Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Role of Persians at The Mughal CourtDokument418 SeitenRole of Persians at The Mughal Courtsunnivoice67% (3)

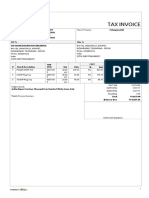

- Inv-0059 Sri Maheshwari EngineeringDokument1 SeiteInv-0059 Sri Maheshwari EngineeringSRIKAR DHANOORINoch keine Bewertungen

- University ListDokument3 SeitenUniversity ListSHARATH KUMARNoch keine Bewertungen

- Abbasuddin AhmedDokument2 SeitenAbbasuddin AhmedMd. Ashfaqur RhamanNoch keine Bewertungen

- Name of Employee Date of Birth (DD-MM-Yyyy) Contact NumberDokument3 SeitenName of Employee Date of Birth (DD-MM-Yyyy) Contact NumberkurutalaNoch keine Bewertungen

- Gender Discrimination in Mahesh Dattani's Play "Dance Like A Man" and "Tara" - A Critical AnalysisDokument4 SeitenGender Discrimination in Mahesh Dattani's Play "Dance Like A Man" and "Tara" - A Critical AnalysisIJELS Research JournalNoch keine Bewertungen

- Were Temple Gopurams in South India Originally Colorful or Is This A Recent ChangeDokument3 SeitenWere Temple Gopurams in South India Originally Colorful or Is This A Recent ChangeNRV APPASAMYNoch keine Bewertungen

- Mahatma GandhiDokument4 SeitenMahatma GandhiKyle McdonaldNoch keine Bewertungen

- EP-501, Evolution of Indian Economy Midterm: Submitted By: Prashun Pranav (CISLS)Dokument8 SeitenEP-501, Evolution of Indian Economy Midterm: Submitted By: Prashun Pranav (CISLS)rumiNoch keine Bewertungen

- 2-An Assessment of Francois Berniers TravelDokument31 Seiten2-An Assessment of Francois Berniers TravelRathindra Narayan BhattacharyaNoch keine Bewertungen

- Topic 13: History Handouts Prepared by Usman Hameed 03224557967Dokument3 SeitenTopic 13: History Handouts Prepared by Usman Hameed 03224557967Usman KhanNoch keine Bewertungen

- Important Awards and Honours 2020 - Free PDFDokument14 SeitenImportant Awards and Honours 2020 - Free PDFsunny kumarNoch keine Bewertungen

- Cabinet Mission PlanDokument9 SeitenCabinet Mission PlanRana Ali MujtabaNoch keine Bewertungen

- Full List of LkoDokument33 SeitenFull List of LkoDixitVishal86% (7)

- Region ADokument98 SeitenRegion Aartresurrected23Noch keine Bewertungen

- Myths and Realities of Tribal Education: A Primary Study in Similipal Area of OdishaDokument6 SeitenMyths and Realities of Tribal Education: A Primary Study in Similipal Area of OdishainventionjournalsNoch keine Bewertungen

- His Mid FileDokument13 SeitenHis Mid FileOmar Fahim Khan 1911758030Noch keine Bewertungen

- 22 2 HooperDokument28 Seiten22 2 HooperBahuvirupakshaNoch keine Bewertungen

- India's Five Year Plan - I To XI - 1951-56 To 2007-12 (In 2 Volumes)Dokument4 SeitenIndia's Five Year Plan - I To XI - 1951-56 To 2007-12 (In 2 Volumes)Sumanta Shee100% (1)

- Sushma Swaraj: Smt. Nirmala Sitharaman Minister of Defence Government of India New DelhiDokument20 SeitenSushma Swaraj: Smt. Nirmala Sitharaman Minister of Defence Government of India New DelhiRuchit SharmaNoch keine Bewertungen

- Addresses 967Dokument16 SeitenAddresses 967prahladraiNoch keine Bewertungen

- The Textile MagazineDokument110 SeitenThe Textile MagazineKayPeaB100% (1)

- Rs100 463 Channels ListDokument26 SeitenRs100 463 Channels ListSubhadip MitraNoch keine Bewertungen

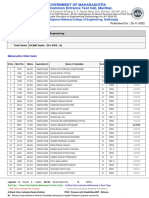

- 6803 - Sant Gajanan Maharaj College of Engineering, GadhinglajDokument10 Seiten6803 - Sant Gajanan Maharaj College of Engineering, Gadhinglajrohit sharmaNoch keine Bewertungen

- 74rt IndependenceDokument24 Seiten74rt Independencesatyagowri abbireddiNoch keine Bewertungen

- Adi Dhakeswari Benarasi Kuthi Benarasi Kuthi BenarasiDokument3 SeitenAdi Dhakeswari Benarasi Kuthi Benarasi Kuthi BenarasiAkhil DaveNoch keine Bewertungen

- Project On ItcDokument7 SeitenProject On ItcAnonymous 6LQLwsNoch keine Bewertungen

- Our Country IndiaDokument16 SeitenOur Country Indiasuja venugopalNoch keine Bewertungen

- Textbook CultureDokument4 SeitenTextbook CultureAbhinavNoch keine Bewertungen

- E&S PPT FormatDokument6 SeitenE&S PPT FormatKishoreNoch keine Bewertungen