Das könnte Ihnen auch gefallen

- QuessCorpLimited PDFDokument13 SeitenQuessCorpLimited PDFabmahendruNoch keine Bewertungen

- Bodal Chemical PresnDokument39 SeitenBodal Chemical PresnabmahendruNoch keine Bewertungen

- Manappuram Finance Investor PresentationDokument43 SeitenManappuram Finance Investor PresentationabmahendruNoch keine Bewertungen

- Reality in 40 VersesDokument38 SeitenReality in 40 Versesmetaperl6453100% (2)

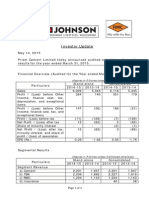

- Prism Cement Investor Update May 2015Dokument4 SeitenPrism Cement Investor Update May 2015abmahendruNoch keine Bewertungen

- Results Transcript HesterDokument18 SeitenResults Transcript HesterabmahendruNoch keine Bewertungen

- Berkshire 2016 LetterDokument28 SeitenBerkshire 2016 LetterZerohedgeNoch keine Bewertungen

- Ashiana Housing Investor PresentationDokument37 SeitenAshiana Housing Investor PresentationabmahendruNoch keine Bewertungen

- Prism Cement LTD FY 15 ResultsDokument4 SeitenPrism Cement LTD FY 15 ResultsabmahendruNoch keine Bewertungen

- Prism Cement Investor May 15Dokument30 SeitenPrism Cement Investor May 15abmahendruNoch keine Bewertungen

- Prism Cement Limited Investor UpdateDokument5 SeitenPrism Cement Limited Investor UpdateabmahendruNoch keine Bewertungen

- Investor May 2013Dokument31 SeitenInvestor May 2013nitin2khNoch keine Bewertungen

- Prism Cement Investor Update May 2014Dokument5 SeitenPrism Cement Investor Update May 2014abmahendruNoch keine Bewertungen

- Prism Cement Limited: Investor Update Feb 2014Dokument5 SeitenPrism Cement Limited: Investor Update Feb 2014abmahendruNoch keine Bewertungen

- Investor Update Oct 2012Dokument5 SeitenInvestor Update Oct 2012abmahendruNoch keine Bewertungen

- Infosys FY12Dokument3 SeitenInfosys FY12abmahendruNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5782)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Computer Spare Part ListDokument6 SeitenComputer Spare Part ListKenneth TanNoch keine Bewertungen

- Presentation TitleDokument13 SeitenPresentation TitleAzzhara FatianNoch keine Bewertungen

- CISM Outline DescriptionDokument3 SeitenCISM Outline DescriptionDannyNoch keine Bewertungen

- Exida exSILentia User Guide PDFDokument168 SeitenExida exSILentia User Guide PDFHrudayananda NayakNoch keine Bewertungen

- MRT7 - Concession AgreementDokument95 SeitenMRT7 - Concession AgreementRomeo Santos Mandinggin100% (2)

- Reducing Noise From TramsDokument21 SeitenReducing Noise From TramsFnasseNoch keine Bewertungen

- Sap MDG Presentation PDFDokument1 SeiteSap MDG Presentation PDFFaraz HussainNoch keine Bewertungen

- VPS Quotation 2019-03Dokument1 SeiteVPS Quotation 2019-03mohamed AlshriefNoch keine Bewertungen

- HR For Agile in A Nutshell 6 PDFDokument1 SeiteHR For Agile in A Nutshell 6 PDFpasc colcheteNoch keine Bewertungen

- GQNN Airport ChartsDokument2 SeitenGQNN Airport ChartsCandiceNoch keine Bewertungen

- Marcegaglia CasalmaggioreEN - Dic2012Dokument36 SeitenMarcegaglia CasalmaggioreEN - Dic2012lucidbaseNoch keine Bewertungen

- SM87 SL & XB11 SL Status LampsDokument2 SeitenSM87 SL & XB11 SL Status Lampsfroid1259539Noch keine Bewertungen

- CV Engineer Md Mahmudur RahmanDokument4 SeitenCV Engineer Md Mahmudur RahmanEngr SwapanNoch keine Bewertungen

- 2017 Optimization of Flotation Plant Performance Using Micro-Price AnalysisDokument7 Seiten2017 Optimization of Flotation Plant Performance Using Micro-Price AnalysisClaudiaCamilaRodriguezArroyoNoch keine Bewertungen

- Database Design Chapter OverviewDokument17 SeitenDatabase Design Chapter OverviewanwarNoch keine Bewertungen

- Main Data-2Dokument144 SeitenMain Data-2prakashNoch keine Bewertungen

- Incheon International Airport Passenger Terminal 2Dokument3 SeitenIncheon International Airport Passenger Terminal 2sophiaardfslkfNoch keine Bewertungen

- PTCL Data Centre FinalDokument32 SeitenPTCL Data Centre FinalZohaib Chachar100% (2)

- Sawyer's Gas Turbine Combustor - Chapter 50001Dokument61 SeitenSawyer's Gas Turbine Combustor - Chapter 50001Venkat AthmanathanNoch keine Bewertungen

- Lecture 4: Quality Philosophy and Management Strategies: 1.0.1 William Edwards DemingDokument3 SeitenLecture 4: Quality Philosophy and Management Strategies: 1.0.1 William Edwards DemingDiego PulidoNoch keine Bewertungen

- ES 096 Weldable Structural SteelsDokument19 SeitenES 096 Weldable Structural SteelsMichael CovillNoch keine Bewertungen

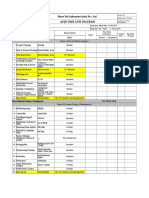

- Shree Ved Industries India Pvt. Ltd. Apqp Time Line DiagramDokument2 SeitenShree Ved Industries India Pvt. Ltd. Apqp Time Line DiagramS. R. OvhalNoch keine Bewertungen

- 2-95 pgs-OK ISO 9000-2000 LEAD AUDITOR COURSEDokument96 Seiten2-95 pgs-OK ISO 9000-2000 LEAD AUDITOR COURSEDaun KelorNoch keine Bewertungen

- Top 10 Excel formulas for data analysisDokument7 SeitenTop 10 Excel formulas for data analysisTamseel ShahajahanNoch keine Bewertungen

- Accountancy Refresher Course on Quantitative TechniquesDokument4 SeitenAccountancy Refresher Course on Quantitative Techniquesshamel marohom100% (2)

- Plant and Process Engineering WorkflowDokument43 SeitenPlant and Process Engineering WorkflowSuhas Jadhal100% (12)

- Process Analysis BatchingDokument2 SeitenProcess Analysis Batchingaditya162Noch keine Bewertungen

- ChapterDokument60 SeitenChapterMa ThiNoch keine Bewertungen

- Control Valves PDFDokument6 SeitenControl Valves PDFIlham Bayu TiasmoroNoch keine Bewertungen

- Microsoft 365 E5 Update Webinar January 15 2019Dokument26 SeitenMicrosoft 365 E5 Update Webinar January 15 2019written4meNoch keine Bewertungen