Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- MOS FY09 Financial Data PDFDokument9 SeitenMOS FY09 Financial Data PDFRafaelKwongNoch keine Bewertungen

- Competitor AnalysisDokument4 SeitenCompetitor AnalysisRafaelKwong100% (1)

- Case Study (Section 2.4)Dokument5 SeitenCase Study (Section 2.4)RafaelKwongNoch keine Bewertungen

- Cost Control and AnalysisDokument2 SeitenCost Control and AnalysisRafaelKwongNoch keine Bewertungen

- Management Accounting - Project 2Dokument3 SeitenManagement Accounting - Project 2RafaelKwongNoch keine Bewertungen

- Ma - Capital Expenditure AnalysisDokument3 SeitenMa - Capital Expenditure AnalysisRafaelKwongNoch keine Bewertungen

- Burger King-10K2009 PDFDokument128 SeitenBurger King-10K2009 PDFRafaelKwongNoch keine Bewertungen

- Pizza Hutt 2009annualreportDokument220 SeitenPizza Hutt 2009annualreportevojulzNoch keine Bewertungen

- Sales ForecastDokument2 SeitenSales ForecastRafaelKwongNoch keine Bewertungen

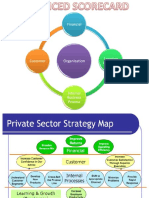

- Balanced Scorecard - Wells Fargo (BUSI0027D) PDFDokument12 SeitenBalanced Scorecard - Wells Fargo (BUSI0027D) PDFRafaelKwong50% (4)

- MADokument12 SeitenMARafaelKwongNoch keine Bewertungen

- Management Accounting - Project 1Dokument7 SeitenManagement Accounting - Project 1RafaelKwongNoch keine Bewertungen

- MA DisadvantageDokument1 SeiteMA DisadvantageRafaelKwongNoch keine Bewertungen

- MA Project 2 - McDonaldsDokument11 SeitenMA Project 2 - McDonaldsRafaelKwongNoch keine Bewertungen

- Inventory Management of McDonald'sDokument2 SeitenInventory Management of McDonald'sRafaelKwongNoch keine Bewertungen

- Advantages of Balanced ScorecardDokument1 SeiteAdvantages of Balanced ScorecardRafaelKwongNoch keine Bewertungen

- McDonald's Advertising and Pricing IIDokument2 SeitenMcDonald's Advertising and Pricing IIRafaelKwongNoch keine Bewertungen

- MA Presentation Slide Finalized - PPSXDokument33 SeitenMA Presentation Slide Finalized - PPSXRafaelKwongNoch keine Bewertungen

- Cash BudgetDokument1 SeiteCash BudgetRafaelKwongNoch keine Bewertungen

- McDonald's Industry, Competitor and Marketing AnalysisDokument20 SeitenMcDonald's Industry, Competitor and Marketing AnalysisRafaelKwongNoch keine Bewertungen

- IS PictureDokument1 SeiteIS PictureRafaelKwongNoch keine Bewertungen

- 1011 Group Project AssignmentDokument1 Seite1011 Group Project AssignmentRafaelKwongNoch keine Bewertungen

- Income Statement NeatDokument2 SeitenIncome Statement NeatRafaelKwongNoch keine Bewertungen

- Management Accounting - Project 2Dokument3 SeitenManagement Accounting - Project 2RafaelKwongNoch keine Bewertungen

- Chapter 16 LeadershipDokument18 SeitenChapter 16 LeadershipRafaelKwongNoch keine Bewertungen

- Budgeted Balance SheetDokument2 SeitenBudgeted Balance SheetRafaelKwongNoch keine Bewertungen

- Mini Interview Instruction SheetDokument2 SeitenMini Interview Instruction SheetRafaelKwongNoch keine Bewertungen

- Taxation Q21 Handout v3 PDFDokument11 SeitenTaxation Q21 Handout v3 PDFRafaelKwongNoch keine Bewertungen

- Answers For Question 2Dokument1 SeiteAnswers For Question 2RafaelKwongNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Role of Government in The Housing Market. The Eexperiences From AsiaDokument109 SeitenThe Role of Government in The Housing Market. The Eexperiences From AsiaPUSTAKA Virtual Tata Ruang dan Pertanahan (Pusvir TRP)Noch keine Bewertungen

- Macro and Micro AnalysisDokument20 SeitenMacro and Micro AnalysisRiya Pandey100% (1)

- Navi Mumbai MidcDokument132 SeitenNavi Mumbai MidcKedar Parab67% (15)

- Economics ProjectDokument15 SeitenEconomics ProjectAniket taywadeNoch keine Bewertungen

- Eco Handout Analyzes India's Demonetization and Black Money PoliciesDokument15 SeitenEco Handout Analyzes India's Demonetization and Black Money Policiessonali mishraNoch keine Bewertungen

- Tax InvoiceDokument1 SeiteTax Invoicepiyush1809Noch keine Bewertungen

- Encyclopedia of American BusinessDokument863 SeitenEncyclopedia of American Businessshark_freire5046Noch keine Bewertungen

- Dokumen - Tips Unclaimed DividendsDokument107 SeitenDokumen - Tips Unclaimed DividendsVM ONoch keine Bewertungen

- Chapter 1-Introduction To Green BuildingsDokument40 SeitenChapter 1-Introduction To Green Buildingsniti860Noch keine Bewertungen

- Aisa Business Kaha Hindi-1 PDFDokument20 SeitenAisa Business Kaha Hindi-1 PDFAnonymous 2rX2W07100% (1)

- Sample Project AbstractDokument2 SeitenSample Project AbstractJyotiprakash sahuNoch keine Bewertungen

- "Potential of Life Insurance Industry in Surat Market": Under The Guidance ofDokument51 Seiten"Potential of Life Insurance Industry in Surat Market": Under The Guidance ofFreddy Savio D'souzaNoch keine Bewertungen

- Rajanpur Salary Sheet June 2020Dokument18.379 SeitenRajanpur Salary Sheet June 2020Zahid HussainNoch keine Bewertungen

- Tao Wang - World Bank Experience On Carbon Finance Operations in BiogasDokument20 SeitenTao Wang - World Bank Experience On Carbon Finance Operations in BiogasEnergy for AllNoch keine Bewertungen

- Costing and Control of LabourDokument43 SeitenCosting and Control of Labourrohit vermaNoch keine Bewertungen

- Oil Industry of Kazakhstan: Name: LIU XU Class: Tuesday ID No.: 014201900253Dokument2 SeitenOil Industry of Kazakhstan: Name: LIU XU Class: Tuesday ID No.: 014201900253cey liuNoch keine Bewertungen

- Questionnaire Fast FoodDokument6 SeitenQuestionnaire Fast FoodAsh AsvinNoch keine Bewertungen

- ISLAMIYA ENGLISH SCHOOL MONEY CHAPTER EXERCISESDokument1 SeiteISLAMIYA ENGLISH SCHOOL MONEY CHAPTER EXERCISESeverly.Noch keine Bewertungen

- CH North&south PDFDokument24 SeitenCH North&south PDFNelson Vinod KumarNoch keine Bewertungen

- Partnership Formation Answer KeyDokument8 SeitenPartnership Formation Answer KeyNichole Joy XielSera TanNoch keine Bewertungen

- JVA JuryDokument22 SeitenJVA JuryYogesh SharmaNoch keine Bewertungen

- IIP - Vs - PMI, DifferencesDokument5 SeitenIIP - Vs - PMI, DifferencesChetan GuptaNoch keine Bewertungen

- TransportPlanning&Engineering PDFDokument121 SeitenTransportPlanning&Engineering PDFItishree RanaNoch keine Bewertungen

- DaewooDokument18 SeitenDaewooapoorva498Noch keine Bewertungen

- India Inc's Baby Steps On Long Road To Normalcy: HE Conomic ImesDokument12 SeitenIndia Inc's Baby Steps On Long Road To Normalcy: HE Conomic ImesShobhashree PandaNoch keine Bewertungen

- Study of Supply Chain at Big BasketDokument10 SeitenStudy of Supply Chain at Big BasketPratul Batra100% (1)

- Tax Invoice: Tommy Hilfiger Slim Men Blue JeansDokument1 SeiteTax Invoice: Tommy Hilfiger Slim Men Blue JeansSusil Kumar MisraNoch keine Bewertungen

- Faith in Wooden Toys: A Glimpse into Selecta SpielzeugDokument2 SeitenFaith in Wooden Toys: A Glimpse into Selecta SpielzeugAvishekNoch keine Bewertungen

- MCQs On Transfer of Property ActDokument46 SeitenMCQs On Transfer of Property ActRam Iyer75% (4)

- Practice Problems For Mid TermDokument6 SeitenPractice Problems For Mid TermMohit ChawlaNoch keine Bewertungen