Das könnte Ihnen auch gefallen

- IPCE May 2013 Taxation Suggested AnswerDokument13 SeitenIPCE May 2013 Taxation Suggested AnswerParasuram IyerNoch keine Bewertungen

- Direct Tax SLE-2 Roll No KSPMCAA012 Dev ShahDokument5 SeitenDirect Tax SLE-2 Roll No KSPMCAA012 Dev ShahDev ShahNoch keine Bewertungen

- IPCC Taxation Guideline Answer Nov 2015 ExamDokument16 SeitenIPCC Taxation Guideline Answer Nov 2015 ExamSushant SaxenaNoch keine Bewertungen

- Discussions Updated 24.03Dokument28 SeitenDiscussions Updated 24.03rajawatswadheentaNoch keine Bewertungen

- Examples Salary 2015Dokument44 SeitenExamples Salary 2015Farhan JanNoch keine Bewertungen

- Tax Melville AnswersDokument58 SeitenTax Melville AnswersAmrita Dhasmana25% (4)

- Principles of Taxation For Business and Investment Planning 2016 19Th Edition Jones Solutions Manual Full Chapter PDFDokument21 SeitenPrinciples of Taxation For Business and Investment Planning 2016 19Th Edition Jones Solutions Manual Full Chapter PDFrosyseedorff100% (7)

- Advanced Taxation and Strategic Tax Planning PDFDokument11 SeitenAdvanced Taxation and Strategic Tax Planning PDFAnuk PereraNoch keine Bewertungen

- SalaryDokument66 SeitenSalaryFurqan AhmedNoch keine Bewertungen

- Mock E Exam Pap ERDokument19 SeitenMock E Exam Pap ERtim_rattanaNoch keine Bewertungen

- Application Level Corporate Laws Practices Nov Dec 2013Dokument3 SeitenApplication Level Corporate Laws Practices Nov Dec 2013Timothy GillespieNoch keine Bewertungen

- Chap03 Sol OddDokument19 SeitenChap03 Sol OddRussell WilsonNoch keine Bewertungen

- Employment Income TaxDokument5 SeitenEmployment Income TaxYehualashet MekonninNoch keine Bewertungen

- Taxation Review Dec2017Dokument7 SeitenTaxation Review Dec2017Shaiful Alam FCANoch keine Bewertungen

- Public Chapter 4Dokument19 SeitenPublic Chapter 4samuel debebeNoch keine Bewertungen

- Dawit Taxation AssignmentDokument3 SeitenDawit Taxation Assignmentthedalesh weldeNoch keine Bewertungen

- Taxation 2013 NovDokument25 SeitenTaxation 2013 NovAshok 'Maelk' RajpurohitNoch keine Bewertungen

- Taxation concepts and calculationsDokument34 SeitenTaxation concepts and calculationsMeet GargNoch keine Bewertungen

- F9 - IPRO - Mock 1 - AnswersDokument12 SeitenF9 - IPRO - Mock 1 - AnswersOlivier MNoch keine Bewertungen

- Chapter 6Dokument13 SeitenChapter 6vitbau98100% (1)

- Fabm2 Q2 W4 5Dokument8 SeitenFabm2 Q2 W4 5maeesotoNoch keine Bewertungen

- Salary PDFDokument83 SeitenSalary PDFGaurav BeniwalNoch keine Bewertungen

- On capital structure, dividend policy and bankruptcy costsDokument3 SeitenOn capital structure, dividend policy and bankruptcy costsAdi AliNoch keine Bewertungen

- Taxation Answers 2Dokument9 SeitenTaxation Answers 2Kiều Thảo AnhNoch keine Bewertungen

- Tax SolutionDokument9 SeitenTax SolutionGhulam Mohyudin KharalNoch keine Bewertungen

- Identify and Discuss Direct TaxDokument7 SeitenIdentify and Discuss Direct Taxsamuel asefaNoch keine Bewertungen

- Acct 557Dokument5 SeitenAcct 557kihumbae100% (4)

- Diploma in Cambodia Tax Pilot Exam AnswersDokument13 SeitenDiploma in Cambodia Tax Pilot Exam AnswersVannak2015Noch keine Bewertungen

- Chapter 6: Accounting For Income Tax: Review QuestionsDokument10 SeitenChapter 6: Accounting For Income Tax: Review QuestionsShek Kwun HeiNoch keine Bewertungen

- Income From Interest On SecuritiesDokument4 SeitenIncome From Interest On SecuritiesSohidul IslamNoch keine Bewertungen

- Fifth PartDokument17 SeitenFifth PartMahsinur RahmanNoch keine Bewertungen

- ENGR 301 - Assign4solnDokument5 SeitenENGR 301 - Assign4solnAP100% (1)

- MAC CEO Tax CalculationDokument4 SeitenMAC CEO Tax CalculationhafsaNoch keine Bewertungen

- FA II - Chapter 2 & 3 Part IIDokument21 SeitenFA II - Chapter 2 & 3 Part IISitra AbduNoch keine Bewertungen

- Chapter 11 Advance Accounting SolmanDokument12 SeitenChapter 11 Advance Accounting SolmanShiela GumamelaNoch keine Bewertungen

- PDF Document E64dfec87bb0 1Dokument75 SeitenPDF Document E64dfec87bb0 120BRM051 Sukant SNoch keine Bewertungen

- Chapter 5 - 14thDokument18 SeitenChapter 5 - 14thLNoch keine Bewertungen

- DocumentDokument3 SeitenDocumentMaria Kathreena Andrea AdevaNoch keine Bewertungen

- CB Lecture 1Dokument20 SeitenCB Lecture 1Tshepang MatebesiNoch keine Bewertungen

- Mock Exam Paper: Time AllowedDokument9 SeitenMock Exam Paper: Time AllowedVannak2015Noch keine Bewertungen

- ATax - 03Dokument29 SeitenATax - 03Haseeb Ahmed ShaikhNoch keine Bewertungen

- Suggested Tax Paper May 2011Dokument11 SeitenSuggested Tax Paper May 2011Sudhir PanigrahiNoch keine Bewertungen

- AbelDokument12 SeitenAbelErmi ManNoch keine Bewertungen

- Chapter 4 PDFDokument14 SeitenChapter 4 PDFJay BrockNoch keine Bewertungen

- Taxation Law CIA 3Dokument3 SeitenTaxation Law CIA 3Deepa GowdaNoch keine Bewertungen

- Corporations: Introduction to Operating RulesDokument4 SeitenCorporations: Introduction to Operating RulesSheena CarrouthersNoch keine Bewertungen

- MT Test Review-Taxation 1-Win 2024Dokument4 SeitenMT Test Review-Taxation 1-Win 2024Mariola AlkuNoch keine Bewertungen

- 2019 PROBLEM EXERCISES IN INCOME TAXATION and TRAIN LAW (B)Dokument11 Seiten2019 PROBLEM EXERCISES IN INCOME TAXATION and TRAIN LAW (B)MGVMonNoch keine Bewertungen

- Additions To TaxDokument22 SeitenAdditions To Taxstannis69420Noch keine Bewertungen

- Taxation of Employment IncomeDokument7 SeitenTaxation of Employment IncomeJamvy Jose FernandezNoch keine Bewertungen

- Federal Income Taxation Chapter 6 Solutions (Other Itemized Deductions)Dokument14 SeitenFederal Income Taxation Chapter 6 Solutions (Other Itemized Deductions)JW67% (3)

- F1 November 2010 AnswersDokument11 SeitenF1 November 2010 AnswersmavkaziNoch keine Bewertungen

- Accounting Seminar 16 - Team 6 Part I & IIDokument64 SeitenAccounting Seminar 16 - Team 6 Part I & IIJerilynn YeoNoch keine Bewertungen

- Accounting For Financial ManagementDokument42 SeitenAccounting For Financial ManagementTIDURLANoch keine Bewertungen

- 1 .Income Tax On Salaries - (01.06.2015)Dokument57 Seiten1 .Income Tax On Salaries - (01.06.2015)yvNoch keine Bewertungen

- Fast-Track Tax Reform: Lessons from the MaldivesVon EverandFast-Track Tax Reform: Lessons from the MaldivesNoch keine Bewertungen

- Income Tax Law for Start-Up Businesses: An Overview of Business Entities and Income Tax LawVon EverandIncome Tax Law for Start-Up Businesses: An Overview of Business Entities and Income Tax LawBewertung: 3.5 von 5 Sternen3.5/5 (4)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineVon EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNoch keine Bewertungen

- J.K. Lasser's 1001 Deductions and Tax Breaks 2024: Your Complete Guide to Everything DeductibleVon EverandJ.K. Lasser's 1001 Deductions and Tax Breaks 2024: Your Complete Guide to Everything DeductibleNoch keine Bewertungen

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsVon Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsNoch keine Bewertungen

- MOS FY09 Financial Data PDFDokument9 SeitenMOS FY09 Financial Data PDFRafaelKwongNoch keine Bewertungen

- Pizza Hutt 2009annualreportDokument220 SeitenPizza Hutt 2009annualreportevojulzNoch keine Bewertungen

- Ma - Capital Expenditure AnalysisDokument3 SeitenMa - Capital Expenditure AnalysisRafaelKwongNoch keine Bewertungen

- Management Accounting - Project 1Dokument7 SeitenManagement Accounting - Project 1RafaelKwongNoch keine Bewertungen

- MADokument12 SeitenMARafaelKwongNoch keine Bewertungen

- Case Study (Section 2.4)Dokument5 SeitenCase Study (Section 2.4)RafaelKwongNoch keine Bewertungen

- Burger King-10K2009 PDFDokument128 SeitenBurger King-10K2009 PDFRafaelKwongNoch keine Bewertungen

- Cost Control and AnalysisDokument2 SeitenCost Control and AnalysisRafaelKwongNoch keine Bewertungen

- Sales ForecastDokument2 SeitenSales ForecastRafaelKwongNoch keine Bewertungen

- Management Accounting - Project 2Dokument3 SeitenManagement Accounting - Project 2RafaelKwongNoch keine Bewertungen

- McDonald's Advertising and Pricing IIDokument2 SeitenMcDonald's Advertising and Pricing IIRafaelKwongNoch keine Bewertungen

- Competitor AnalysisDokument4 SeitenCompetitor AnalysisRafaelKwong100% (1)

- MA DisadvantageDokument1 SeiteMA DisadvantageRafaelKwongNoch keine Bewertungen

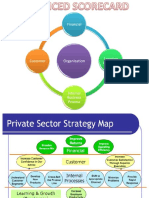

- Balanced Scorecard - Wells Fargo (BUSI0027D) PDFDokument12 SeitenBalanced Scorecard - Wells Fargo (BUSI0027D) PDFRafaelKwong50% (4)

- MA Project 2 - McDonaldsDokument11 SeitenMA Project 2 - McDonaldsRafaelKwongNoch keine Bewertungen

- MA Presentation Slide Finalized - PPSXDokument33 SeitenMA Presentation Slide Finalized - PPSXRafaelKwongNoch keine Bewertungen

- Inventory Management of McDonald'sDokument2 SeitenInventory Management of McDonald'sRafaelKwongNoch keine Bewertungen

- Advantages of Balanced ScorecardDokument1 SeiteAdvantages of Balanced ScorecardRafaelKwongNoch keine Bewertungen

- Budgeted Balance SheetDokument2 SeitenBudgeted Balance SheetRafaelKwongNoch keine Bewertungen

- Income Statement NeatDokument2 SeitenIncome Statement NeatRafaelKwongNoch keine Bewertungen

- Cash BudgetDokument1 SeiteCash BudgetRafaelKwongNoch keine Bewertungen

- McDonald's Industry, Competitor and Marketing AnalysisDokument20 SeitenMcDonald's Industry, Competitor and Marketing AnalysisRafaelKwongNoch keine Bewertungen

- IS PictureDokument1 SeiteIS PictureRafaelKwongNoch keine Bewertungen

- Taxation Q21 Handout v3 PDFDokument11 SeitenTaxation Q21 Handout v3 PDFRafaelKwongNoch keine Bewertungen

- 1011 Group Project AssignmentDokument1 Seite1011 Group Project AssignmentRafaelKwongNoch keine Bewertungen

- Management Accounting - Project 2Dokument3 SeitenManagement Accounting - Project 2RafaelKwongNoch keine Bewertungen

- Mini Interview Instruction SheetDokument2 SeitenMini Interview Instruction SheetRafaelKwongNoch keine Bewertungen

- Chapter 16 LeadershipDokument18 SeitenChapter 16 LeadershipRafaelKwongNoch keine Bewertungen

- Answers For Question 2Dokument1 SeiteAnswers For Question 2RafaelKwongNoch keine Bewertungen

- 1B Insurance Vs Spouses GregorioDokument3 Seiten1B Insurance Vs Spouses GregorioJessa LoNoch keine Bewertungen

- Certainty of ObjectDokument18 SeitenCertainty of ObjectNadrah RasidiNoch keine Bewertungen

- Persons and Family Law NotesDokument10 SeitenPersons and Family Law NotesMaria Dana BrillantesNoch keine Bewertungen

- House GOP Letter To Jake SullivanDokument2 SeitenHouse GOP Letter To Jake SullivanFox NewsNoch keine Bewertungen

- 9 The Aims of Punishment and Principles of SentencingDokument14 Seiten9 The Aims of Punishment and Principles of Sentencingiskandar027Noch keine Bewertungen

- Supreme Court Rules in Favor of Daughters' Equal Rights to Coparcenary PropertyDokument3 SeitenSupreme Court Rules in Favor of Daughters' Equal Rights to Coparcenary Propertyayush kumarNoch keine Bewertungen

- Dizon-Rivera vs. DizonDokument2 SeitenDizon-Rivera vs. Dizonmmabbun001Noch keine Bewertungen

- Heirs of Racaza v. Sps Abay-AbayDokument2 SeitenHeirs of Racaza v. Sps Abay-AbayRostum AgapitoNoch keine Bewertungen

- 05 Mitsubishi Motors Phils. Corp. v. Bureau of CustomsDokument3 Seiten05 Mitsubishi Motors Phils. Corp. v. Bureau of CustomsMunchie MichieNoch keine Bewertungen

- Cases in Tax ReviewDokument173 SeitenCases in Tax ReviewErmawooNoch keine Bewertungen

- Search For Outstanding Government Workers: HAP Form 1Dokument4 SeitenSearch For Outstanding Government Workers: HAP Form 1gbenjielizonNoch keine Bewertungen

- Income Tax Ruling Explains Salary and WagesDokument11 SeitenIncome Tax Ruling Explains Salary and WagesAbedNoch keine Bewertungen

- PLJ Volume 85 Issue 1 2 The Supreme Court and International Law Problems and Approaches in Philippine Practice Merlin M. MagallonaDokument101 SeitenPLJ Volume 85 Issue 1 2 The Supreme Court and International Law Problems and Approaches in Philippine Practice Merlin M. MagallonaNicole Stephanie WeeNoch keine Bewertungen

- In The United States District Court For The District of ArizonaDokument3 SeitenIn The United States District Court For The District of ArizonaDoctor Conspiracy100% (1)

- Central Industrial Security Force: Citizen'S CharterDokument44 SeitenCentral Industrial Security Force: Citizen'S Charterashay singhNoch keine Bewertungen

- Agreement of Authorisation and Cession of Payment: S The CEDENT)Dokument3 SeitenAgreement of Authorisation and Cession of Payment: S The CEDENT)takuva03100% (2)

- 11 de Los Reyes V AlojadoDokument1 Seite11 de Los Reyes V AlojadoAngelo NavarroNoch keine Bewertungen

- Thayer Background Brief U.S. FONOPS, Vietnam and The South China SeaDokument2 SeitenThayer Background Brief U.S. FONOPS, Vietnam and The South China SeaCarlyle Alan ThayerNoch keine Bewertungen

- KWASEKO CBO ConstitutionDokument7 SeitenKWASEKO CBO ConstitutionSharon Amondi50% (2)

- Montano V Verceles Case DigestDokument5 SeitenMontano V Verceles Case DigestRho Hanee XaNoch keine Bewertungen

- Raghu Nayjas PDFDokument2 SeitenRaghu Nayjas PDFManish R ShankarNoch keine Bewertungen

- Supreme Court Review Judgment on Taj Heritage Corruption CaseDokument22 SeitenSupreme Court Review Judgment on Taj Heritage Corruption CaseBhupendra CharanNoch keine Bewertungen

- Diao Vs MartinezDokument3 SeitenDiao Vs MartinezM Azeneth JJNoch keine Bewertungen

- Civil Mock Trial: I S C B CDokument23 SeitenCivil Mock Trial: I S C B CEugene Evan Endaya Uy100% (1)

- THEORIESDokument15 SeitenTHEORIES123Noch keine Bewertungen

- Petition For NaturalizationDokument4 SeitenPetition For NaturalizationbertspamintuanNoch keine Bewertungen

- SPECIAL POWER O-WPS OfficeDokument4 SeitenSPECIAL POWER O-WPS OfficeKaori SakiNoch keine Bewertungen

- Current Affairs Study PDF Capsule - February 2017 by AffairsCloudDokument167 SeitenCurrent Affairs Study PDF Capsule - February 2017 by AffairsCloudsdfdNoch keine Bewertungen

- Revisiting ISLAW by Atty. HulingangaDokument6 SeitenRevisiting ISLAW by Atty. HulingangaRommel Brian FloresNoch keine Bewertungen

- PBB vs. CHUADokument3 SeitenPBB vs. CHUAVeronica ChanNoch keine Bewertungen