Das könnte Ihnen auch gefallen

- Standard Articles of AssociationDokument25 SeitenStandard Articles of AssociationVainess S Zulu0% (1)

- Company Regulation SampleDokument13 SeitenCompany Regulation SampleJames Oludele Etu67% (3)

- Samridhi Foundation Draft AoaDokument10 SeitenSamridhi Foundation Draft AoaPawan KumarNoch keine Bewertungen

- Article of AssociationDokument19 SeitenArticle of AssociationDhruvraj SolankiNoch keine Bewertungen

- Mercado, Floriemae S. BSA 2 Exercise 10Dokument6 SeitenMercado, Floriemae S. BSA 2 Exercise 10Floriemae MercadoNoch keine Bewertungen

- M&A SampleA-eDokument25 SeitenM&A SampleA-edearyatuNoch keine Bewertungen

- The Companies Act, 1956Dokument14 SeitenThe Companies Act, 1956C A Sumit DasNoch keine Bewertungen

- 4TH ScheduleDokument11 Seiten4TH ScheduleNURUL MASTURA BINTI KHAIRUDDIN (MOF)Noch keine Bewertungen

- Memorandum Articles of Association DummyDokument10 SeitenMemorandum Articles of Association DummyMuneeb HanifNoch keine Bewertungen

- Articles of AssociationDokument17 SeitenArticles of AssociationMohamad Khairul DaimNoch keine Bewertungen

- Checklist ESOPDokument24 SeitenChecklist ESOPKnowledge GuruNoch keine Bewertungen

- Provisions of ESOP in Companies ActDokument6 SeitenProvisions of ESOP in Companies ActshanikaNoch keine Bewertungen

- CDC LawDokument8 SeitenCDC LawNawazNoch keine Bewertungen

- Articles of Association of - Private LimitedDokument10 SeitenArticles of Association of - Private LimitedSatish V MadalaNoch keine Bewertungen

- Aoa OpcDokument6 SeitenAoa OpcjatinchopracoNoch keine Bewertungen

- Articles of AssociationDokument24 SeitenArticles of AssociationChidananda SwaroopNoch keine Bewertungen

- Securities and Exchange Board of India (Share Based Employee Benefits) Regulations, 2014Dokument19 SeitenSecurities and Exchange Board of India (Share Based Employee Benefits) Regulations, 2014Shyam SunderNoch keine Bewertungen

- Aoa OpcDokument6 SeitenAoa OpcJacinth JoseNoch keine Bewertungen

- The Companies Act 1956: Memorandum and Articles of Association OFDokument15 SeitenThe Companies Act 1956: Memorandum and Articles of Association OFSudhakar P M StriverNoch keine Bewertungen

- Articles of AssociationDokument11 SeitenArticles of AssociationxoxoxNoch keine Bewertungen

- Articles of Association (AOA) - (1) 2008Dokument24 SeitenArticles of Association (AOA) - (1) 2008theretailreachNoch keine Bewertungen

- The Companies Act, 1956 (Private Company Limited by Shares) : Articles of Association of Dsiidc Exim LimitedDokument16 SeitenThe Companies Act, 1956 (Private Company Limited by Shares) : Articles of Association of Dsiidc Exim LimitedArunkumarNoch keine Bewertungen

- Sample Memorandum PDFDokument16 SeitenSample Memorandum PDFsuresh6265Noch keine Bewertungen

- Wa0004.Dokument15 SeitenWa0004.Ýøgësh ÑäyãkNoch keine Bewertungen

- Share Option PlanDokument13 SeitenShare Option PlanAllan HenryNoch keine Bewertungen

- Checklist For Issue of ESOP by Private CompanyDokument18 SeitenChecklist For Issue of ESOP by Private Companyaslam shaNoch keine Bewertungen

- Brief of EsopsDokument3 SeitenBrief of EsopsIshita MisraNoch keine Bewertungen

- Preference Redeemable SharesDokument14 SeitenPreference Redeemable SharesColin TanNoch keine Bewertungen

- Redemption of Preference SharesDokument8 SeitenRedemption of Preference SharesAyush BhavsarNoch keine Bewertungen

- Articles of Association As Per New Companies Act 2013Dokument14 SeitenArticles of Association As Per New Companies Act 2013greeshmaNoch keine Bewertungen

- GCC&BA SUPR Share-Capital-1 Sushita-Chakraborty UG (R1)Dokument14 SeitenGCC&BA SUPR Share-Capital-1 Sushita-Chakraborty UG (R1)aman sainiNoch keine Bewertungen

- Corporation Sec.75 85Dokument37 SeitenCorporation Sec.75 85iseonggyeong302Noch keine Bewertungen

- Companies Act - SchedulesDokument25 SeitenCompanies Act - SchedulesTracey HighlyFavouredNoch keine Bewertungen

- Lecture - 6 - Certificate of Shares and Other Securities - 71-83Dokument8 SeitenLecture - 6 - Certificate of Shares and Other Securities - 71-83Ahsan RazaNoch keine Bewertungen

- Article of Association KvellDokument11 SeitenArticle of Association KvellCA Sudhanshu JoshiNoch keine Bewertungen

- Allotment of Shares, Share & Share CapitalDokument9 SeitenAllotment of Shares, Share & Share Capitalkavya.aroraNoch keine Bewertungen

- Spic AOA: Table F - Articles of Association of Acompany Limited by SharesDokument8 SeitenSpic AOA: Table F - Articles of Association of Acompany Limited by SharesshivamNoch keine Bewertungen

- Aoa Josoft TechnologiesDokument15 SeitenAoa Josoft TechnologiesPc RajasekharNoch keine Bewertungen

- AOA Pragya ReadableDokument12 SeitenAOA Pragya Readablerajesh KumarNoch keine Bewertungen

- Sebi Sbeb 2014Dokument29 SeitenSebi Sbeb 2014jayesh khatriNoch keine Bewertungen

- Adoption of New Set of Articles of Association (Company Update)Dokument21 SeitenAdoption of New Set of Articles of Association (Company Update)Shyam SunderNoch keine Bewertungen

- Securities Market InstrumentsDokument8 SeitenSecurities Market InstrumentsBRIJESHA MOHANTYNoch keine Bewertungen

- Equity Incentive PlanDokument3 SeitenEquity Incentive PlanRocketLawyer100% (2)

- Share Capital PDFDokument6 SeitenShare Capital PDFKajal MattuNoch keine Bewertungen

- Part 6 - Share Capital and DebenturesDokument6 SeitenPart 6 - Share Capital and Debentures8928Noch keine Bewertungen

- 3.issue of Shares Various Regulations Relating To Issue of Various Shares - Sushita Chakraborty - UGDokument7 Seiten3.issue of Shares Various Regulations Relating To Issue of Various Shares - Sushita Chakraborty - UGSyed aliNoch keine Bewertungen

- Lesson 3 CLOSE CORPORATIONS DISCUSSION OUTLINEDokument11 SeitenLesson 3 CLOSE CORPORATIONS DISCUSSION OUTLINEVanessa Evans CruzNoch keine Bewertungen

- Galgotias University: Bba+Llb (Hons) Section-B Semester-VthDokument11 SeitenGalgotias University: Bba+Llb (Hons) Section-B Semester-VthTannu guptaNoch keine Bewertungen

- 19 Oct Corp ClassDokument117 Seiten19 Oct Corp ClassNichole LanuzaNoch keine Bewertungen

- Private Company Limited by Shares Regulations FormDokument17 SeitenPrivate Company Limited by Shares Regulations FormGerard 'Rockefeller' YitamkeyNoch keine Bewertungen

- RSR AOA FinalDokument18 SeitenRSR AOA Finaladesh_naharNoch keine Bewertungen

- SEBI ESOP Regulations 1492522977714Dokument20 SeitenSEBI ESOP Regulations 1492522977714MohitNoch keine Bewertungen

- Merger and ConsolidationDokument3 SeitenMerger and ConsolidationJohanna Raissa CapadaNoch keine Bewertungen

- The Corporation Code of The Philippines Section 6. Classification of SharesDokument4 SeitenThe Corporation Code of The Philippines Section 6. Classification of SharesLovely ZyrenjcNoch keine Bewertungen

- The Following Rules Regarding Allotment of Shares Are NotedDokument3 SeitenThe Following Rules Regarding Allotment of Shares Are NotedIshika AroraNoch keine Bewertungen

- Under The Companies Act, 1956Dokument17 SeitenUnder The Companies Act, 1956yamarthiNoch keine Bewertungen

- Founders Vesting AgreementDokument9 SeitenFounders Vesting AgreementTristan KoNoch keine Bewertungen

- What You Must Know About Incorporate a Company in IndiaVon EverandWhat You Must Know About Incorporate a Company in IndiaNoch keine Bewertungen

- Registration of Charges On Properties Acquired Subject To Charge.Dokument13 SeitenRegistration of Charges On Properties Acquired Subject To Charge.rhnthrNoch keine Bewertungen

- Lecture - 6 Power of Companies To Purchase Its Own Shares (Sec. 95A)Dokument8 SeitenLecture - 6 Power of Companies To Purchase Its Own Shares (Sec. 95A)rhnthrNoch keine Bewertungen

- Lecture - 4 - Amended (Section 62-68, 70-73)Dokument8 SeitenLecture - 4 - Amended (Section 62-68, 70-73)rhnthrNoch keine Bewertungen

- Lecture - 3Dokument2 SeitenLecture - 3rhnthrNoch keine Bewertungen

- Winding Up - CompleteDokument98 SeitenWinding Up - Completehabib1912Noch keine Bewertungen

- Winding Up - CompleteDokument98 SeitenWinding Up - Completehabib1912Noch keine Bewertungen

- Tobin, J. (1987) Financial IntermediariesDokument14 SeitenTobin, J. (1987) Financial IntermediariesClaudia PalaciosNoch keine Bewertungen

- Tutorial 11 AnswersDokument3 SeitenTutorial 11 AnswershrfjbjrfrfNoch keine Bewertungen

- OneStop ReportDokument52 SeitenOneStop ReportArindam SardarNoch keine Bewertungen

- UMS Holdings LTD - 2Q23 - Results Below Expectation But Optimistic Outlook Ahead Upgrade To BUYDokument5 SeitenUMS Holdings LTD - 2Q23 - Results Below Expectation But Optimistic Outlook Ahead Upgrade To BUYtanmabel16Noch keine Bewertungen

- Uid46434 UCCD Financial Accounting Question PaperDokument7 SeitenUid46434 UCCD Financial Accounting Question PaperPhoenixFirebrdNoch keine Bewertungen

- EDP by Gowtham Kumar C.K PDFDokument84 SeitenEDP by Gowtham Kumar C.K PDFDeepthi Gowda100% (3)

- Different Kinds of ObligationDokument7 SeitenDifferent Kinds of ObligationLimVianesse100% (3)

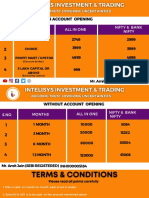

- Intelisys Pricing PlanDokument5 SeitenIntelisys Pricing PlanregsNoch keine Bewertungen

- 2013 Product Guide and Calendar FX ProductsDokument135 Seiten2013 Product Guide and Calendar FX ProductsThomas KimNoch keine Bewertungen

- Book of Hull - Week 1Dokument6 SeitenBook of Hull - Week 1zamunda0809Noch keine Bewertungen

- CH 4 4-35 SpreadsheetDokument34 SeitenCH 4 4-35 Spreadsheetcherishwisdom_997598Noch keine Bewertungen

- Fong v. DueñasDokument3 SeitenFong v. DueñasGia DimayugaNoch keine Bewertungen

- 12 Accountancy Lyp 2015 Foreign Set1Dokument42 Seiten12 Accountancy Lyp 2015 Foreign Set1Ashish GangwalNoch keine Bewertungen

- Perimeter Wall 4 Sec 4 BQ Combined PDFDokument65 SeitenPerimeter Wall 4 Sec 4 BQ Combined PDFNeil AngNoch keine Bewertungen

- Pert 5 - Hedge Net Invest and Embeded Derivatives - PostDokument26 SeitenPert 5 - Hedge Net Invest and Embeded Derivatives - PostSwanbellyNoch keine Bewertungen

- (Reviewer - Midterm GoSalTo) Tax 2 PDFDokument38 Seiten(Reviewer - Midterm GoSalTo) Tax 2 PDFHoreb Felix VillaNoch keine Bewertungen

- Economics AssignmentDokument8 SeitenEconomics Assignmentchandanprakash30Noch keine Bewertungen

- SHA Broker Update Form - October 2015Dokument1 SeiteSHA Broker Update Form - October 2015henrydeeNoch keine Bewertungen

- NBFCDokument7 SeitenNBFCRaktima MajumdarNoch keine Bewertungen

- P 17-1 Cash Distribution Plan and Entries - Installment: RequiredDokument5 SeitenP 17-1 Cash Distribution Plan and Entries - Installment: RequiredGhitha Afifah HurinNoch keine Bewertungen

- Reyes v. BancomDokument8 SeitenReyes v. BancomMarie Nickie BolosNoch keine Bewertungen

- SWAPsDokument41 SeitenSWAPsFranklin XavierNoch keine Bewertungen

- Week 2 - The Battle For Value, 2004 QuestionsDokument2 SeitenWeek 2 - The Battle For Value, 2004 QuestionsLucasNoch keine Bewertungen

- 9381 - Soal Uas Akl 2Dokument14 Seiten9381 - Soal Uas Akl 2Kurnia Purnama Ayu0% (3)

- Platts Pe 24 June 2015Dokument12 SeitenPlatts Pe 24 June 2015mcontrerjNoch keine Bewertungen

- 018.ASX IAW Feb 1 2008 Appendix 4C QuarterlyDokument10 Seiten018.ASX IAW Feb 1 2008 Appendix 4C QuarterlyASX:ILH (ILH Group)Noch keine Bewertungen

- BajajcorpDokument317 SeitenBajajcorpPrabha ChelladuraiNoch keine Bewertungen

- Saudi Real Estate SectorDokument14 SeitenSaudi Real Estate SectorJitendra Garg100% (4)

- SM Chapter 13Dokument52 SeitenSM Chapter 13ginish120% (1)

- Religious Freedom Non Impairment of ContractsDokument4 SeitenReligious Freedom Non Impairment of ContractsJean Jamailah Tomugdan100% (1)