Das könnte Ihnen auch gefallen

- Beta Anomaly An Ex-Ante Tail RiskDokument104 SeitenBeta Anomaly An Ex-Ante Tail RiskDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Why The Euro Will Rival The Dollar PDFDokument25 SeitenWhy The Euro Will Rival The Dollar PDFDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Claudia Jones Nuclear TestingDokument25 SeitenClaudia Jones Nuclear TestingDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Continuity Change State of Process of Task ofDokument1 SeiteContinuity Change State of Process of Task ofDaniel Lee Eisenberg JacobsNoch keine Bewertungen

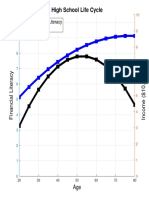

- High School Life Cycle: Financial Literacy IncomeDokument1 SeiteHigh School Life Cycle: Financial Literacy IncomeDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Theophilus Capital Against: Fisk Labor1Dokument9 SeitenTheophilus Capital Against: Fisk Labor1Daniel Lee Eisenberg Jacobs100% (1)

- Conference Group For Central European History of The American Historical AssociationDokument9 SeitenConference Group For Central European History of The American Historical AssociationDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Individualization of Robo-AdviceDokument8 SeitenIndividualization of Robo-AdviceDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Karl Kautsky Republic and Social Democra PDFDokument4 SeitenKarl Kautsky Republic and Social Democra PDFDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Borel Sets PDFDokument181 SeitenBorel Sets PDFDaniel Lee Eisenberg Jacobs100% (1)

- Cover FERCDokument1 SeiteCover FERCDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- 1st International: Djacobs November 2020Dokument5 Seiten1st International: Djacobs November 2020Daniel Lee Eisenberg JacobsNoch keine Bewertungen

- Gpebook PDFDokument332 SeitenGpebook PDFDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- The Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDokument8 SeitenThe Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Bank Loan Loss ProvisioningDokument17 SeitenBank Loan Loss ProvisioningDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Necessary and Sufficient Conditions For Dynamic OptimizationDokument18 SeitenNecessary and Sufficient Conditions For Dynamic OptimizationDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Teach-In: Government of The People, by The People, For The PeopleDokument24 SeitenTeach-In: Government of The People, by The People, For The PeopleDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Simple BeamerDokument25 SeitenSimple BeamerDaniel Lee Eisenberg JacobsNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Catalog Man 1Dokument116 SeitenCatalog Man 1Petrov AndreiNoch keine Bewertungen

- Manual Elspec SPG 4420Dokument303 SeitenManual Elspec SPG 4420Bairon Alvira ManiosNoch keine Bewertungen

- Biopsy: Assessment Diagnosis Planning Intervention Rationale EvaluationDokument5 SeitenBiopsy: Assessment Diagnosis Planning Intervention Rationale EvaluationDan HizonNoch keine Bewertungen

- Definition of Logistics ManagementDokument4 SeitenDefinition of Logistics ManagementzamaneNoch keine Bewertungen

- Dragons and Winged SerpentsDokument5 SeitenDragons and Winged SerpentsYuna Raven100% (1)

- Academic Program Required Recommended Academic Program Required RecommendedDokument1 SeiteAcademic Program Required Recommended Academic Program Required Recommendedonur scribdNoch keine Bewertungen

- Grand Vitara 2005Dokument35 SeitenGrand Vitara 2005PattyaaNoch keine Bewertungen

- An Infallible JusticeDokument7 SeitenAn Infallible JusticeMani Gopal DasNoch keine Bewertungen

- Wind Load CompututationsDokument31 SeitenWind Load Compututationskim suarezNoch keine Bewertungen

- The Coffee Shop Easy Reading - 152542Dokument1 SeiteThe Coffee Shop Easy Reading - 152542Fc MakmurNoch keine Bewertungen

- DA-42 Performance Calculator v2.3.1Dokument23 SeitenDA-42 Performance Calculator v2.3.1DodgeHemi1Noch keine Bewertungen

- Iron FistDokument2 SeitenIron FistVictor PileggiNoch keine Bewertungen

- 5 Kingdoms of OrganismsDokument13 Seiten5 Kingdoms of OrganismsChoirul Anam100% (2)

- Content For Essay and Paragraph Writing On Maritime HistoryDokument15 SeitenContent For Essay and Paragraph Writing On Maritime HistoryRaju KumarNoch keine Bewertungen

- Cad, CamDokument16 SeitenCad, CamRakhi Mol BVNoch keine Bewertungen

- 020 Basketball CourtDokument4 Seiten020 Basketball CourtMohamad TaufiqNoch keine Bewertungen

- Our Lady of Fatima University: College of Business & AccountancyDokument17 SeitenOur Lady of Fatima University: College of Business & AccountancyCLARIN GERALDNoch keine Bewertungen

- 7 Stages of NafsDokument7 Seiten7 Stages of NafsLilyNoch keine Bewertungen

- TRL Explanations - 1Dokument4 SeitenTRL Explanations - 1Ana DulceNoch keine Bewertungen

- Catalogue Mp200Dokument33 SeitenCatalogue Mp200Adrian TudorNoch keine Bewertungen

- Time Series - Practical ExercisesDokument9 SeitenTime Series - Practical ExercisesJobayer Islam TunanNoch keine Bewertungen

- Pre-Test First QTR 2022-2023Dokument3 SeitenPre-Test First QTR 2022-2023anna marie mangulabnanNoch keine Bewertungen

- Journal Homepage: - : IntroductionDokument9 SeitenJournal Homepage: - : IntroductionIJAR JOURNALNoch keine Bewertungen

- Construction Companies in AlbaniaDokument17 SeitenConstruction Companies in AlbaniaPacific HRNoch keine Bewertungen

- Barium Chloride 2h2o LRG MsdsDokument3 SeitenBarium Chloride 2h2o LRG MsdsAnas GiselNoch keine Bewertungen

- OKM 54MP FlyerDokument1 SeiteOKM 54MP FlyerJohnsonNoch keine Bewertungen

- Load ScheduleDokument8 SeitenLoad SchedulemerebookNoch keine Bewertungen

- Danh M C AHTN 2017 - HS Code 2017 PDFDokument564 SeitenDanh M C AHTN 2017 - HS Code 2017 PDFBao Ngoc Nguyen100% (1)

- A Practical Approach To Classical YogaDokument39 SeitenA Practical Approach To Classical Yogaabhilasha_yadav_1Noch keine Bewertungen

- Pastor O. I. Kirk, SR D.D LIFE Celebration BookDokument63 SeitenPastor O. I. Kirk, SR D.D LIFE Celebration Booklindakirk1100% (1)