Das könnte Ihnen auch gefallen

- Contract Research Organizations An Industry AnalysisDokument25 SeitenContract Research Organizations An Industry AnalysisJürgen FleischerNoch keine Bewertungen

- Purchasing Medical Innovation: The Right Technology, for the Right Patient, at the Right PriceVon EverandPurchasing Medical Innovation: The Right Technology, for the Right Patient, at the Right PriceNoch keine Bewertungen

- Cross Roads in Quality 2008Hlth AffairsDokument11 SeitenCross Roads in Quality 2008Hlth AffairsVaida BankauskaiteNoch keine Bewertungen

- Pharma Medical Affairs 2020Dokument9 SeitenPharma Medical Affairs 2020Prateek AgarwalNoch keine Bewertungen

- Measuring the Gains from Medical Research: An Economic ApproachVon EverandMeasuring the Gains from Medical Research: An Economic ApproachNoch keine Bewertungen

- Exploring Why Global Health Needs Are Unmet by Research Efforts: The Potential Influences of Geography, Industry and Publication IncentivesDokument14 SeitenExploring Why Global Health Needs Are Unmet by Research Efforts: The Potential Influences of Geography, Industry and Publication IncentivesDorakolliopoulouNoch keine Bewertungen

- Unhealthy Politics: The Battle over Evidence-Based MedicineVon EverandUnhealthy Politics: The Battle over Evidence-Based MedicineBewertung: 4 von 5 Sternen4/5 (1)

- Letter To CIHRDokument12 SeitenLetter To CIHRTimothy AvilaNoch keine Bewertungen

- Healthcare in the United States: Clinical, Financial, and Operational DimensionsVon EverandHealthcare in the United States: Clinical, Financial, and Operational DimensionsNoch keine Bewertungen

- Research Paper Health Care ReformDokument4 SeitenResearch Paper Health Care Reformsjcuwurif100% (1)

- National Health Policy: What Role for Government?Von EverandNational Health Policy: What Role for Government?Bewertung: 5 von 5 Sternen5/5 (1)

- 04 International 3 PDFDokument12 Seiten04 International 3 PDFjumaidi ratnaNoch keine Bewertungen

- Notes and Editing Sheet2Dokument3 SeitenNotes and Editing Sheet2Christian HawthorneNoch keine Bewertungen

- Greg Simon #1 v7Dokument9 SeitenGreg Simon #1 v7ogangurelNoch keine Bewertungen

- Research Paper On Healthcare in The United StatesDokument8 SeitenResearch Paper On Healthcare in The United Statesafedetbma100% (1)

- Project Report of International Hospital BanditaDokument99 SeitenProject Report of International Hospital Banditapolly1963Noch keine Bewertungen

- Avoidable Costs in HealthcareDokument62 SeitenAvoidable Costs in HealthcareAnthony WilsonNoch keine Bewertungen

- Research Paper On Health Care CostsDokument6 SeitenResearch Paper On Health Care Costsgw1nm9nb100% (1)

- N Vitalari A Prospective Analysis of The Healthcare IndustryDokument47 SeitenN Vitalari A Prospective Analysis of The Healthcare IndustryKiran DuggarajuNoch keine Bewertungen

- OutDokument46 SeitenOutsertacariNoch keine Bewertungen

- Brett J. Skinner. - Canadian Health Policy Failures - What's Wrong, Who Gets Hurt, and Why Nothing Changes (2009) PDFDokument282 SeitenBrett J. Skinner. - Canadian Health Policy Failures - What's Wrong, Who Gets Hurt, and Why Nothing Changes (2009) PDFElviraNoch keine Bewertungen

- Health Research and DevelopmentDokument4 SeitenHealth Research and DevelopmentInterActionNoch keine Bewertungen

- Research Paper On Health Care ReformDokument4 SeitenResearch Paper On Health Care Reformgz7vhnpe100% (1)

- Protecting Biopharmaceutical Innovation Means Hope For New Treatments For PatientsDokument4 SeitenProtecting Biopharmaceutical Innovation Means Hope For New Treatments For PatientsPatientsPatentsNoch keine Bewertungen

- Evidence-Based Public HealthDokument312 SeitenEvidence-Based Public HealthBudi Lamaka100% (7)

- A Framework To Measure The Impact of Investments in Health ResearchDokument16 SeitenA Framework To Measure The Impact of Investments in Health ResearchGesler Pilvan SainNoch keine Bewertungen

- Dae MM Rich 2014Dokument13 SeitenDae MM Rich 2014PhyoNyeinChanNoch keine Bewertungen

- Essay: Corporate and Government Funding Means That Scientists Today Cannot Be NeutralDokument6 SeitenEssay: Corporate and Government Funding Means That Scientists Today Cannot Be Neutralsweet rabia brohiNoch keine Bewertungen

- What Passes and Fails As Health Policy and Management: Behind The JargonDokument14 SeitenWhat Passes and Fails As Health Policy and Management: Behind The JargonterenachintyaNoch keine Bewertungen

- New England Journal of Medicine Ranking 37th - Measuring The Performance of The U.S. Health Care SystemDokument2 SeitenNew England Journal of Medicine Ranking 37th - Measuring The Performance of The U.S. Health Care SystemPaul JohnsonNoch keine Bewertungen

- Data Financing Global Health Lancet 2009Dokument2 SeitenData Financing Global Health Lancet 2009peteramicoNoch keine Bewertungen

- Guide To Writing Grant ProposalsDokument15 SeitenGuide To Writing Grant ProposalsMartina NoelNoch keine Bewertungen

- Doctors and Drug Companies - Still Cozy After All These Years (2010)Dokument2 SeitenDoctors and Drug Companies - Still Cozy After All These Years (2010)EMFsafetyNoch keine Bewertungen

- Comparative Effectiveness HA - Oct 2010Dokument1 SeiteComparative Effectiveness HA - Oct 2010anndemareeNoch keine Bewertungen

- Role of Industry in Clinical Care, Research and Education: A Guide To Interactions With IndustryDokument11 SeitenRole of Industry in Clinical Care, Research and Education: A Guide To Interactions With IndustryTylerNoch keine Bewertungen

- Global Biomedical Industry: Preserving U.S. Leadership - Full ReportDokument71 SeitenGlobal Biomedical Industry: Preserving U.S. Leadership - Full ReportCouncil for American Medical InnovationNoch keine Bewertungen

- FRANCO CreationHealthConsumerDokument21 SeitenFRANCO CreationHealthConsumerRogerio Lima BarbosaNoch keine Bewertungen

- How To Write A Research Paper On Health Care ReformDokument7 SeitenHow To Write A Research Paper On Health Care Reformlyn0l1gamop2Noch keine Bewertungen

- NIH Public Access: Author ManuscriptDokument16 SeitenNIH Public Access: Author Manuscriptashgee1Noch keine Bewertungen

- SFN NihDokument2 SeitenSFN NihKKNoch keine Bewertungen

- Healt (15384)Dokument110 SeitenHealt (15384)Oscar Javier Gaitan TrujilloNoch keine Bewertungen

- Novartis: Sell SellDokument8 SeitenNovartis: Sell SellDeron LaiNoch keine Bewertungen

- Thesis Health Care ReformDokument5 SeitenThesis Health Care ReformKate Campbell100% (2)

- Jurnal HBMDokument10 SeitenJurnal HBMSeindz OstenNoch keine Bewertungen

- 2020 - A New Vision A Future For Regenerative MedicineDokument33 Seiten2020 - A New Vision A Future For Regenerative MedicineGiulianoNoch keine Bewertungen

- The Importance of Biomedical ResearchDokument13 SeitenThe Importance of Biomedical ResearchEmily CribasNoch keine Bewertungen

- Us Healthcare Research Paper TopicsDokument6 SeitenUs Healthcare Research Paper Topicsaflbasnka100% (1)

- The Profit Motive and Patient CareDokument448 SeitenThe Profit Motive and Patient CareTCFdotorgNoch keine Bewertungen

- Dissertation Funding Public HealthDokument5 SeitenDissertation Funding Public HealthWriteMyPaperCanadaUK100% (1)

- Health Care Policy Research Paper TopicsDokument4 SeitenHealth Care Policy Research Paper Topicsgsrkoxplg100% (1)

- Welcome To Our First Weekly Discussion!: CollapseDokument7 SeitenWelcome To Our First Weekly Discussion!: CollapsetugaNoch keine Bewertungen

- Tackling Out-Of-Pocket Health Care Costs A Discussion Paper: Lesley Russell Jennifer DoggettDokument15 SeitenTackling Out-Of-Pocket Health Care Costs A Discussion Paper: Lesley Russell Jennifer DoggettLesley Russell100% (1)

- Assessing Risk and Return: Personalized Medicine Development and New Innovation ParadigmDokument34 SeitenAssessing Risk and Return: Personalized Medicine Development and New Innovation ParadigmThe Ewing Marion Kauffman Foundation100% (1)

- Asn NihDokument2 SeitenAsn NihKKNoch keine Bewertungen

- Lva1 App6892Dokument62 SeitenLva1 App6892Pallavi PalluNoch keine Bewertungen

- Hoover Institution Summer Policy Boot Camp Director's AwardDokument44 SeitenHoover Institution Summer Policy Boot Camp Director's AwardHoover InstitutionNoch keine Bewertungen

- Reductions in Funding For Medical ResearchDokument3 SeitenReductions in Funding For Medical ResearchhealthfunditNoch keine Bewertungen

- Globalisation and Health: Challenges: Go ToDokument3 SeitenGlobalisation and Health: Challenges: Go ToRembrant FernandezNoch keine Bewertungen

- Infographic: IMPACT OF MUSCULOSKELETAL DISEASEDokument1 SeiteInfographic: IMPACT OF MUSCULOSKELETAL DISEASEAdvaMedLCINoch keine Bewertungen

- The Value of Medical Technology: Impact of DiabetesDokument2 SeitenThe Value of Medical Technology: Impact of DiabetesAdvaMedLCINoch keine Bewertungen

- Chronic Pain Management Fact SheetDokument2 SeitenChronic Pain Management Fact SheetAdvaMedLCINoch keine Bewertungen

- The Importance of Diagnostic Tests in Fighting Infectious DiseasesDokument2 SeitenThe Importance of Diagnostic Tests in Fighting Infectious DiseasesAdvaMedLCINoch keine Bewertungen

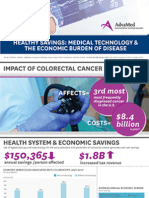

- Infographic: HEALTHY SAVINGS: MEDICAL TECHNOLOGY & THE ECONOMIC BURDEN OF DISEASEDokument1 SeiteInfographic: HEALTHY SAVINGS: MEDICAL TECHNOLOGY & THE ECONOMIC BURDEN OF DISEASEAdvaMedLCINoch keine Bewertungen

- The Value of Medical Technology: Managing Chronic PainDokument2 SeitenThe Value of Medical Technology: Managing Chronic PainAdvaMedLCINoch keine Bewertungen

- 2015 Innovation AgendaDokument1 Seite2015 Innovation AgendaAdvaMedLCINoch keine Bewertungen

- Infographic: IMPACT OF COLORECTAL CANCERDokument1 SeiteInfographic: IMPACT OF COLORECTAL CANCERAdvaMedLCINoch keine Bewertungen

- Infographic: IMPACT OF HEART DISEASEDokument1 SeiteInfographic: IMPACT OF HEART DISEASEAdvaMedLCINoch keine Bewertungen

- Wound Treatment Infographic 2015Dokument1 SeiteWound Treatment Infographic 2015AdvaMedLCINoch keine Bewertungen

- Infographic: HEALTHY SAVINGS: MEDICAL TECHNOLOGY & THE ECONOMIC BURDEN OF DISEASEDokument1 SeiteInfographic: HEALTHY SAVINGS: MEDICAL TECHNOLOGY & THE ECONOMIC BURDEN OF DISEASEAdvaMedLCINoch keine Bewertungen

- Recent Average Price Trends For Implantable Medical Devices, 2007-2011Dokument7 SeitenRecent Average Price Trends For Implantable Medical Devices, 2007-2011AdvaMedLCINoch keine Bewertungen

- Infographic: IMPACT OF DIABETESDokument1 SeiteInfographic: IMPACT OF DIABETESAdvaMedLCINoch keine Bewertungen

- LCI Wound Treatment Toolkit 2015Dokument8 SeitenLCI Wound Treatment Toolkit 2015AdvaMedLCINoch keine Bewertungen

- The Value of Medical Technology in Controlling and Treating DiabetesDokument8 SeitenThe Value of Medical Technology in Controlling and Treating DiabetesAdvaMedLCINoch keine Bewertungen

- Impact of The Medical Device Excise TaxDokument5 SeitenImpact of The Medical Device Excise TaxAdvaMedLCINoch keine Bewertungen

- Innovation Agenda: February 2015Dokument4 SeitenInnovation Agenda: February 2015AdvaMedLCINoch keine Bewertungen

- Pulse Redefining Medical Technology InnovationDokument64 SeitenPulse Redefining Medical Technology InnovationAdvaMedLCINoch keine Bewertungen

- Social Media Stroke ToolkitDokument4 SeitenSocial Media Stroke ToolkitAdvaMedLCINoch keine Bewertungen

- MedTech Prices Lag Behind CPI, Other Medical GoodsDokument2 SeitenMedTech Prices Lag Behind CPI, Other Medical GoodsAdvaMedLCINoch keine Bewertungen

- AdvaMed Device Tax ReportDokument5 SeitenAdvaMed Device Tax ReportAdvaMedLCINoch keine Bewertungen

- The Value of Joint Replacement in Treating Patients With OsteoarthritisDokument6 SeitenThe Value of Joint Replacement in Treating Patients With OsteoarthritisAdvaMedLCINoch keine Bewertungen

- Diabetes Infographic: The Value of Medical Technology: Controlling & Treating DiabetesDokument1 SeiteDiabetes Infographic: The Value of Medical Technology: Controlling & Treating DiabetesAdvaMedLCINoch keine Bewertungen

- Estimates of Medical Device Spending in The United StatesDokument17 SeitenEstimates of Medical Device Spending in The United StatesAdvaMedLCINoch keine Bewertungen

- Oct 2012 King Report FINALDokument16 SeitenOct 2012 King Report FINALAdvaMedLCINoch keine Bewertungen

- Pulse Medical Technology Report 2012Dokument52 SeitenPulse Medical Technology Report 2012AdvaMedLCINoch keine Bewertungen

- Sustaining American Leadership: A Competitiveness Policy For The Medical Technology IndustryDokument3 SeitenSustaining American Leadership: A Competitiveness Policy For The Medical Technology IndustryAdvaMedLCINoch keine Bewertungen

- A Competitiveness Policy For The Medical Technology Industry: Six Policy Proposals To Sustain American LeadershipDokument5 SeitenA Competitiveness Policy For The Medical Technology Industry: Six Policy Proposals To Sustain American LeadershipAdvaMedLCINoch keine Bewertungen

- Employment Effects of The New Excise Tax On The Medical Device IndustryDokument30 SeitenEmployment Effects of The New Excise Tax On The Medical Device IndustryAdvaMedLCINoch keine Bewertungen

- Case Number 1Dokument1 SeiteCase Number 1ybunNoch keine Bewertungen

- Arts6 Q1 WK1Dokument28 SeitenArts6 Q1 WK1JOVELYN BAQUIRANNoch keine Bewertungen

- Department of Education: 4 QUARTER - Module 1Dokument12 SeitenDepartment of Education: 4 QUARTER - Module 1Haycel FranciscoNoch keine Bewertungen

- EU Court of Justice YouTube JudgmentDokument3 SeitenEU Court of Justice YouTube JudgmentTHROnlineNoch keine Bewertungen

- Stainless Steel Socket-Set Screws: Standard Specification ForDokument5 SeitenStainless Steel Socket-Set Screws: Standard Specification FormsbarretosNoch keine Bewertungen

- Actor Training and Emotions - Finding A BalanceDokument317 SeitenActor Training and Emotions - Finding A Balanceعامر جدونNoch keine Bewertungen

- 8200-0859-01-A0 Intlx InstallConfig EN PDFDokument94 Seiten8200-0859-01-A0 Intlx InstallConfig EN PDFFrancisco Rodriguez MartinezNoch keine Bewertungen

- Note 2491302 Routine PDFDokument2 SeitenNote 2491302 Routine PDFGaurav Aarti SuyalNoch keine Bewertungen

- The Ancient Regime by Taine, Hippolyte, 1828-1893Dokument252 SeitenThe Ancient Regime by Taine, Hippolyte, 1828-1893Gutenberg.orgNoch keine Bewertungen

- Controlled F.O.R.C.E Level 1 - Instructor Lesson PlanDokument62 SeitenControlled F.O.R.C.E Level 1 - Instructor Lesson PlanJPNoch keine Bewertungen

- Aci 355-3r11 (Ejemplos Anclajes)Dokument128 SeitenAci 355-3r11 (Ejemplos Anclajes)dnavarrete01100% (1)

- Torque Standard 35511,1Dokument4 SeitenTorque Standard 35511,1eigersumarlyNoch keine Bewertungen

- Eurocode - Load Combinations For Steel Structures - R1Dokument26 SeitenEurocode - Load Combinations For Steel Structures - R1anil97232Noch keine Bewertungen

- Edugain Rational NumbersDokument2 SeitenEdugain Rational NumbersananditaNoch keine Bewertungen

- Astm F 835 PDFDokument6 SeitenAstm F 835 PDFDan Dela Peña100% (1)

- Apple vs. Samsung Case StudyDokument23 SeitenApple vs. Samsung Case StudyJessah Mae E. Reyes100% (4)

- PI200 User Guide 230 V 50 HZDokument26 SeitenPI200 User Guide 230 V 50 HZEsneider Rodriguez BravoNoch keine Bewertungen

- Double Dare MeDokument60 SeitenDouble Dare MeShreya Kishore67% (12)

- Bs Na en 1998 2 2005Dokument18 SeitenBs Na en 1998 2 2005Kishiwa100% (1)

- Doug Casey: International Speculator UpdateDokument6 SeitenDoug Casey: International Speculator UpdateDynacor Gold Mines Inc.100% (1)

- Dru Ouy Procedure Les1801Dokument5 SeitenDru Ouy Procedure Les1801geverett2765100% (1)

- Unified Patents EPO Opposition On Velos MediaDokument37 SeitenUnified Patents EPO Opposition On Velos MediaJennifer M GallagherNoch keine Bewertungen

- Astm C 441-2017Dokument5 SeitenAstm C 441-2017Mohammed AliNoch keine Bewertungen

- Financial Accounting Canadian 2nd Edition Waybright Solutions ManualDokument36 SeitenFinancial Accounting Canadian 2nd Edition Waybright Solutions Manualkrossenflorrie355Noch keine Bewertungen

- E Book My Secret LifeDokument23 SeitenE Book My Secret LifesudumanikamanjuNoch keine Bewertungen

- Altayaar v. Etsy - AMENDED Class Action Securities Complaint PDFDokument87 SeitenAltayaar v. Etsy - AMENDED Class Action Securities Complaint PDFMark JaffeNoch keine Bewertungen

- EPO - Training Overview - 06 03 12-FinalDokument72 SeitenEPO - Training Overview - 06 03 12-FinalJussara FerreiraNoch keine Bewertungen

- Tablet Press Machine User ManualDokument100 SeitenTablet Press Machine User ManualDEEPUJ PHARMA MACHINERYNoch keine Bewertungen

- Statute of Monopolies 1623Dokument28 SeitenStatute of Monopolies 1623Srivardhan ShuklaNoch keine Bewertungen

- Desislava Stankova's Master ThesisDokument73 SeitenDesislava Stankova's Master ThesisborilbogoevNoch keine Bewertungen

- Think This, Not That: 12 Mindshifts to Breakthrough Limiting Beliefs and Become Who You Were Born to BeVon EverandThink This, Not That: 12 Mindshifts to Breakthrough Limiting Beliefs and Become Who You Were Born to BeBewertung: 2 von 5 Sternen2/5 (1)

- By the Time You Read This: The Space between Cheslie's Smile and Mental Illness—Her Story in Her Own WordsVon EverandBy the Time You Read This: The Space between Cheslie's Smile and Mental Illness—Her Story in Her Own WordsNoch keine Bewertungen

- Summary: Outlive: The Science and Art of Longevity by Peter Attia MD, With Bill Gifford: Key Takeaways, Summary & AnalysisVon EverandSummary: Outlive: The Science and Art of Longevity by Peter Attia MD, With Bill Gifford: Key Takeaways, Summary & AnalysisBewertung: 4.5 von 5 Sternen4.5/5 (42)

- The Age of Magical Overthinking: Notes on Modern IrrationalityVon EverandThe Age of Magical Overthinking: Notes on Modern IrrationalityBewertung: 4 von 5 Sternen4/5 (24)

- Why We Die: The New Science of Aging and the Quest for ImmortalityVon EverandWhy We Die: The New Science of Aging and the Quest for ImmortalityBewertung: 4 von 5 Sternen4/5 (3)

- Summary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedVon EverandSummary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedBewertung: 5 von 5 Sternen5/5 (80)

- The Obesity Code: Unlocking the Secrets of Weight LossVon EverandThe Obesity Code: Unlocking the Secrets of Weight LossBewertung: 4 von 5 Sternen4/5 (5)

- Summary: The Myth of Normal: Trauma, Illness, and Healing in a Toxic Culture By Gabor Maté MD & Daniel Maté: Key Takeaways, Summary & AnalysisVon EverandSummary: The Myth of Normal: Trauma, Illness, and Healing in a Toxic Culture By Gabor Maté MD & Daniel Maté: Key Takeaways, Summary & AnalysisBewertung: 4 von 5 Sternen4/5 (9)

- Raising Mentally Strong Kids: How to Combine the Power of Neuroscience with Love and Logic to Grow Confident, Kind, Responsible, and Resilient Children and Young AdultsVon EverandRaising Mentally Strong Kids: How to Combine the Power of Neuroscience with Love and Logic to Grow Confident, Kind, Responsible, and Resilient Children and Young AdultsBewertung: 5 von 5 Sternen5/5 (1)

- Sleep Stories for Adults: Overcome Insomnia and Find a Peaceful AwakeningVon EverandSleep Stories for Adults: Overcome Insomnia and Find a Peaceful AwakeningBewertung: 4 von 5 Sternen4/5 (3)

- The Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaVon EverandThe Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Comfort of Crows: A Backyard YearVon EverandThe Comfort of Crows: A Backyard YearBewertung: 4.5 von 5 Sternen4.5/5 (23)

- When the Body Says No by Gabor Maté: Key Takeaways, Summary & AnalysisVon EverandWhen the Body Says No by Gabor Maté: Key Takeaways, Summary & AnalysisBewertung: 3.5 von 5 Sternen3.5/5 (2)

- ADHD is Awesome: A Guide to (Mostly) Thriving with ADHDVon EverandADHD is Awesome: A Guide to (Mostly) Thriving with ADHDBewertung: 5 von 5 Sternen5/5 (1)

- The Ritual Effect: From Habit to Ritual, Harness the Surprising Power of Everyday ActionsVon EverandThe Ritual Effect: From Habit to Ritual, Harness the Surprising Power of Everyday ActionsBewertung: 3.5 von 5 Sternen3.5/5 (3)

- Outlive: The Science and Art of Longevity by Peter Attia: Key Takeaways, Summary & AnalysisVon EverandOutlive: The Science and Art of Longevity by Peter Attia: Key Takeaways, Summary & AnalysisBewertung: 4 von 5 Sternen4/5 (1)

- Mindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessVon EverandMindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessBewertung: 4.5 von 5 Sternen4.5/5 (328)

- The Courage Habit: How to Accept Your Fears, Release the Past, and Live Your Courageous LifeVon EverandThe Courage Habit: How to Accept Your Fears, Release the Past, and Live Your Courageous LifeBewertung: 4.5 von 5 Sternen4.5/5 (253)

- Gut: the new and revised Sunday Times bestsellerVon EverandGut: the new and revised Sunday Times bestsellerBewertung: 4 von 5 Sternen4/5 (392)

- Raising Good Humans: A Mindful Guide to Breaking the Cycle of Reactive Parenting and Raising Kind, Confident KidsVon EverandRaising Good Humans: A Mindful Guide to Breaking the Cycle of Reactive Parenting and Raising Kind, Confident KidsBewertung: 4.5 von 5 Sternen4.5/5 (169)

- Dark Psychology & Manipulation: Discover How To Analyze People and Master Human Behaviour Using Emotional Influence Techniques, Body Language Secrets, Covert NLP, Speed Reading, and Hypnosis.Von EverandDark Psychology & Manipulation: Discover How To Analyze People and Master Human Behaviour Using Emotional Influence Techniques, Body Language Secrets, Covert NLP, Speed Reading, and Hypnosis.Bewertung: 4.5 von 5 Sternen4.5/5 (110)

- To Explain the World: The Discovery of Modern ScienceVon EverandTo Explain the World: The Discovery of Modern ScienceBewertung: 3.5 von 5 Sternen3.5/5 (51)

- An Autobiography of Trauma: A Healing JourneyVon EverandAn Autobiography of Trauma: A Healing JourneyBewertung: 5 von 5 Sternen5/5 (2)

- 12 Rules for Life by Jordan B. Peterson - Book Summary: An Antidote to ChaosVon Everand12 Rules for Life by Jordan B. Peterson - Book Summary: An Antidote to ChaosBewertung: 4.5 von 5 Sternen4.5/5 (207)