Das könnte Ihnen auch gefallen

- Essay On Barclays Bank Marketing PlanDokument24 SeitenEssay On Barclays Bank Marketing Plannprash123Noch keine Bewertungen

- Electronic Financial Services: Technology and ManagementVon EverandElectronic Financial Services: Technology and ManagementBewertung: 5 von 5 Sternen5/5 (1)

- Financial Analysis of BarclaysDokument17 SeitenFinancial Analysis of BarclaysGohar100% (2)

- Business Partnering A Complete Guide - 2020 EditionVon EverandBusiness Partnering A Complete Guide - 2020 EditionNoch keine Bewertungen

- Capital Investment Appraisal in Retail Business Management: Sainsbury's As A Case StudyDokument6 SeitenCapital Investment Appraisal in Retail Business Management: Sainsbury's As A Case StudyIOSRjournalNoch keine Bewertungen

- Marketing PlanDokument17 SeitenMarketing PlanSteve WeberNoch keine Bewertungen

- Fintech in Asia Pacific: Digital Payment Platforms: October 2019Dokument42 SeitenFintech in Asia Pacific: Digital Payment Platforms: October 2019VaishnaviRaviNoch keine Bewertungen

- 2013 Quintiles Annual Report - Final PDFDokument147 Seiten2013 Quintiles Annual Report - Final PDFLate ArtistNoch keine Bewertungen

- A Project Study On Unethical Behavior of Barclays BankDokument21 SeitenA Project Study On Unethical Behavior of Barclays BankAŋoop KrīşħŋặNoch keine Bewertungen

- Introduction To The Business of Banking and Financial-ServicesDokument30 SeitenIntroduction To The Business of Banking and Financial-ServicesWan ThengNoch keine Bewertungen

- Digital BankingDokument32 SeitenDigital BankingAnshul VermaNoch keine Bewertungen

- Role of Banking in International BusinessDokument15 SeitenRole of Banking in International Businesstheaaj100% (2)

- Chapter 1Dokument27 SeitenChapter 1Nicole JoanNoch keine Bewertungen

- 13813-Case Study SolutionsDokument7 Seiten13813-Case Study SolutionsMaryam KhanNoch keine Bewertungen

- Barclays Strategicmanagement2Dokument45 SeitenBarclays Strategicmanagement2Kushan Kumar100% (2)

- Case Study - Barclays BankDokument1 SeiteCase Study - Barclays BankMehedi Hassan Rana100% (2)

- JPR 54079 DailmerAG EquityResearch Report 1303Dokument35 SeitenJPR 54079 DailmerAG EquityResearch Report 1303André Fonseca100% (1)

- Profile: AT&T Inc (T.N)Dokument6 SeitenProfile: AT&T Inc (T.N)JavierAlfonsoGomezZamoraNoch keine Bewertungen

- MTN PitchbookDokument21 SeitenMTN PitchbookGideon Antwi Boadi100% (1)

- Lending ClubDokument2 SeitenLending ClubNaman JainNoch keine Bewertungen

- Transactions BankingDokument27 SeitenTransactions BankingSơ Ri Muối100% (1)

- The Hertz Corporation Chapter 11 FilingDokument27 SeitenThe Hertz Corporation Chapter 11 FilingTradeHawkNoch keine Bewertungen

- Barclay Case StudyDokument8 SeitenBarclay Case StudySujit S NairNoch keine Bewertungen

- Cash Conversion CycleDokument7 SeitenCash Conversion Cyclebarakkat72Noch keine Bewertungen

- 2020 q4 Earnings Results PresentationDokument14 Seiten2020 q4 Earnings Results PresentationZerohedgeNoch keine Bewertungen

- M Commerce and Ecomerce 2019 .1Dokument10 SeitenM Commerce and Ecomerce 2019 .1isabella DiazNoch keine Bewertungen

- Yell Case Exhibits Growth RatesDokument12 SeitenYell Case Exhibits Growth RatesJames MorinNoch keine Bewertungen

- Tackling Tax Avoidance Evasion and Other Forms of Non-Compliance WebDokument68 SeitenTackling Tax Avoidance Evasion and Other Forms of Non-Compliance WebT HNoch keine Bewertungen

- CB Insights 2020 Fintech 250: Company Sector CategoryDokument3 SeitenCB Insights 2020 Fintech 250: Company Sector CategoryBánh NgôNoch keine Bewertungen

- BCG InsideSherpa Core Strategy - Telco (Task 2 Model Answer) - FinalDokument10 SeitenBCG InsideSherpa Core Strategy - Telco (Task 2 Model Answer) - FinalburaNoch keine Bewertungen

- World Fintech Report 2017Dokument48 SeitenWorld Fintech Report 2017morellimarc100% (2)

- VirginDokument14 SeitenVirginGururaj Prakash75% (4)

- Final Report Ebl and SCBDokument30 SeitenFinal Report Ebl and SCBRasadul Hasan Rasel100% (1)

- Banking On Our FutureDokument21 SeitenBanking On Our FutureHamilton Place StrategiesNoch keine Bewertungen

- Special Emphasis On Working Capital Finance of Jamuna Bank Ltd.Dokument18 SeitenSpecial Emphasis On Working Capital Finance of Jamuna Bank Ltd.Imam Hasan Sazeeb100% (1)

- Presentation of Banking and OperationsDokument13 SeitenPresentation of Banking and OperationsGurinder M. IshpunaniNoch keine Bewertungen

- Segment AnalysisDokument53 SeitenSegment AnalysisamanNoch keine Bewertungen

- Econet AR 2011Dokument75 SeitenEconet AR 2011Kristi Duran100% (1)

- About Oracle Financial Services SoftwareDokument20 SeitenAbout Oracle Financial Services SoftwareAroosh KhalidNoch keine Bewertungen

- New Heritage Doll Company Case StudyDokument10 SeitenNew Heritage Doll Company Case StudyRAJATH JNoch keine Bewertungen

- Colgate Financial Model SolvedDokument33 SeitenColgate Financial Model SolvedVvb SatyanarayanaNoch keine Bewertungen

- Stryker Corporation: Capital BudgetingDokument4 SeitenStryker Corporation: Capital BudgetingShakthi RaghaviNoch keine Bewertungen

- Annual ReportDokument193 SeitenAnnual ReportShafali R ChandranNoch keine Bewertungen

- SaasplanecomodelDokument2 SeitenSaasplanecomodelapi-336055432Noch keine Bewertungen

- Barclays Statement of Facts From The Justice DepartmentDokument23 SeitenBarclays Statement of Facts From The Justice DepartmentDealBookNoch keine Bewertungen

- Marketing Plan Report ItradeDokument8 SeitenMarketing Plan Report ItradeVkNoch keine Bewertungen

- Elements of A Bank Marketing PlanDokument7 SeitenElements of A Bank Marketing PlanBogdan ColdeaNoch keine Bewertungen

- Financial System of China: Lecturer - Oleg Deev Oleg@mail - Muni.czDokument37 SeitenFinancial System of China: Lecturer - Oleg Deev Oleg@mail - Muni.czSaurabh BhirudNoch keine Bewertungen

- Assessment 3 (Dominos Case Study)Dokument5 SeitenAssessment 3 (Dominos Case Study)RishabNoch keine Bewertungen

- CRM in BankingDokument11 SeitenCRM in BankingleoniNoch keine Bewertungen

- 5 - G2B and G2C Pakistan - Mudasir Rasool - 13879Dokument4 Seiten5 - G2B and G2C Pakistan - Mudasir Rasool - 13879saadriazNoch keine Bewertungen

- Global Oil & Gas - 130813 - BarclaysDokument56 SeitenGlobal Oil & Gas - 130813 - Barclaysalokgupta87Noch keine Bewertungen

- Monetary Policy of BangladeshDokument26 SeitenMonetary Policy of Bangladeshsuza054Noch keine Bewertungen

- Credit Assignment 1Dokument5 SeitenCredit Assignment 1Marock Rajwinder0% (1)

- PESTL Singapore - Strategic Analysis On SingTelDokument21 SeitenPESTL Singapore - Strategic Analysis On SingTelWooGimChuan100% (5)

- Impact of Sub-Prime Mortgage Crisis On Major UK BanksDokument54 SeitenImpact of Sub-Prime Mortgage Crisis On Major UK BanksIdris ShittuNoch keine Bewertungen

- RBS TbeDokument7 SeitenRBS Tbeatulbhosale11Noch keine Bewertungen

- A Critical Essay On International FinanceDokument11 SeitenA Critical Essay On International FinanceDakshesh PatelNoch keine Bewertungen

- Original Content and IntrodDokument36 SeitenOriginal Content and IntrodBlessing UmorenNoch keine Bewertungen

- Solution Manual Financial Institution Management 3rd Edition by Helen Lange SLM1085Dokument8 SeitenSolution Manual Financial Institution Management 3rd Edition by Helen Lange SLM1085thar adelei100% (1)

- Module 2a - AR RecapDokument10 SeitenModule 2a - AR RecapChen HaoNoch keine Bewertungen

- Chapter 8Dokument17 SeitenChapter 8Meo XinkNoch keine Bewertungen

- Transfer PricingDokument14 SeitenTransfer PricingDiana Rose BassigNoch keine Bewertungen

- How To Develop A CRM RoadmapDokument3 SeitenHow To Develop A CRM Roadmapfb3003Noch keine Bewertungen

- Help FileDokument92 SeitenHelp FileAnirudh NarlaNoch keine Bewertungen

- Organization of Production: Test IiDokument7 SeitenOrganization of Production: Test IiKamarul NizamNoch keine Bewertungen

- Coa Circular 2008-002Dokument2 SeitenCoa Circular 2008-002bolNoch keine Bewertungen

- Budgetary Control System - HeritageDokument82 SeitenBudgetary Control System - HeritageSwathi Manthena50% (4)

- Data Analytics by Management Accountants: Gary Spraakman Cristobal Sanchez-Rodriguez Carol Anne Tuck-RiggsDokument21 SeitenData Analytics by Management Accountants: Gary Spraakman Cristobal Sanchez-Rodriguez Carol Anne Tuck-Riggsمعن الفاعوريNoch keine Bewertungen

- Training Needs Assessment Practices in Corporate Sector of PakistanDokument7 SeitenTraining Needs Assessment Practices in Corporate Sector of PakistanWan JaiNoch keine Bewertungen

- "Don't Bother Me, I Can't Cope": Activity Activity Time Immediate (Seconds) PredecessorDokument3 Seiten"Don't Bother Me, I Can't Cope": Activity Activity Time Immediate (Seconds) PredecessorARYA BARANWAL IPM 2018 BatchNoch keine Bewertungen

- Top 50 Management Consulting Firms Guide PDFDokument165 SeitenTop 50 Management Consulting Firms Guide PDFSunny Naresh ManchandaNoch keine Bewertungen

- Chapter Three Golis UniversityDokument40 SeitenChapter Three Golis UniversityCabdixakiim-Tiyari Cabdillaahi AadenNoch keine Bewertungen

- Kal Atm Software Trends and Analysis 2014 PDFDokument61 SeitenKal Atm Software Trends and Analysis 2014 PDFlcarrionNoch keine Bewertungen

- Scope of Strategic MarketingDokument3 SeitenScope of Strategic MarketingM Fani Malik100% (1)

- On BoardingDokument15 SeitenOn BoardingAnkita Jain100% (3)

- Cost Sheet Practical ProblemsDokument2 SeitenCost Sheet Practical Problemssameer_kini100% (1)

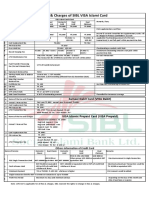

- Fees and Charges of SIBL Islami CardDokument1 SeiteFees and Charges of SIBL Islami CardMd YusufNoch keine Bewertungen

- ACompanyDokument12 SeitenACompanypiyushffrtNoch keine Bewertungen

- Growth & Changing Structure of Non-Banking Financial InstitutionsDokument14 SeitenGrowth & Changing Structure of Non-Banking Financial InstitutionsPuneet KaurNoch keine Bewertungen

- Group 1 Case Study 7 - AcerDokument38 SeitenGroup 1 Case Study 7 - AcerVõ Thị Xuân HạnhNoch keine Bewertungen

- Nfjpia Nmbe Auditing 2017 AnsDokument10 SeitenNfjpia Nmbe Auditing 2017 AnsSamieeNoch keine Bewertungen

- Simulation of The Preparation of The Work Unit (Satker) Financial StatementsDokument23 SeitenSimulation of The Preparation of The Work Unit (Satker) Financial StatementskarismaNoch keine Bewertungen

- GPAC Purple Roadshow Presentation 01.07.18Dokument41 SeitenGPAC Purple Roadshow Presentation 01.07.18Ala BasterNoch keine Bewertungen

- Internal and External Vacancy Announcement (Laboratory & Logistics Officer)Dokument2 SeitenInternal and External Vacancy Announcement (Laboratory & Logistics Officer)Phr InitiativeNoch keine Bewertungen

- CA IPCC Company Law Last Minute Revision Notes in PDF Format-3Dokument29 SeitenCA IPCC Company Law Last Minute Revision Notes in PDF Format-3Naman JainNoch keine Bewertungen

- An Introduction To Integrated Marketing CommunicationsDokument42 SeitenAn Introduction To Integrated Marketing CommunicationsShuvroNoch keine Bewertungen

- Appendix A The Iia Cia Exam Syllabus and Cross-ReferencesDokument4 SeitenAppendix A The Iia Cia Exam Syllabus and Cross-ReferencesSehra GULNoch keine Bewertungen

- ConceptualizingDokument8 SeitenConceptualizingHyacinth'Faith Espesor IIINoch keine Bewertungen