Das könnte Ihnen auch gefallen

- Rich Dad Poor Dad PresentationDokument31 SeitenRich Dad Poor Dad Presentationbindu15100% (1)

- Global Financial MarketsDokument37 SeitenGlobal Financial MarketsSangram PandaNoch keine Bewertungen

- Basic Functions of MarketingDokument10 SeitenBasic Functions of MarketingRaunak ChaudhuryNoch keine Bewertungen

- Consolidated Financial StatementsDokument7 SeitenConsolidated Financial StatementsParvez NahidNoch keine Bewertungen

- Kotak StatementDokument5 SeitenKotak StatementAdv RINKY JAISWALNoch keine Bewertungen

- Economics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsVon EverandEconomics for Investment Decision Makers Workbook: Micro, Macro, and International EconomicsNoch keine Bewertungen

- Account StatementDokument132 SeitenAccount StatementBASHA SHAFIQNoch keine Bewertungen

- Product DevelopmentDokument23 SeitenProduct DevelopmentMuhammad ShahidNoch keine Bewertungen

- Introduction To Engineering EconomyDokument9 SeitenIntroduction To Engineering Economymayka mawrinNoch keine Bewertungen

- REVIEWER ME (Finals)Dokument17 SeitenREVIEWER ME (Finals)cynthia karylle natividadNoch keine Bewertungen

- Chapter 2Dokument25 SeitenChapter 2faulau100% (1)

- Market Positioning Assignment PDFDokument5 SeitenMarket Positioning Assignment PDFazar emraanNoch keine Bewertungen

- Daniel Geto Article ReviewDokument14 SeitenDaniel Geto Article ReviewTikeher DemenaNoch keine Bewertungen

- A Product Is What The Company Has To OfferDokument4 SeitenA Product Is What The Company Has To OfferapplesbyNoch keine Bewertungen

- Global Markets: Brand Image Brand IdentityDokument4 SeitenGlobal Markets: Brand Image Brand IdentityKris Marie Eullaran TorresNoch keine Bewertungen

- Carrer FinanceDokument12 SeitenCarrer Financeusefulthomas67Noch keine Bewertungen

- Managerial Eco q-4Dokument9 SeitenManagerial Eco q-4Ritik katochNoch keine Bewertungen

- DerivativesDokument9 SeitenDerivativesrududu duduNoch keine Bewertungen

- Page - Chapter 3 - Financial Instruments, Financial Markets, and Financial InstitutionsDokument5 SeitenPage - Chapter 3 - Financial Instruments, Financial Markets, and Financial InstitutionsJoginder S AhlawatNoch keine Bewertungen

- Task 11 - 223Dokument17 SeitenTask 11 - 223Eswar Sai VenkatNoch keine Bewertungen

- Pricing Types: Signalling Market Positioning IntentVon EverandPricing Types: Signalling Market Positioning IntentNoch keine Bewertungen

- Introduction To Derivatives: July 26, 2002 11:57 I26-Ch01 Sheet Number 1 Page Number 1Dokument18 SeitenIntroduction To Derivatives: July 26, 2002 11:57 I26-Ch01 Sheet Number 1 Page Number 1iubianmmnNoch keine Bewertungen

- Marketing-5 4Dokument12 SeitenMarketing-5 4Bryan GonzalesNoch keine Bewertungen

- Introductions: 1.1 Purpose of The Project DefinitionDokument10 SeitenIntroductions: 1.1 Purpose of The Project Definitionnaruto boeingNoch keine Bewertungen

- Task 16 Ch.l.sri KariDokument41 SeitenTask 16 Ch.l.sri KariEswar Sai VenkatNoch keine Bewertungen

- Notes For FRMDokument6 SeitenNotes For FRMAshutosh PandeyNoch keine Bewertungen

- Good Morningeryone!!!!!Dokument24 SeitenGood Morningeryone!!!!!allengplNoch keine Bewertungen

- Difference Between Customer and ConsumerDokument12 SeitenDifference Between Customer and ConsumerdushyantNoch keine Bewertungen

- Describe Dif CostsDokument6 SeitenDescribe Dif Costsvanerie manumbaleNoch keine Bewertungen

- Im - Module - IVDokument28 SeitenIm - Module - IVCH ANIL VARMANoch keine Bewertungen

- Describe Dif CostsDokument6 SeitenDescribe Dif Costsvanerie manumbaleNoch keine Bewertungen

- Unit Objectives and Methods: StructureDokument15 SeitenUnit Objectives and Methods: Structure009sidNoch keine Bewertungen

- Price Can Be Quoted To Currency, Quantities of Goods or VouchersDokument2 SeitenPrice Can Be Quoted To Currency, Quantities of Goods or VouchersKaranNoch keine Bewertungen

- Summary Mba525Dokument27 SeitenSummary Mba525navjot2k2Noch keine Bewertungen

- Market Dynamics.Dokument6 SeitenMarket Dynamics.abidmehrajNoch keine Bewertungen

- 4 5810dbusinessmarketingbook PDFDokument506 Seiten4 5810dbusinessmarketingbook PDFMatshele SerageNoch keine Bewertungen

- The Perfectly Competitive FirmDokument13 SeitenThe Perfectly Competitive FirmMaria StancanNoch keine Bewertungen

- Underlying and The Changes in Volatility. Factors Contributing To These Risks Are ManyDokument74 SeitenUnderlying and The Changes in Volatility. Factors Contributing To These Risks Are ManyAzaruddin Shaik B PositiveNoch keine Bewertungen

- Microeconomics ExternalitiesDokument19 SeitenMicroeconomics ExternalitiesNorweste SurgicalNoch keine Bewertungen

- Marketing ManagementDokument26 SeitenMarketing ManagementKali PandiNoch keine Bewertungen

- Factors To Consider When Setting Prices and Its General Pricing ApproachesDokument5 SeitenFactors To Consider When Setting Prices and Its General Pricing Approacheschelseamanacho11Noch keine Bewertungen

- Module IIDokument13 SeitenModule IIRajesh MgNoch keine Bewertungen

- Name Sachin Kumar Student Id: Q1004197 Module Name: Economics For BusinessDokument13 SeitenName Sachin Kumar Student Id: Q1004197 Module Name: Economics For BusinessShashank JainNoch keine Bewertungen

- Entrep 1-3Dokument23 SeitenEntrep 1-3Fainted HopeNoch keine Bewertungen

- LLLLLLLLLLLLLLLL HHHHHHHHHHHHHH Introduction To Cooperative Marketing Zvi GalorDokument13 SeitenLLLLLLLLLLLLLLLL HHHHHHHHHHHHHH Introduction To Cooperative Marketing Zvi GalorahmedtaniNoch keine Bewertungen

- ASSIGNMENT (Marketng) - GOPIKA PDokument10 SeitenASSIGNMENT (Marketng) - GOPIKA PAmrutha P RNoch keine Bewertungen

- Frameworks in The Financial Engineering Domain An Experience ReportDokument15 SeitenFrameworks in The Financial Engineering Domain An Experience Report1man1bookNoch keine Bewertungen

- Week 8 CONCEPT AND COMPONENTS OF MARKETING MIXDokument13 SeitenWeek 8 CONCEPT AND COMPONENTS OF MARKETING MIXPrincess Manelle de VeraNoch keine Bewertungen

- Introduction of Marketing MixDokument5 SeitenIntroduction of Marketing MixManoranjan BisoyiNoch keine Bewertungen

- Chapter 3-Market and Competitive Space: Prepared By: Hiba Assaf & Nathalie FakhryDokument7 SeitenChapter 3-Market and Competitive Space: Prepared By: Hiba Assaf & Nathalie FakhryKarl haddadNoch keine Bewertungen

- Business - Law - Marks 10Dokument14 SeitenBusiness - Law - Marks 10Server IssueNoch keine Bewertungen

- Business Week4, QuizDokument12 SeitenBusiness Week4, QuizadaNoch keine Bewertungen

- Task 12, 13, 14Dokument7 SeitenTask 12, 13, 14bendermacherrickNoch keine Bewertungen

- Fall 2017Dokument11 SeitenFall 2017Kripaya ShakyaNoch keine Bewertungen

- Product Management Chapter 1Dokument18 SeitenProduct Management Chapter 1Ramesh SafareNoch keine Bewertungen

- BundlingDokument2 SeitenBundlinghpeter195798Noch keine Bewertungen

- Assignment of Managerial Economy: Mohamed Omar MahamoudDokument8 SeitenAssignment of Managerial Economy: Mohamed Omar MahamoudMohamed OmarionNoch keine Bewertungen

- Chapter Review 7Dokument3 SeitenChapter Review 7Tória RajabecNoch keine Bewertungen

- Marketing ChannelDokument4 SeitenMarketing ChannelDato Seri Iebal SanchezNoch keine Bewertungen

- Chapter 9: Pricing and FinancingDokument23 SeitenChapter 9: Pricing and Financingbakshi_sNoch keine Bewertungen

- NotesDokument17 SeitenNotesKripaya ShakyaNoch keine Bewertungen

- 74664bos60481 FND p4 cp4 U1Dokument15 Seiten74664bos60481 FND p4 cp4 U1Pushpinder KumarNoch keine Bewertungen

- Dark Markets: A Literature Review.: AbstractDokument15 SeitenDark Markets: A Literature Review.: AbstractPatrickNoch keine Bewertungen

- RE Inv IntroDokument13 SeitenRE Inv IntroShafiq NezatNoch keine Bewertungen

- B203B-Week 4 - (Accounting-1)Dokument11 SeitenB203B-Week 4 - (Accounting-1)ahmed helmyNoch keine Bewertungen

- Adnan ThesisDokument51 SeitenAdnan ThesisMohammad Naveed Hashmi100% (1)

- MCQ On Current Trends Cases in FinanceDokument20 SeitenMCQ On Current Trends Cases in FinanceSanju Das100% (1)

- Asset Rotation Fund: Tactical and FlexibleDokument2 SeitenAsset Rotation Fund: Tactical and FlexibleEttore TruccoNoch keine Bewertungen

- The Revenue CycleDokument36 SeitenThe Revenue CycleGerlyn Dasalla ClaorNoch keine Bewertungen

- CIVABTech66829BrEstrAP - Valuation NumericalsDokument3 SeitenCIVABTech66829BrEstrAP - Valuation NumericalsAditiNoch keine Bewertungen

- Gmail - Expedia Travel Confirmation - Wed, Jul 19 - (Itinerary # 72593634072884)Dokument4 SeitenGmail - Expedia Travel Confirmation - Wed, Jul 19 - (Itinerary # 72593634072884)LUZ URREANoch keine Bewertungen

- Slides Macroeconomics 1 - FTUDokument50 SeitenSlides Macroeconomics 1 - FTUK60 Nguyễn Ái Huyền TrangNoch keine Bewertungen

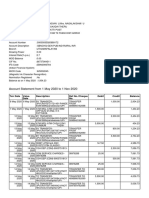

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument9 SeitenAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiNoch keine Bewertungen

- Chapter 3. The Optimal Capital Budget: The Investment Opportunity Schedule (IOS)Dokument14 SeitenChapter 3. The Optimal Capital Budget: The Investment Opportunity Schedule (IOS)shiprabansal_123Noch keine Bewertungen

- Chapter 8: Cash and Bank Management Daily Procedures: ObjectivesDokument26 SeitenChapter 8: Cash and Bank Management Daily Procedures: ObjectivesArturo GonzalezNoch keine Bewertungen

- Convertibility of RupeeDokument14 SeitenConvertibility of RupeeArun MishraNoch keine Bewertungen

- Biotechusa KFT Beu24008891Dokument1 SeiteBiotechusa KFT Beu24008891peicivek5Noch keine Bewertungen

- Account Statement As of 21-03-2020 11:43:46 GMT +0530Dokument2 SeitenAccount Statement As of 21-03-2020 11:43:46 GMT +0530Sourabh MeenaNoch keine Bewertungen

- Neighborhood 3 B29 L19Dokument4 SeitenNeighborhood 3 B29 L19Kate CastañaresNoch keine Bewertungen

- SIP 2023 Project Akshay Dakhale 20233Dokument48 SeitenSIP 2023 Project Akshay Dakhale 20233Aniket KambleNoch keine Bewertungen

- Is LM2Dokument8 SeitenIs LM2samu123djghoshNoch keine Bewertungen

- Correct?Dokument29 SeitenCorrect?Hong Anh NguyenNoch keine Bewertungen

- Individual Assignment Financial ManagementDokument17 SeitenIndividual Assignment Financial ManagementUtheu Budhi Susetyo100% (1)

- FIRMS - User ManualDokument112 SeitenFIRMS - User ManualAnkit AgarwalNoch keine Bewertungen

- Guidelines On Securitisation of Standard AssetsDokument14 SeitenGuidelines On Securitisation of Standard AssetsPrianca GalaNoch keine Bewertungen

- The Jap YenDokument13 SeitenThe Jap YenRadhika KashyapNoch keine Bewertungen

- FIN 420 CASE STUDY Leverage RatioDokument4 SeitenFIN 420 CASE STUDY Leverage RatioNur AdibahNoch keine Bewertungen

- FM II Assignment 19 19Dokument1 SeiteFM II Assignment 19 19RaaziaNoch keine Bewertungen

- Bus 5111: Financial Management: Written Assignment Unit 1 Ratios CalculationDokument5 SeitenBus 5111: Financial Management: Written Assignment Unit 1 Ratios CalculationCharles IrikefeNoch keine Bewertungen

- Solution 786526Dokument38 SeitenSolution 786526Anvesha AgarwalNoch keine Bewertungen