Enhancing Governance through internal audit

Internal Audit Overview

Conference on Public Internal Control in the EU

May 15, 2014

Thijs Smit

President

Enhancing Governance through internal audit

Introduction

Thijs Smit

ECIIA

Internal Audit

Definition

3 lines of defence

2020

Quality Assurance

Audit Committee

Agenda

Enhancing Governance through internal audit

Thijs Smit

PTT KPN 1978 1997

Corus 1997 2000

Ahold 2000 2005

SNS REAAL 2006 2010

SHV 2011

Enhancing Governance through internal audit

European Confederation of Institutes of

Internal Auditing

The ECIIA represents the beacon of the Internal Audit

profession in the wider geographic area of Europe and the

Mediterranean basin

37 countries

40.000 members

Primary objective of furthering the development of

corporate governance and internal audit through

knowledge sharing, key relationships and the

regulatory environment oversight

Enhancing Governance through internal audit

Definition Internal Audit

Internal auditing is an objective assurance activity that

benefits an organization by providing independent evaluations,

advice,and insight on governance, risk management

and internal control.

Enhancing Governance through internal audit

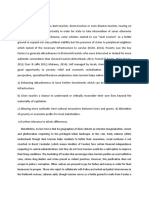

1

st

line of defence 2

nd

line of defence 3

rd

line of defence

Internal

Audit

Actuarial Function

Risk Management

E

x

t

e

r

n

a

l

a

u

d

i

t

R

e

g

u

l

a

t

o

r

Management

Controls

Internal

Control

Measures

Compliance

Governing Body / Audit Committee

Senior Management

The three lines of defence model

Enhancing Governance through internal audit

Less emphasis on controls and more on risk management

and governance

New risks to consider: reputational damage,

Audit plan reviewed more regularly

Technology: Mega Data and GRC

More focus on key risks, key recommendations

More operational skills and emphasis on soft skills

(communication, project management,)

*IA Magazine : interviews of thought leaders , 2013 Pulse Survey, New risks for internal audit

In the public sector

Internal audit in 2020*

Enhancing Governance through internal audit

Quality Assurance

Audit the Auditor

Crucial to bring profession to the next level

Mandatory in certain situations

Enhancing Governance through internal audit

Oversee Internal Audit

Ensure independence

Assess quality

Direct reporting line

Assess quality external Auditor

Review risks

Oversee financial reporting

Coordinate assurance functions

Review internal control framework

Audit Committee Roles

Enhancing Governance through internal audit

www.eciia.eu

Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Working Paper 1Dokument40 SeitenWorking Paper 1Alexandru VasileNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- IPPF Exposure Draft EnglishDokument26 SeitenIPPF Exposure Draft EnglishAhsan Iftikhar QureshiNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Rbi A ManualDokument344 SeitenRbi A ManualAlexandru VasileNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- New Document Microsoft Office WordDokument4 SeitenNew Document Microsoft Office WordAlexandru VasileNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Quality Assurance and Improvement Program Pa - 1300-1-May-2015Dokument1 SeiteQuality Assurance and Improvement Program Pa - 1300-1-May-2015Alexandru VasileNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- 17 Principles Internal ControlDokument1 Seite17 Principles Internal ControlAlexandru VasileNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Un Pan 024135Dokument54 SeitenUn Pan 024135Alexandru VasileNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Audit Risk in A Brave New WorldDokument6 SeitenAudit Risk in A Brave New World0730118008Noch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Implementation Guides: I G1000 - Purpose Authority and Responsibility IG2110 - GovernanceDokument1 SeiteImplementation Guides: I G1000 - Purpose Authority and Responsibility IG2110 - GovernanceAlexandru VasileNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- Fraud PaperDokument80 SeitenFraud PaperAlexandru VasileNoch keine Bewertungen

- New Document Microsoft Office WordDokument1 SeiteNew Document Microsoft Office WordAlexandru VasileNoch keine Bewertungen

- Rbi A ImplementingDokument24 SeitenRbi A ImplementingAlexandru VasileNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Rbi A ImplementingDokument24 SeitenRbi A ImplementingAlexandru VasileNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Raport Tara 2014Dokument91 SeitenRaport Tara 2014Laura IonescuNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- AuditRiskModelDokument17 SeitenAuditRiskModelAlexandru VasileNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Public Internal Control Systems in The European UnionDokument11 SeitenPublic Internal Control Systems in The European UnionAlexandru VasileNoch keine Bewertungen

- Ebook Connecting The Dots Building Internal Audit ValueDokument36 SeitenEbook Connecting The Dots Building Internal Audit ValueAlexandru VasileNoch keine Bewertungen

- 2012 IIA Standards UpdateDokument34 Seiten2012 IIA Standards UpdateAlexandru VasileNoch keine Bewertungen

- Statement On RIsk Management and Internal COntrolDokument18 SeitenStatement On RIsk Management and Internal COntrolkien91Noch keine Bewertungen

- 7 Attributes of Highly Effective Internal AuditorsDokument12 Seiten7 Attributes of Highly Effective Internal AuditorsMan KapNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Coso Training - New York StateDokument35 SeitenCoso Training - New York StateAlexandru VasileNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- Training Manuals CollectionDokument9 SeitenTraining Manuals CollectionAlexandru VasileNoch keine Bewertungen

- CD 04 Stakeholder ExpectationsDokument2 SeitenCD 04 Stakeholder ExpectationsAlexandru VasileNoch keine Bewertungen

- Anexa COCOF-2013Dokument22 SeitenAnexa COCOF-2013CJNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- COSO in The Cyber Age - FULL - r11Dokument28 SeitenCOSO in The Cyber Age - FULL - r11Alexandru VasileNoch keine Bewertungen

- 1 Agenda Final European Territorial Cooperation 2014 2020 Indicators 02 2013Dokument2 Seiten1 Agenda Final European Territorial Cooperation 2014 2020 Indicators 02 2013Alexandru VasileNoch keine Bewertungen

- Audit ManualDokument185 SeitenAudit Manualandysupa100% (4)

- Assuring Quality of Internal Audit in the EUDokument10 SeitenAssuring Quality of Internal Audit in the EUAlexandru VasileNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- CD 07 A Internal ControlDokument8 SeitenCD 07 A Internal ControlAlexandru VasileNoch keine Bewertungen

- The Impact of Internal Control System On The Financial Management of An OrganizationDokument7 SeitenThe Impact of Internal Control System On The Financial Management of An OrganizationAlexandru VasileNoch keine Bewertungen

- Peace Corps Malawi Country Crime StatisticsDokument11 SeitenPeace Corps Malawi Country Crime StatisticsAccessible Journal Media: Peace Corps DocumentsNoch keine Bewertungen

- Wepik Exploring The Impact of Internet Addiction Within The Realm of Media Psychology 20231106202202XcXLDokument8 SeitenWepik Exploring The Impact of Internet Addiction Within The Realm of Media Psychology 20231106202202XcXLarsitaagrawalaNoch keine Bewertungen

- Slum Tourism ArticlesDokument7 SeitenSlum Tourism ArticlesKrystalline Naldoza DugangNoch keine Bewertungen

- AppendixDokument113 SeitenAppendixapi-277248806Noch keine Bewertungen

- The Struggles Women Faces in Male Chauvinistic SocietyDokument12 SeitenThe Struggles Women Faces in Male Chauvinistic SocietyNeha Sudhan100% (1)

- Draft Resolution 1.1 SOCHUM LGSMUN '13Dokument8 SeitenDraft Resolution 1.1 SOCHUM LGSMUN '13Hamza HashimNoch keine Bewertungen

- Difference Between Diversity and Equal OpportunitiesDokument3 SeitenDifference Between Diversity and Equal OpportunitiesAyomide Muyiwa-OjeladeNoch keine Bewertungen

- 1.2 Learning Activity 2Dokument2 Seiten1.2 Learning Activity 2Enrico ReyesNoch keine Bewertungen

- DRW 306 (Module 2) VillarinDokument7 SeitenDRW 306 (Module 2) VillarinRomel Ayson VillarinNoch keine Bewertungen

- Ebook Ebook PDF Race Ethnicity Gender and Class The Sociology of Group Conflict and Change 8th Edition PDFDokument27 SeitenEbook Ebook PDF Race Ethnicity Gender and Class The Sociology of Group Conflict and Change 8th Edition PDFseth.bruno786100% (29)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Role of Education On Poverty ReductionThe Case StudyDokument6 SeitenRole of Education On Poverty ReductionThe Case Studyzoya gulNoch keine Bewertungen

- POCSODokument12 SeitenPOCSOPragya RaniNoch keine Bewertungen

- Challenging Prejudice WorksheetDokument3 SeitenChallenging Prejudice WorksheetJessan Ybañez JoreNoch keine Bewertungen

- SSRN Id2079750Dokument33 SeitenSSRN Id2079750Ahmed MohammedNoch keine Bewertungen

- Hva B3Dokument1 SeiteHva B3aldhilaNoch keine Bewertungen

- How to Deal with and Overcome Body ShamingDokument12 SeitenHow to Deal with and Overcome Body ShamingAung PhyoeNoch keine Bewertungen

- CCAP CIR Letter of Consent (Annex B) - CCAP CIR Letter of Consent (Annex B)Dokument1 SeiteCCAP CIR Letter of Consent (Annex B) - CCAP CIR Letter of Consent (Annex B)Ira Angelo CorderoNoch keine Bewertungen

- Gender Inequality in Workplace Glass CeilingDokument6 SeitenGender Inequality in Workplace Glass CeilingdeviNoch keine Bewertungen

- HR and IHLDokument7 SeitenHR and IHLahmedistiakNoch keine Bewertungen

- Nativism DBQ Activity Packet EditDokument3 SeitenNativism DBQ Activity Packet Editapi-200885658Noch keine Bewertungen

- Child Labor - The Snag and Way OutDokument1 SeiteChild Labor - The Snag and Way OutReyvennNoch keine Bewertungen

- Life of Students With OFW ParentsDokument16 SeitenLife of Students With OFW ParentsCrisa Mae G. VillaesterNoch keine Bewertungen

- Chapter OneDokument43 SeitenChapter OneAkindehinde RidwanNoch keine Bewertungen

- Indian DemocracyDokument16 SeitenIndian DemocracyVirender SinghNoch keine Bewertungen

- IndianDivorceActExplainedDokument6 SeitenIndianDivorceActExplainedMayank SharmaNoch keine Bewertungen

- EDUC 5710 Unit 1 Discussion Assignment Good Example 3Dokument2 SeitenEDUC 5710 Unit 1 Discussion Assignment Good Example 3Abed OthmanNoch keine Bewertungen

- Data ProtectionDokument3 SeitenData ProtectionAishwarya PandeyNoch keine Bewertungen

- Elc231 3A18 (Evaluative Commentary)Dokument2 SeitenElc231 3A18 (Evaluative Commentary)fenny yabinNoch keine Bewertungen

- Top Five Countries With Highest Rates of Child ProstitutionDokument5 SeitenTop Five Countries With Highest Rates of Child ProstitutionThavamNoch keine Bewertungen

- When Ethics and Law Collide: Social Workers' DilemmasDokument3 SeitenWhen Ethics and Law Collide: Social Workers' DilemmasTugonon M Leo RoswaldNoch keine Bewertungen