Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- TNG JSC Consultancy Services Agreement FINAL - To SendDokument16 SeitenTNG JSC Consultancy Services Agreement FINAL - To SendAn PeannieNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Virata vs. Ng Wee (2017) Ruling on Real Party in Interest and Cause of ActionDokument12 SeitenVirata vs. Ng Wee (2017) Ruling on Real Party in Interest and Cause of ActionElay CalinaoNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Cybercrime - Capuz-SorianoDokument4 SeitenCybercrime - Capuz-SorianosorianoleinelyngraceNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- US v. Kudryn IndictmentDokument6 SeitenUS v. Kudryn IndictmentJustin OkunNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Standard Request For Proposal For Adm Building 12Dokument39 SeitenStandard Request For Proposal For Adm Building 12Bidur KhadkaNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- 10 BOC vs. DevanaderaDokument3 Seiten10 BOC vs. Devanaderaaspiringlawyer1234Noch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Belita vs. Sy G.R. No. 191087 June 2016Dokument14 SeitenBelita vs. Sy G.R. No. 191087 June 2016Kesca GutierrezNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Becg m-4Dokument25 SeitenBecg m-4CH ANIL VARMANoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Forensic Accounting andDokument16 SeitenForensic Accounting andNsr100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

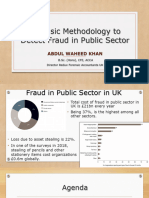

- CTFAIA Hari Ke 5 Materi 2 - Waheed KhanDokument31 SeitenCTFAIA Hari Ke 5 Materi 2 - Waheed Khanoyonglisa12Noch keine Bewertungen

- Accounting Exam 2 Study GuideDokument1 SeiteAccounting Exam 2 Study GuideIvan LauNoch keine Bewertungen

- A Quo: G.R. No. 162822 August 25, 2005 JAIME GUINHAWA, Petitioners, People of The Philippines, RespondentDokument11 SeitenA Quo: G.R. No. 162822 August 25, 2005 JAIME GUINHAWA, Petitioners, People of The Philippines, RespondentDonna SabellanoNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- United States v. Eugene D. Gatewood, 733 F.2d 1390, 10th Cir. (1984)Dokument7 SeitenUnited States v. Eugene D. Gatewood, 733 F.2d 1390, 10th Cir. (1984)Scribd Government DocsNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- ONG CHUA v. CARRDokument2 SeitenONG CHUA v. CARRJames Erwin VelascoNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Reopening of Partition: Submitted By-Soumil Goyal Submitted To - Roll No - 97/13Dokument13 SeitenReopening of Partition: Submitted By-Soumil Goyal Submitted To - Roll No - 97/13soumilNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- LA County Minimum Fees ListDokument92 SeitenLA County Minimum Fees ListSGVNewsNoch keine Bewertungen

- RAJIV GANDHI UNIVERSITY'S STUDY ON CYBER CRIME LAWDokument23 SeitenRAJIV GANDHI UNIVERSITY'S STUDY ON CYBER CRIME LAWshivanika singlaNoch keine Bewertungen

- Siguan vs. LimDokument2 SeitenSiguan vs. LimDongkae100% (1)

- Chief Operating Officer CCO in Charlotte NC Resume Ram ManchiDokument2 SeitenChief Operating Officer CCO in Charlotte NC Resume Ram ManchiRam ManchiNoch keine Bewertungen

- Cyber Security Unit 1Dokument9 SeitenCyber Security Unit 1Seema PatilNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- About This Application For Accident BenefitsDokument8 SeitenAbout This Application For Accident BenefitsdesigniumNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- BRC Global Standard For Packaging and Packaging MaterialsDokument5 SeitenBRC Global Standard For Packaging and Packaging MaterialsCassilda CarvalhoNoch keine Bewertungen

- Case of JACINTO TANGUILIG Doing Business Under The Name and Style JDokument12 SeitenCase of JACINTO TANGUILIG Doing Business Under The Name and Style JChris Javier100% (1)

- Audit 2 Marks QuestionsDokument4 SeitenAudit 2 Marks QuestionsEric MartinezNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Gathering Evidences and Forms of Evidence1Dokument12 SeitenGathering Evidences and Forms of Evidence1gokul ramananNoch keine Bewertungen

- United States v. Karen M. McGauley, 279 F.3d 62, 1st Cir. (2002)Dokument18 SeitenUnited States v. Karen M. McGauley, 279 F.3d 62, 1st Cir. (2002)Scribd Government DocsNoch keine Bewertungen

- University of Strathclyde Card ID Theft: Trends in Smartcard Fraud ScamDokument2 SeitenUniversity of Strathclyde Card ID Theft: Trends in Smartcard Fraud ScamdavidganiNoch keine Bewertungen

- SCRA Lee vs. PeopleDokument31 SeitenSCRA Lee vs. Peoplerols villanezaNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Taiwan Kolin Corporation, Ltd. vs. Kolin Electronics Co., Inc.Dokument2 SeitenTaiwan Kolin Corporation, Ltd. vs. Kolin Electronics Co., Inc.Maricar Corina Canaya0% (2)

- Bank Secrecy Law ExceptionsDokument15 SeitenBank Secrecy Law ExceptionsCristelle Elaine ColleraNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)