Das könnte Ihnen auch gefallen

- Solution Manual For Designing and Managing The Supply Chain 3rd Edition by David Simchi LeviDokument5 SeitenSolution Manual For Designing and Managing The Supply Chain 3rd Edition by David Simchi LeviRamswaroop Khichar100% (1)

- Fundamentals of Corporate Finance 8th Edition by Brealey Myers Marcus ISBN Solution ManualDokument6 SeitenFundamentals of Corporate Finance 8th Edition by Brealey Myers Marcus ISBN Solution Manualmary100% (24)

- Answers To Chapter 4 Exercises: Review and Practice ExercisesDokument10 SeitenAnswers To Chapter 4 Exercises: Review and Practice ExercisesHuyen NguyenNoch keine Bewertungen

- ECON 210 Homework 2Dokument3 SeitenECON 210 Homework 2Nas DNoch keine Bewertungen

- Limits To Growth ModelDokument12 SeitenLimits To Growth ModelKarpagam MahadevanNoch keine Bewertungen

- Receipt PDFDokument2 SeitenReceipt PDFObi ToNoch keine Bewertungen

- 12th Economics Question Paper For Public Exam 2022 PDF Download 1Dokument12 Seiten12th Economics Question Paper For Public Exam 2022 PDF Download 1karthikvijayan207Noch keine Bewertungen

- Price Determination Under Perfect CompetitionDokument19 SeitenPrice Determination Under Perfect CompetitionRajeshsharmapurangNoch keine Bewertungen

- 103 EADB Chapter-2: Dr. Rakesh BhatiDokument85 Seiten103 EADB Chapter-2: Dr. Rakesh BhatiDr. Rakesh BhatiNoch keine Bewertungen

- Parkin Elasticity Ch04Dokument20 SeitenParkin Elasticity Ch04AnnaNoch keine Bewertungen

- The Role of Time Element in The DeterminationDokument9 SeitenThe Role of Time Element in The DeterminationniranjanaNoch keine Bewertungen

- Fin Management - m4Dokument19 SeitenFin Management - m4Ma. Elene MagdaraogNoch keine Bewertungen

- Lecture Test 2021 t2w8 Year 5 Essay Test - Examiners' ReportDokument9 SeitenLecture Test 2021 t2w8 Year 5 Essay Test - Examiners' ReportXIAOQI WANGNoch keine Bewertungen

- Time Elements Used in The Theory of Price Determination!Dokument2 SeitenTime Elements Used in The Theory of Price Determination!Anonymous TUQNFWAPW5Noch keine Bewertungen

- B.A Part 1 EconomicsDokument11 SeitenB.A Part 1 EconomicsSona SinghNoch keine Bewertungen

- 5 KLMDokument2 Seiten5 KLMAizel KateNoch keine Bewertungen

- Pricing Under Perfect CompetitionDokument12 SeitenPricing Under Perfect Competitionchameli sNoch keine Bewertungen

- SupplyDokument18 SeitenSupplyShubham KumarNoch keine Bewertungen

- Instructor Manual For Designing and Managing The Supply Chain 3e by David Simchi Levi Philip Kaminsky Edith Simchi LeviDokument29 SeitenInstructor Manual For Designing and Managing The Supply Chain 3e by David Simchi Levi Philip Kaminsky Edith Simchi Levigleesomecystideagpdm100% (11)

- Theory of PricingDokument48 SeitenTheory of PricingDedipyaNoch keine Bewertungen

- Industry Demand and Company DemandDokument20 SeitenIndustry Demand and Company DemandTouseef ShagooNoch keine Bewertungen

- Master Vikas EconomicsDokument8 SeitenMaster Vikas Economicshoney_gupta_5Noch keine Bewertungen

- Aggregate Supply & Business Cycles: Unit HighlightsDokument14 SeitenAggregate Supply & Business Cycles: Unit HighlightsprabodhNoch keine Bewertungen

- Determinants of PESDokument5 SeitenDeterminants of PESUgly DucklingNoch keine Bewertungen

- Lesson 10 - Module 1 - Supply ElasticityDokument5 SeitenLesson 10 - Module 1 - Supply ElasticityLizlee LaluanNoch keine Bewertungen

- Price Elasticity of SupplyDokument2 SeitenPrice Elasticity of SupplycrisNoch keine Bewertungen

- Econ ScriptDokument4 SeitenEcon ScriptnanaNoch keine Bewertungen

- Aligarh Collage of Engineering AND Technology, Aligarh Project Report ON SupplyDokument20 SeitenAligarh Collage of Engineering AND Technology, Aligarh Project Report ON SupplyPriyaNoch keine Bewertungen

- Unit IV Answers OriginalDokument11 SeitenUnit IV Answers OriginalRutvij GiteNoch keine Bewertungen

- Econ Macroeconomics 4 4th Edition Mceachern Solutions ManualDokument12 SeitenEcon Macroeconomics 4 4th Edition Mceachern Solutions Manualexoynambuj7100% (30)

- Presentation On Financial Management: Factors Influencing Working Capital RequirementsDokument11 SeitenPresentation On Financial Management: Factors Influencing Working Capital RequirementsjineshshajiNoch keine Bewertungen

- By Maria AhmedDokument49 SeitenBy Maria AhmedQuiz UpNoch keine Bewertungen

- Mental Brain Test Maths For StudentsDokument45 SeitenMental Brain Test Maths For StudentsmekalmandibhanuNoch keine Bewertungen

- Ch4 Aggregate SSDokument13 SeitenCh4 Aggregate SSProveedor Iptv EspañaNoch keine Bewertungen

- Course of MicroeconomicsDokument6 SeitenCourse of MicroeconomicsAbdulahi olaadNoch keine Bewertungen

- Micro EconomicsDokument10 SeitenMicro EconomicsAnkur SinhaNoch keine Bewertungen

- Aggregrate of SupplyDokument29 SeitenAggregrate of Supplyarmelimperial1Noch keine Bewertungen

- LR CostsDokument9 SeitenLR Costsnathanlpk11Noch keine Bewertungen

- Chapter 3Dokument3 SeitenChapter 3Regine Gale UlnaganNoch keine Bewertungen

- Supply Chain Operations Planning and SourcingDokument29 SeitenSupply Chain Operations Planning and SourcingSabar SimanjuntakNoch keine Bewertungen

- Time Affecting The Price Elasticity of Demand and SupplyDokument5 SeitenTime Affecting The Price Elasticity of Demand and SupplyAbdulahi olaadNoch keine Bewertungen

- Elasticity and Its Application: Solutions To Text ProblemsDokument6 SeitenElasticity and Its Application: Solutions To Text ProblemsterrancekuNoch keine Bewertungen

- BSECO - 12 (Aggregate Supply Curve)Dokument15 SeitenBSECO - 12 (Aggregate Supply Curve)Paris AliNoch keine Bewertungen

- ElasticityDokument4 SeitenElasticityUnicorn ProjectNoch keine Bewertungen

- 42 ECO SAT-2 From Vikash AgrawalDokument15 Seiten42 ECO SAT-2 From Vikash AgrawalVikash AgrawalNoch keine Bewertungen

- Chap 2 Solutions PDFDokument19 SeitenChap 2 Solutions PDFanon_461458122Noch keine Bewertungen

- SUPPLY Bba NotesDokument9 SeitenSUPPLY Bba NotesAbhiNoch keine Bewertungen

- Chap 10Dokument11 SeitenChap 10Ahsan AliNoch keine Bewertungen

- Year 11 EconomiesDokument10 SeitenYear 11 EconomiesKabNoch keine Bewertungen

- Supply Curve Ppt-1Dokument18 SeitenSupply Curve Ppt-1mansi mehtaNoch keine Bewertungen

- MicroEconomics AssignmentDokument15 SeitenMicroEconomics AssignmentMayankNoch keine Bewertungen

- Mos Game Writeup b10Dokument2 SeitenMos Game Writeup b10Siddharth BathlaNoch keine Bewertungen

- Activity 6 - Theory of Production and CostDokument5 SeitenActivity 6 - Theory of Production and CostJelo DavidNoch keine Bewertungen

- Unit - 3: Supply: Learning OutcomesDokument38 SeitenUnit - 3: Supply: Learning OutcomesZoya SarwatNoch keine Bewertungen

- 11 Determinants of Working Capital - Financial ManagementDokument3 Seiten11 Determinants of Working Capital - Financial ManagementsharmilaNoch keine Bewertungen

- Aggregate Supply: Economy at Potential Gross Domestic Product Microeconomic ViewDokument6 SeitenAggregate Supply: Economy at Potential Gross Domestic Product Microeconomic ViewMAk KhanNoch keine Bewertungen

- Lesson 4: The Full Macroeconomic Model ObjectivesDokument26 SeitenLesson 4: The Full Macroeconomic Model ObjectivesAChristensen1299Noch keine Bewertungen

- Price Elasticity of Supply: by Paarssh MehtaDokument9 SeitenPrice Elasticity of Supply: by Paarssh MehtaPaarssh MehtaNoch keine Bewertungen

- Law of SupplyDokument26 SeitenLaw of SupplyCindy BartolayNoch keine Bewertungen

- Economics Complete 2setDokument35 SeitenEconomics Complete 2setYash koradiaNoch keine Bewertungen

- Factors Affecting The Price Elasticity of SupplyDokument1 SeiteFactors Affecting The Price Elasticity of SupplyshintaNoch keine Bewertungen

- Impact of Price Elasticity of Supply and DemandDokument8 SeitenImpact of Price Elasticity of Supply and DemandAlexander ShresthaNoch keine Bewertungen

- Length of Period of ManufactureDokument6 SeitenLength of Period of ManufacturegayathriNoch keine Bewertungen

- Forest EcosystemDokument3 SeitenForest EcosystemKarpagam MahadevanNoch keine Bewertungen

- The Carbon CurrencyDokument9 SeitenThe Carbon CurrencyKarpagam MahadevanNoch keine Bewertungen

- Reaction FunctionDokument4 SeitenReaction FunctionKarpagam Mahadevan0% (1)

- Consumer SurplusDokument7 SeitenConsumer SurplusKarpagam MahadevanNoch keine Bewertungen

- Green Economy and TradeDokument302 SeitenGreen Economy and TradeKarpagam MahadevanNoch keine Bewertungen

- Asymmetric InformationDokument15 SeitenAsymmetric InformationKarpagam MahadevanNoch keine Bewertungen

- Price EffectDokument6 SeitenPrice EffectKarpagam MahadevanNoch keine Bewertungen

- Environmental Performance Evaluation and Indicators: Christine JaschDokument10 SeitenEnvironmental Performance Evaluation and Indicators: Christine JaschKarpagam MahadevanNoch keine Bewertungen

- Ap-5901 SheDokument7 SeitenAp-5901 SheLizette Oliva80% (5)

- This Study Resource Was: MPO FenêtresDokument4 SeitenThis Study Resource Was: MPO FenêtresRana HassanNoch keine Bewertungen

- Supply Chain Management - KishoreDokument19 SeitenSupply Chain Management - KishorekishorechakravarthyNoch keine Bewertungen

- Journal of CompetitivenessDokument127 SeitenJournal of CompetitivenessShifat HasanNoch keine Bewertungen

- Chocolate Industry FinalDokument19 SeitenChocolate Industry FinalLakshmi Kapoor100% (1)

- Imran Zulfiqar: Career ObjectiveDokument3 SeitenImran Zulfiqar: Career ObjectiveImran ZulfiqarNoch keine Bewertungen

- Marketing in Banking Sector-A Case Study On DBBLDokument34 SeitenMarketing in Banking Sector-A Case Study On DBBLAhsan Azhar Shopan50% (2)

- Interest: Interest Is A Fee That Is Charged For The Use of Someone Else's Money. The Size of The Fee Will DependDokument2 SeitenInterest: Interest Is A Fee That Is Charged For The Use of Someone Else's Money. The Size of The Fee Will DependAlexandra BanteguiNoch keine Bewertungen

- Trading Bot Concept PDFDokument4 SeitenTrading Bot Concept PDFyZdXA5MDTirXw3uvD4Y2GL9NNoch keine Bewertungen

- BAB 5 - Consumer Behaviour Consumer BankingDokument67 SeitenBAB 5 - Consumer Behaviour Consumer BankingSyai GenjNoch keine Bewertungen

- p1139 WilsonDokument8 Seitenp1139 WilsondnvnNoch keine Bewertungen

- Relative Valuations FINALDokument44 SeitenRelative Valuations FINALChinmay ShirsatNoch keine Bewertungen

- Ncda ResumeDokument2 SeitenNcda Resumeapi-446321851Noch keine Bewertungen

- CoaseDokument20 SeitenCoasepwalker_25100% (1)

- Tybms C (Marketing) - Project Title (2022-23)Dokument4 SeitenTybms C (Marketing) - Project Title (2022-23)Aryan SawardekarNoch keine Bewertungen

- Managerial EconomicsDokument199 SeitenManagerial EconomicsAnonymous yy8In96j0rNoch keine Bewertungen

- The Calculations Are Based On "A Sustainable Spending Rate Without Simulation" by M. A. Milevsky & Ch. Robinson, FAJ Vol 61 No 6, 2005Dokument6 SeitenThe Calculations Are Based On "A Sustainable Spending Rate Without Simulation" by M. A. Milevsky & Ch. Robinson, FAJ Vol 61 No 6, 2005morrisonkaniu8283Noch keine Bewertungen

- RbiDokument1 SeiteRbibhawani shankar SharmaNoch keine Bewertungen

- Responsibility CenterDokument14 SeitenResponsibility CenterKashif TradingNoch keine Bewertungen

- Digital Marketing ProjectDokument23 SeitenDigital Marketing ProjectALi KhanNoch keine Bewertungen

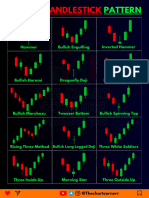

- Chart Pattern Cheat Sheet-1Dokument18 SeitenChart Pattern Cheat Sheet-1YASHANK VISHWAKARMANoch keine Bewertungen

- Marketing Management: Chapter-10 Crafting The Brand PositioningDokument34 SeitenMarketing Management: Chapter-10 Crafting The Brand PositioningBilal Raja75% (4)

- MMM SyllabusDokument17 SeitenMMM Syllabusbhar4tpNoch keine Bewertungen

- A Practioners Toolkit On ValuationDokument6 SeitenA Practioners Toolkit On ValuationhoalongkiemNoch keine Bewertungen

- Idea Submission TemplateDokument9 SeitenIdea Submission TemplateDarkartsNoch keine Bewertungen

- GSTIN: 29AACCF1132H2ZX CIN: U67190MH2012PTC337657 Pan: Aaccf1132H State Code: 29Dokument1 SeiteGSTIN: 29AACCF1132H2ZX CIN: U67190MH2012PTC337657 Pan: Aaccf1132H State Code: 29SRIDHAR SUNKARINoch keine Bewertungen

- DerivSERV Technical Specification - Equity Derivatives v6.0 Revision 4Dokument255 SeitenDerivSERV Technical Specification - Equity Derivatives v6.0 Revision 4Binny SharmaNoch keine Bewertungen

- Challenges Facing EQUITY BANKDokument52 SeitenChallenges Facing EQUITY BANKSimon Muteke50% (2)