Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Consumer Durable LoansDokument10 SeitenConsumer Durable LoansdevrajkinjalNoch keine Bewertungen

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Bayo DetaDokument2 SeitenBayo DetadevrajkinjalNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- 43 Overview of Ind As 1201Dokument97 Seiten43 Overview of Ind As 1201padmanabha14Noch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- "Marketing Department of Dudhsagar Dairy": A Winter Project OnDokument1 Seite"Marketing Department of Dudhsagar Dairy": A Winter Project OndevrajkinjalNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- CCD INDEXDokument5 SeitenCCD INDEXdevrajkinjalNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Cost of Projectannexure DataDokument4 SeitenCost of Projectannexure DatadevrajkinjalNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- 14.1 Relative Industry Attractiveness Weighting Rating (1-10) Industry AttractivenessDokument3 Seiten14.1 Relative Industry Attractiveness Weighting Rating (1-10) Industry AttractivenessdevrajkinjalNoch keine Bewertungen

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- 3.1 Project Concept: S.V. Institute of Management, Kadi. S.V. Institute of Management, KadiDokument2 Seiten3.1 Project Concept: S.V. Institute of Management, Kadi. S.V. Institute of Management, KadidevrajkinjalNoch keine Bewertungen

- Chap 13 NBFC (CP)Dokument2 SeitenChap 13 NBFC (CP)devrajkinjalNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Power Finance CorpDokument10 SeitenPower Finance CorpdevrajkinjalNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Key Success Factors of Nbfcs NBFCS: 1. Technology UtilizationDokument3 SeitenKey Success Factors of Nbfcs NBFCS: 1. Technology UtilizationdevrajkinjalNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Research Methodology: 2.1 Objectives of The StudyDokument2 SeitenResearch Methodology: 2.1 Objectives of The StudydevrajkinjalNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Chap 14 NBFC (CP)Dokument2 SeitenChap 14 NBFC (CP)devrajkinjalNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Chap 6 NBFC (CP)Dokument2 SeitenChap 6 NBFC (CP)devrajkinjalNoch keine Bewertungen

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Distribution Channel in The NBFC Industry NBFCDokument2 SeitenDistribution Channel in The NBFC Industry NBFCdevrajkinjalNoch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- INDIAN MirrorDokument14 SeitenINDIAN MirrordevrajkinjalNoch keine Bewertungen

- Pradhan Mantri MUDRA YojanaDokument3 SeitenPradhan Mantri MUDRA YojanaKiran JadhavNoch keine Bewertungen

- DHFL Meltdown: The Corporate Governance Lapses: Daitri Tiwary and Arunaditya SahayDokument14 SeitenDHFL Meltdown: The Corporate Governance Lapses: Daitri Tiwary and Arunaditya SahayGaurav GuptaNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Central BankDokument35 SeitenCentral BankanujNoch keine Bewertungen

- FMI Unit 1Dokument30 SeitenFMI Unit 1Debajit DasNoch keine Bewertungen

- Non Performing Assets - Challenges To Public Sector Bank-1Dokument96 SeitenNon Performing Assets - Challenges To Public Sector Bank-1nimittpathak1989Noch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Finance FunctionDokument25 SeitenFinance FunctionKane0% (1)

- 12 Chapter 9 - Risk Management in Banks NBFCsDokument4 Seiten12 Chapter 9 - Risk Management in Banks NBFCsgarima_kukreja_dceNoch keine Bewertungen

- Economy Current Affairs by Teju, Nextgen Ias - November 2020Dokument50 SeitenEconomy Current Affairs by Teju, Nextgen Ias - November 2020akshaygmailNoch keine Bewertungen

- A Project Report On Loan Procedure of Consumer Durable Product at Bajaj Finserv LendingDokument65 SeitenA Project Report On Loan Procedure of Consumer Durable Product at Bajaj Finserv LendingHusna Majid50% (2)

- First Draft of The Project ReportDokument9 SeitenFirst Draft of The Project ReportHunny VermaNoch keine Bewertungen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Archana Khetan SFM OldDokument53 SeitenArchana Khetan SFM OldSakshi VermaNoch keine Bewertungen

- HDFC MergerDokument18 SeitenHDFC MergerRishabh RakeshNoch keine Bewertungen

- Business Finance: Mr. Dave Kieth J. Lappay Subject TeacherDokument26 SeitenBusiness Finance: Mr. Dave Kieth J. Lappay Subject TeacherNathaniel BocautoNoch keine Bewertungen

- Bajaj Finance Limited: BY: Nagarjuna Reddy PGDM-FINANCE, IBA BangaloreDokument12 SeitenBajaj Finance Limited: BY: Nagarjuna Reddy PGDM-FINANCE, IBA BangaloreNagarjuna ReddyNoch keine Bewertungen

- Manappuram Finance - A Gold DerivativeDokument2 SeitenManappuram Finance - A Gold DerivativeRaghu.GNoch keine Bewertungen

- ICICI Vehical LoanDokument49 SeitenICICI Vehical Loanjagdish80% (5)

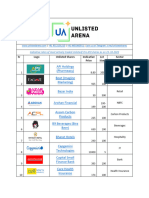

- Unlisted Arena Price List 23-10-2023Dokument5 SeitenUnlisted Arena Price List 23-10-2023shammore97Noch keine Bewertungen

- Ksfe Organisation StudyDokument74 SeitenKsfe Organisation Studyrajagopal100% (1)

- Financial System in PakistanDokument13 SeitenFinancial System in PakistanMuhammad IrfanNoch keine Bewertungen

- Order in The Matter of GBC Enterprise LimitedDokument24 SeitenOrder in The Matter of GBC Enterprise LimitedShyam SunderNoch keine Bewertungen

- NBFC MeaningDokument48 SeitenNBFC MeaningMurali Krishna VelavetiNoch keine Bewertungen

- Indian Financial System - An Overview - Mahesh ParikhDokument33 SeitenIndian Financial System - An Overview - Mahesh ParikhJe RomeNoch keine Bewertungen

- Functions of National Saving OrganizationDokument42 SeitenFunctions of National Saving OrganizationDebbie Jacobson62% (29)

- FFDokument106 SeitenFFSRIJITNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Final EBCL NovemberDokument686 SeitenFinal EBCL Novemberelliot fernandesNoch keine Bewertungen

- NBFC CLTDokument15 SeitenNBFC CLTArmaanNoch keine Bewertungen

- Bfsi - Icici Direct (Su - Oct 2020)Dokument14 SeitenBfsi - Icici Direct (Su - Oct 2020)Debjit AdakNoch keine Bewertungen

- Chapter - 8 Micro Finance Institutions: Introductio NDokument5 SeitenChapter - 8 Micro Finance Institutions: Introductio Netc123456789Noch keine Bewertungen

- .III Syllaubs PDFDokument22 Seiten.III Syllaubs PDFSamNoch keine Bewertungen

- Investment Law MarketingDokument6 SeitenInvestment Law MarketingJust RandomNoch keine Bewertungen

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsVon EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNoch keine Bewertungen

- Basic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonVon EverandBasic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonBewertung: 5 von 5 Sternen5/5 (9)