- Newsletter No 3 - 5 May 2017Dokument3 SeitenNewsletter No 3 - 5 May 2017Kate SpainNoch keine Bewertungen

- The Real Original Sin of Modern European CivilizationDokument10 SeitenThe Real Original Sin of Modern European CivilizationOscar CabreraNoch keine Bewertungen

- Answers: Unit 5 A Place To Call HomeDokument1 SeiteAnswers: Unit 5 A Place To Call HomeMr Ling Tuition CentreNoch keine Bewertungen

- Goldziher - Muslim Studies 2Dokument190 SeitenGoldziher - Muslim Studies 2Christine Carey95% (21)

- Akin Ka NalangDokument413 SeitenAkin Ka NalangJobelle GenilNoch keine Bewertungen

- Large It ListDokument864 SeitenLarge It ListGp MishraNoch keine Bewertungen

- Batelco Services Bill - Tax InvoiceDokument3 SeitenBatelco Services Bill - Tax InvoiceAysha Muhammad ShahzadNoch keine Bewertungen

- The Neon Red Catalog: DisclaimerDokument28 SeitenThe Neon Red Catalog: DisclaimerKarl Punu100% (2)

- Assignment No. 3: Name: Sunandan Sharma Id: 181070064Dokument3 SeitenAssignment No. 3: Name: Sunandan Sharma Id: 181070064Sunandan SharmaNoch keine Bewertungen

- ShineMaster Manual 202203Dokument13 SeitenShineMaster Manual 202203João Pedro MagalhãesNoch keine Bewertungen

- Collective Bargaining:-Collective Bargaining Is A Technique byDokument13 SeitenCollective Bargaining:-Collective Bargaining Is A Technique bysaquibhafizNoch keine Bewertungen

- HBOE Detailed Agenda May 2021Dokument21 SeitenHBOE Detailed Agenda May 2021Tony PetrosinoNoch keine Bewertungen

- Achieving Academic SuccessDokument1 SeiteAchieving Academic SuccessChino Paolo ChuaNoch keine Bewertungen

- Engineering Forum 2023Dokument19 SeitenEngineering Forum 2023Kgosi MorapediNoch keine Bewertungen

- Uts MorphologyDokument4 SeitenUts MorphologySyahrani SafitriNoch keine Bewertungen

- Sri Bhakti-Sandarbha 9Dokument20 SeitenSri Bhakti-Sandarbha 9api-19975968Noch keine Bewertungen

- North Carolina Wing - Jul 2011Dokument22 SeitenNorth Carolina Wing - Jul 2011CAP History LibraryNoch keine Bewertungen

- 109 Eradication and Control Programs Guinea Worm FINALDokument53 Seiten109 Eradication and Control Programs Guinea Worm FINALFebri Yudha Adhi Kurniawan100% (1)