Das könnte Ihnen auch gefallen

- Pepsi BCG Matrix With ExampleDokument2 SeitenPepsi BCG Matrix With ExampleMunish PathaniaNoch keine Bewertungen

- Project Presentation ON: Paper Rock PicturesDokument18 SeitenProject Presentation ON: Paper Rock PicturesMunish PathaniaNoch keine Bewertungen

- Concepts and Techniques: Data MiningDokument54 SeitenConcepts and Techniques: Data MiningMunish PathaniaNoch keine Bewertungen

- MCS of InfosysDokument7 SeitenMCS of InfosysMunish PathaniaNoch keine Bewertungen

- Import Public Class Public Static Void NullDokument1 SeiteImport Public Class Public Static Void NullMunish PathaniaNoch keine Bewertungen

- Human Resource PlanningDokument14 SeitenHuman Resource PlanningMunish Pathania50% (2)

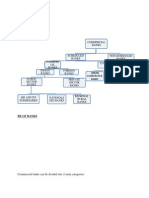

- Structure of Commercial BanksDokument4 SeitenStructure of Commercial BanksMunish PathaniaNoch keine Bewertungen

- Hardware and Software ConceptsDokument21 SeitenHardware and Software ConceptsMunish PathaniaNoch keine Bewertungen

- Functions of RbiDokument4 SeitenFunctions of RbiMunish PathaniaNoch keine Bewertungen

- Role of BanksDokument2 SeitenRole of BanksMunish PathaniaNoch keine Bewertungen

- Perception of Customer Services Provided by Axis BankDokument45 SeitenPerception of Customer Services Provided by Axis BankMunish Pathania100% (1)

- Project Report ON Credit RatingDokument76 SeitenProject Report ON Credit RatingMunish Pathania0% (1)

- Presentation On Research Methodology: Coordinated By:-Anjali Amandeep Kaur Jyoti Amita Chandan SinghDokument11 SeitenPresentation On Research Methodology: Coordinated By:-Anjali Amandeep Kaur Jyoti Amita Chandan SinghMunish Pathania100% (1)

- Enterprise Resource Planning: Management Information Systems by Sahil RajDokument11 SeitenEnterprise Resource Planning: Management Information Systems by Sahil RajMunish PathaniaNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- MOOg 45-64Dokument72 SeitenMOOg 45-64Zeniah Arizo100% (1)

- Sahay Gem Terms of Service - 1619000451Dokument7 SeitenSahay Gem Terms of Service - 1619000451abhisir25Noch keine Bewertungen

- CA INTER CompilerDokument12 SeitenCA INTER CompilernehajnvniwarsiNoch keine Bewertungen

- Loan Application FormDokument5 SeitenLoan Application FormSamantha SinghNoch keine Bewertungen

- 604 ch3Dokument72 Seiten604 ch3Hazel Grace SantosNoch keine Bewertungen

- Bandhan PDFDokument19 SeitenBandhan PDFSonalika SharmaNoch keine Bewertungen

- Banksters Gangsters Traitors V3Dokument188 SeitenBanksters Gangsters Traitors V3John@spiritusNoch keine Bewertungen

- Challenge Prof Ed 3 Code of Ethics For Professional TeachersDokument3 SeitenChallenge Prof Ed 3 Code of Ethics For Professional TeachersDiane RomeroNoch keine Bewertungen

- Mysore Civil CodeDokument423 SeitenMysore Civil CodeUmesh Hb100% (2)

- Gabionza v. CADokument3 SeitenGabionza v. CAIan Joshua RomasantaNoch keine Bewertungen

- CASE DIGESTS - PledgeDokument10 SeitenCASE DIGESTS - PledgeAnonymous b4ycWuoIcNoch keine Bewertungen

- QUIZ Vocabulary Task-14Dokument3 SeitenQUIZ Vocabulary Task-14Syahwa RamadhanNoch keine Bewertungen

- Working Capital Management Exercise 3Dokument2 SeitenWorking Capital Management Exercise 3Nikki San GabrielNoch keine Bewertungen

- Neo Checklist For Credit InvestigatorDokument2 SeitenNeo Checklist For Credit Investigatorjandy salazarNoch keine Bewertungen

- Notes Cfa Fixed Income R42Dokument30 SeitenNotes Cfa Fixed Income R42Ayah AkNoch keine Bewertungen

- Module 3 - Borrowing CostsDokument3 SeitenModule 3 - Borrowing CostsLui100% (1)

- Bank of New Zealand - V - Geddes HC Auckland CIV (2008) 404-8082Dokument14 SeitenBank of New Zealand - V - Geddes HC Auckland CIV (2008) 404-8082Neil McCannNoch keine Bewertungen

- 10000000016Dokument246 Seiten10000000016Chapter 11 DocketsNoch keine Bewertungen

- Melendrez V Decena AC No 2104Dokument6 SeitenMelendrez V Decena AC No 2104Elena TanNoch keine Bewertungen

- OLC Chapter 02Dokument42 SeitenOLC Chapter 02Satarupa MukherjeeNoch keine Bewertungen

- SBA Resource GuideDokument52 SeitenSBA Resource Guideda5id665Noch keine Bewertungen

- Pre-Trial Brief DraftDokument2 SeitenPre-Trial Brief Draft0506sheltonNoch keine Bewertungen

- Low Interest Loan - Business Support For NYSC Graduates - BOIDokument5 SeitenLow Interest Loan - Business Support For NYSC Graduates - BOIsamuel olasupoNoch keine Bewertungen

- 4-CONSUMER CREDIT (PART 1) (Introduction To Consumer Credit)Dokument31 Seiten4-CONSUMER CREDIT (PART 1) (Introduction To Consumer Credit)Muhamad IhsanNoch keine Bewertungen

- Assignment 2 Tax 2 AgiDokument12 SeitenAssignment 2 Tax 2 Agiiknowu250Noch keine Bewertungen

- Gohil DharmadeepsinhDokument79 SeitenGohil DharmadeepsinhNikhil KapoorNoch keine Bewertungen

- Sumaiyya Jamadar Project 1Dokument31 SeitenSumaiyya Jamadar Project 1Shivrajanu123Noch keine Bewertungen

- Alvarez Vs Guingona - G.R. No. 118303. January 31, 1996Dokument8 SeitenAlvarez Vs Guingona - G.R. No. 118303. January 31, 1996Ebbe DyNoch keine Bewertungen

- A Study On South Indain Bank LTDDokument67 SeitenA Study On South Indain Bank LTDKarthik Ravi67% (3)

- Land Bank of The Philippines VS OngDokument13 SeitenLand Bank of The Philippines VS Ongjojo50166Noch keine Bewertungen