Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Acca F8 (INT) Question Dec 2007Dokument5 SeitenAcca F8 (INT) Question Dec 2007elvesjayNoch keine Bewertungen

- Dec 2007 AnDokument11 SeitenDec 2007 AnMohammad Ariful IslamNoch keine Bewertungen

- Fundamentals Level - Skills Module, F8 (INT) Audit and AssuranceDokument12 SeitenFundamentals Level - Skills Module, F8 (INT) Audit and AssurancekhengmaiNoch keine Bewertungen

- Audit and Internal ReviewDokument7 SeitenAudit and Internal ReviewkhengmaiNoch keine Bewertungen

- Part 2 Examination - Paper 2.6 (INT) Audit and Internal ReviewDokument12 SeitenPart 2 Examination - Paper 2.6 (INT) Audit and Internal ReviewkhengmaiNoch keine Bewertungen

- Acca f8 Past YearDokument5 SeitenAcca f8 Past YearAngela AdamsNoch keine Bewertungen

- f8 Pilot Paper IntDokument20 Seitenf8 Pilot Paper IntXin LiNoch keine Bewertungen

- Audit and Internal ReviewDokument5 SeitenAudit and Internal ReviewkhengmaiNoch keine Bewertungen

- Audit and Internal ReviewDokument6 SeitenAudit and Internal ReviewkhengmaiNoch keine Bewertungen

- Audit and Internal ReviewDokument5 SeitenAudit and Internal ReviewkhengmaiNoch keine Bewertungen

- Part 2 Examination - Paper 2.6 (INT) Audit and Internal ReviewDokument12 SeitenPart 2 Examination - Paper 2.6 (INT) Audit and Internal ReviewkhengmaiNoch keine Bewertungen

- Part 2 - Examination - Paper 2.6 (INT) Audit and InternalDokument16 SeitenPart 2 - Examination - Paper 2.6 (INT) Audit and InternalkhengmaiNoch keine Bewertungen

- Audit and Internal ReviewDokument7 SeitenAudit and Internal ReviewkhengmaiNoch keine Bewertungen

- Audit and Internal ReviewDokument6 SeitenAudit and Internal Reviewkhengmai100% (1)

- 2-6int 2002 Dec ADokument14 Seiten2-6int 2002 Dec AJay ChenNoch keine Bewertungen

- Part 2 Examination - Paper 2.6 (INT) Audit and Internal ReviewDokument12 SeitenPart 2 Examination - Paper 2.6 (INT) Audit and Internal ReviewkhengmaiNoch keine Bewertungen

- ACCA F8 Dec 2002 Exams Questions PDFDokument5 SeitenACCA F8 Dec 2002 Exams Questions PDFdhaneshwareeNoch keine Bewertungen

- Audit and Internal ReviewDokument6 SeitenAudit and Internal ReviewkhengmaiNoch keine Bewertungen

- 2008 Jun - Question Paper F8 Audit PDFDokument5 Seiten2008 Jun - Question Paper F8 Audit PDFCool RapperNoch keine Bewertungen

- Audit and Internal ReviewDokument6 SeitenAudit and Internal ReviewkhengmaiNoch keine Bewertungen

- 06 JUNE AnswersDokument13 Seiten06 JUNE AnswerskhengmaiNoch keine Bewertungen

- Part 2 Examination - Paper 2.6 (INT) Audit and Internal ReviewDokument12 SeitenPart 2 Examination - Paper 2.6 (INT) Audit and Internal ReviewkhengmaiNoch keine Bewertungen

- 05 DEC QuestionDokument10 Seiten05 DEC Questionkhengmai100% (1)

- 06 JUNE QuestionDokument11 Seiten06 JUNE QuestionkhengmaiNoch keine Bewertungen

- Financial Reporting: (International Stream)Dokument10 SeitenFinancial Reporting: (International Stream)ebukhory28Noch keine Bewertungen

- 05 JUNE AnswersDokument13 Seiten05 JUNE AnswerskhengmaiNoch keine Bewertungen

- 07 JUNE QuestionDokument11 Seiten07 JUNE Questionkhengmai67% (3)

- 07 JUNE AnswersDokument10 Seiten07 JUNE Answerskhengmai50% (2)

- 05 JUNE QuestionDokument10 Seiten05 JUNE Questionkhengmai100% (1)

- 05 DEC AnswersDokument15 Seiten05 DEC Answerskhengmai100% (5)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Technopreneurship Module 5: Customer Segment Activity 5: Frianeza, Zarah Joy C. BCSE-3-2Dokument2 SeitenTechnopreneurship Module 5: Customer Segment Activity 5: Frianeza, Zarah Joy C. BCSE-3-2Joy Frianeza75% (4)

- Business PlanDokument309 SeitenBusiness PlanAsma ShahidNoch keine Bewertungen

- Kickstarter - Launchboom Guide: Pre CampaignDokument2 SeitenKickstarter - Launchboom Guide: Pre CampaignStella NguyenNoch keine Bewertungen

- Factors Influencing Global Marketing Policy of ColgateDokument8 SeitenFactors Influencing Global Marketing Policy of Colgatesayam siddiquegmail.comNoch keine Bewertungen

- Planned ObsolescenceDokument23 SeitenPlanned ObsolescencealenNoch keine Bewertungen

- Ch. 1 Ch. 2 Aswath DamodaranDokument15 SeitenCh. 1 Ch. 2 Aswath Damodarandeeps0705Noch keine Bewertungen

- Project Gant Chart & Cost S-Curve-OriginalDokument2 SeitenProject Gant Chart & Cost S-Curve-OriginalMuhammad Anamul HoqueNoch keine Bewertungen

- Full Download Book Foundations of Business PDFDokument41 SeitenFull Download Book Foundations of Business PDFbeulah.howland471100% (13)

- Indonesia Daily: UpdateDokument7 SeitenIndonesia Daily: UpdateyolandaNoch keine Bewertungen

- Citibank Case Study Group1Dokument11 SeitenCitibank Case Study Group1Deepaksayu100% (1)

- Analytical Thinking and Decision MakingDokument16 SeitenAnalytical Thinking and Decision MakingJot Saini SainiNoch keine Bewertungen

- ACW 367 WK 5 Conceptual Framework ModifiedDokument18 SeitenACW 367 WK 5 Conceptual Framework ModifiedKameleswary GanesanNoch keine Bewertungen

- Contract of Agency: Submitted ToDokument3 SeitenContract of Agency: Submitted ToTamim RahmanNoch keine Bewertungen

- 06 08 Fathimas TextilesDokument424 Seiten06 08 Fathimas Textilesnadim ansariNoch keine Bewertungen

- A Project Report On: Social-Relevance To Study The Social Corporate Responsiblities Performed by The ICICI BankDokument73 SeitenA Project Report On: Social-Relevance To Study The Social Corporate Responsiblities Performed by The ICICI BankjyotiNoch keine Bewertungen

- T3 2004 - Dec - QDokument8 SeitenT3 2004 - Dec - QVinh Ngo NhuNoch keine Bewertungen

- 153-178 CH 04 Evans, J. Lindsay, W. Ed 8 (pp.153-178)Dokument28 Seiten153-178 CH 04 Evans, J. Lindsay, W. Ed 8 (pp.153-178)Markus KaufmannNoch keine Bewertungen

- Summary - Chap 5Dokument5 SeitenSummary - Chap 5Đăng Khoa Thạch TrầnNoch keine Bewertungen

- SR - Joinery Estimation Engineer/QS: Nidheesh.TDokument4 SeitenSR - Joinery Estimation Engineer/QS: Nidheesh.TTaseer BuchhNoch keine Bewertungen

- Shareholder Activism As A New Facet of Corporate Governance in IndiaDokument11 SeitenShareholder Activism As A New Facet of Corporate Governance in IndiaReeya PrakashNoch keine Bewertungen

- Caed102: Financial MarketsDokument2 SeitenCaed102: Financial MarketsXytusNoch keine Bewertungen

- Nashik Division 1Dokument2 SeitenNashik Division 1PATIL HIRAN JAJOO GSTNoch keine Bewertungen

- Cerda, Ciernelle R. Far 2 Module TypeDokument45 SeitenCerda, Ciernelle R. Far 2 Module TypeKaloy HoodNoch keine Bewertungen

- Far Problems With SolutionsDokument8 SeitenFar Problems With Solutionspatricia abbygail parbaNoch keine Bewertungen

- Counting Bars in Order To Detect End of CorrectionsDokument4 SeitenCounting Bars in Order To Detect End of Correctionsspaireg8977100% (1)

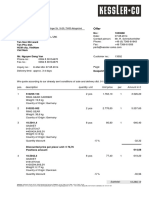

- Angebot 1033668 PDFDokument2 SeitenAngebot 1033668 PDFhoiNoch keine Bewertungen

- Flipkart Senior Business Analyst Analytics JDDokument3 SeitenFlipkart Senior Business Analyst Analytics JDVenkatesh Kumar VidelaNoch keine Bewertungen

- Dynamic Capabilities Theory SummaryDokument9 SeitenDynamic Capabilities Theory SummaryMatthewos HaileNoch keine Bewertungen

- Fernandez-Vega Eye InstituteDokument16 SeitenFernandez-Vega Eye InstituteFabricio Eric ParraNoch keine Bewertungen

- Service Quality Delivery and Its Impact On Customer Satisfaction in The Bank Services in Tanzania: The Case of Moshi Uchumi Commercial BankDokument90 SeitenService Quality Delivery and Its Impact On Customer Satisfaction in The Bank Services in Tanzania: The Case of Moshi Uchumi Commercial Bankkitderoger_391648570Noch keine Bewertungen