Das könnte Ihnen auch gefallen

- Linda Wall Wins Over IRSDokument12 SeitenLinda Wall Wins Over IRSJeff Anderson89% (9)

- Lawfully Yours: The Realm of Business, Government and LawVon EverandLawfully Yours: The Realm of Business, Government and LawNoch keine Bewertungen

- The Ten Commandments Vs Injunctive and Declaratory JudgementsVon EverandThe Ten Commandments Vs Injunctive and Declaratory JudgementsNoch keine Bewertungen

- w4 Voluntary 1Dokument1 Seitew4 Voluntary 1crazybuttful100% (2)

- Challenge IRS AuthorityDokument6 SeitenChallenge IRS AuthorityJeff Anderson91% (11)

- IRS Exposed: IRS Is A Privately Owned Puerto Rican Trust.: 1. IRS Identity & Principal of InterestDokument22 SeitenIRS Exposed: IRS Is A Privately Owned Puerto Rican Trust.: 1. IRS Identity & Principal of InterestJoshua Sygnal GutierrezNoch keine Bewertungen

- w4 VoluntaryDokument1 Seitew4 Voluntarycrazybuttful100% (1)

- Stop The IrsDokument8 SeitenStop The IrsLuis Ewing50% (6)

- 05-29-2011 Rod Class Navy LetterDokument7 Seiten05-29-2011 Rod Class Navy Letterrodclassteam100% (1)

- DMV CVC CafvDokument5 SeitenDMV CVC Cafvtube204Noch keine Bewertungen

- CP-22E IRS Response LetterDokument4 SeitenCP-22E IRS Response LetterTRISTARUSA100% (2)

- Affidavit Lieber PatrickDokument6 SeitenAffidavit Lieber PatrickPatrick Long100% (1)

- Wiping Out Fraudulent LiensDokument2 SeitenWiping Out Fraudulent LiensAnonymous EKGJIpGwPjNoch keine Bewertungen

- Facts About The Income TaxDokument11 SeitenFacts About The Income TaxAnonymous nYwWYS3ntVNoch keine Bewertungen

- How I Fought A Property Tax ForeclosureDokument48 SeitenHow I Fought A Property Tax Foreclosureapi-19731109100% (8)

- Lien RemovalDokument3 SeitenLien Removalspcbanking100% (3)

- 112Dokument21 Seiten112Fuckoff100% (1)

- Free Right of Travel Ticket Killer - PHPDokument2 SeitenFree Right of Travel Ticket Killer - PHPEl-Seti Anu Ali El100% (1)

- 02 Irs CafvDokument8 Seiten02 Irs CafvReginald Ringgold100% (1)

- Police Charged With Theft of Towed AutomobilesDokument2 SeitenPolice Charged With Theft of Towed AutomobilesEl-Seti Anu Ali El100% (2)

- Criminal ComplaintDokument11 SeitenCriminal ComplaintCrystalhengeNoch keine Bewertungen

- 2nd Notice W-4 TerminationDokument2 Seiten2nd Notice W-4 TerminationMichael Kovach100% (4)

- IRS or IR Debt CollectorDokument28 SeitenIRS or IR Debt CollectorWillAsher100% (7)

- Affidavit of Fact IRSDokument13 SeitenAffidavit of Fact IRS123pratus89% (9)

- FORECLOSE ON THE FRAUDSTERS - PUT BANK OF AMERICA IN RECEIVERSHIP - White Collar Expert Calls For FDIC To Take Control of BofADokument8 SeitenFORECLOSE ON THE FRAUDSTERS - PUT BANK OF AMERICA IN RECEIVERSHIP - White Collar Expert Calls For FDIC To Take Control of BofA83jjmack100% (2)

- 2-A-Notice of Fault-Oppurtunity To CureDokument4 Seiten2-A-Notice of Fault-Oppurtunity To CureEmpressInI100% (1)

- IRS Rescission of SignatureDokument23 SeitenIRS Rescission of SignaturePaulStaples100% (12)

- DMV Cites No Registration PDFDokument21 SeitenDMV Cites No Registration PDF1 watchman100% (3)

- Social Security Numbers Can Only Be Issued To Federal - EmployeesDokument1 SeiteSocial Security Numbers Can Only Be Issued To Federal - EmployeesAlbertoNoch keine Bewertungen

- CALIF FrivolousResponseDokument9 SeitenCALIF FrivolousResponseexousiallc100% (1)

- Consumer Goods NoticeDokument3 SeitenConsumer Goods NoticeGee Penn100% (1)

- Irs QuestionsDokument7 SeitenIrs Questionsfisherre2000Noch keine Bewertungen

- The FraternityDokument3 SeitenThe Fraternitybriansolution100% (1)

- Notice & Warning To Utility CompaniesDokument2 SeitenNotice & Warning To Utility Companiesrodclassteam92% (13)

- Affidavit - Writ of Right v15Dokument6 SeitenAffidavit - Writ of Right v15iamsomedude100% (7)

- 4 9 10 Rod Class Coast Guard FilingDokument33 Seiten4 9 10 Rod Class Coast Guard FilingjoerocketmanNoch keine Bewertungen

- 01 Introduction To Administrative RemedyDokument3 Seiten01 Introduction To Administrative Remedyajinxa100% (2)

- Title 31 Section 742 Fraud ExplainedDokument36 SeitenTitle 31 Section 742 Fraud Explainedsabiont90% (10)

- U.S. Supreme Court-IRS Case-IRS in Default-All-documents Thru-Motion For ORDERDokument104 SeitenU.S. Supreme Court-IRS Case-IRS in Default-All-documents Thru-Motion For ORDERJeff Maehr100% (3)

- 40 Well Kept Secrets of Bar AttorneysDokument2 Seiten40 Well Kept Secrets of Bar Attorneysjoe100% (3)

- Letter To PostmasterDokument2 SeitenLetter To PostmasterNotarysTo Go100% (3)

- Bombshell - Rod Class Gets FOURTH Administrative Ruling Government Offices Are Vacant - All Government Officials Are Private Contractors Public Notice/Public RecordDokument4 SeitenBombshell - Rod Class Gets FOURTH Administrative Ruling Government Offices Are Vacant - All Government Officials Are Private Contractors Public Notice/Public Recordin1or100% (4)

- How To Stop Employers From Withholding Income TaxesDokument14 SeitenHow To Stop Employers From Withholding Income TaxesSaleem Alhakim90% (10)

- Jeffrey T Maehr V Internal Revenue Service US Supreme Court SDokument89 SeitenJeffrey T Maehr V Internal Revenue Service US Supreme Court SJeff MaehrNoch keine Bewertungen

- 31 USC Sec. 3124 FROM 31 U.S. CODE Section 742Dokument12 Seiten31 USC Sec. 3124 FROM 31 U.S. CODE Section 742sabiont100% (5)

- How - To - Kill - The - SSN - Doc - 0.odt Filename - UTF-8 - How+to+Kill+the+SSN - Doc - 0Dokument16 SeitenHow - To - Kill - The - SSN - Doc - 0.odt Filename - UTF-8 - How+to+Kill+the+SSN - Doc - 0NotarysTo Go0% (1)

- Memorandum in Support of Affidavit 1Dokument1 SeiteMemorandum in Support of Affidavit 1rodclassteamNoch keine Bewertungen

- 11 7286230909Dokument13 Seiten11 7286230909Joshua Sygnal Gutierrez100% (2)

- Notice and Warning To Utility CompaniesDokument3 SeitenNotice and Warning To Utility CompaniesJuan Carlos Asporosa Vallecillo85% (13)

- Clerk - Notice To County ClerkDokument1 SeiteClerk - Notice To County ClerkMichael Kovach100% (2)

- 31 Questions and Answers About The Internal Revenue ServiceDokument29 Seiten31 Questions and Answers About The Internal Revenue ServiceAlberto100% (2)

- IRS A Private For Profit Foreign Corporation Find Attached IRS Certificate of Incorporation Plus List of Private For Profit Foreign CorporationsDokument10 SeitenIRS A Private For Profit Foreign Corporation Find Attached IRS Certificate of Incorporation Plus List of Private For Profit Foreign Corporationsg100% (1)

- Steps To Terminate IRS 668 Notice of LienDokument10 SeitenSteps To Terminate IRS 668 Notice of Lienrhouse_1100% (3)

- UCC 1 108 Relation To Electronic SignaturesDokument1 SeiteUCC 1 108 Relation To Electronic Signaturespouhka100% (1)

- Cover Letter Cease and Desist Abusive Collection IRS ScrubbedDokument2 SeitenCover Letter Cease and Desist Abusive Collection IRS ScrubbedMark AustinNoch keine Bewertungen

- 26cfr31.3121e1 Why You Are Likely Not A U.S. Citizen.Dokument1 Seite26cfr31.3121e1 Why You Are Likely Not A U.S. Citizen.Title IV-D Man with a planNoch keine Bewertungen

- Private Attorney General PAGA-09Dokument5 SeitenPrivate Attorney General PAGA-09Truth Press MediaNoch keine Bewertungen

- FreeDokument156 SeitenFreeSnowdenKonanNoch keine Bewertungen

- Affidavit of Truth of Citizenship StatusDokument7 SeitenAffidavit of Truth of Citizenship StatusSnowdenKonan100% (4)

- Chapter 1-Electrical Theory: (Essential For Journeyman and Master/ Contractor Licensing Exams)Dokument5 SeitenChapter 1-Electrical Theory: (Essential For Journeyman and Master/ Contractor Licensing Exams)SnowdenKonanNoch keine Bewertungen

- 2022 - Texas Motion To Quash Indictment - AltDokument3 Seiten2022 - Texas Motion To Quash Indictment - AltSnowdenKonanNoch keine Bewertungen

- Zip Code LetterDokument1 SeiteZip Code LetterSnowdenKonanNoch keine Bewertungen

- Paying Off DebtDokument12 SeitenPaying Off DebtSnowdenKonanNoch keine Bewertungen

- Great Britain Owns USADokument7 SeitenGreat Britain Owns USAplayboi501100% (5)

- 1 A Short History On Connection To The Philippines and TaxationDokument4 Seiten1 A Short History On Connection To The Philippines and TaxationSnowdenKonanNoch keine Bewertungen

- Affidavit Usufructory Military RuleDokument4 SeitenAffidavit Usufructory Military Ruleapi-247852575100% (4)

- 1895 Eighth Grade Final ExamDokument5 Seiten1895 Eighth Grade Final ExamSnowdenKonan100% (1)

- Personal Financial StatementDokument2 SeitenPersonal Financial StatementSnowdenKonanNoch keine Bewertungen

- 5.2d - Successor TrusteeDokument2 Seiten5.2d - Successor TrusteeSnowdenKonan50% (2)

- Modification or Discharge of Debt in A Chapter 9 CaseDokument13 SeitenModification or Discharge of Debt in A Chapter 9 CaseSnowdenKonanNoch keine Bewertungen

- Insured's Name and Address Re: Insured's Name - Name of Claimant(s) - Policy No. - Court Cause No.Dokument3 SeitenInsured's Name and Address Re: Insured's Name - Name of Claimant(s) - Policy No. - Court Cause No.SnowdenKonanNoch keine Bewertungen

- Us 01648BGDokument4 SeitenUs 01648BGSnowdenKonanNoch keine Bewertungen

- North Richland Hills City CharterDokument50 SeitenNorth Richland Hills City CharterSnowdenKonanNoch keine Bewertungen

- Subject: RE: TRAFFIC TICKET SCAM: Washington, DC Earns $179 Million A Year FromDokument12 SeitenSubject: RE: TRAFFIC TICKET SCAM: Washington, DC Earns $179 Million A Year FromSnowdenKonan100% (1)

- Postal Treaty of Light Earth DNA LodialDokument33 SeitenPostal Treaty of Light Earth DNA LodialSnowdenKonan100% (22)

- Commercial LessonDokument8 SeitenCommercial LessonSnowdenKonan100% (1)

- Termination of TrusteeDokument1 SeiteTermination of TrusteeSnowdenKonanNoch keine Bewertungen

- TITLE 4: U.-S.-W.: CODES: CHAPTER 1: 1 2. FOR THE FLAG: CONTRACT-STATES-CORPORATION-VESSEL. Copyclaim - 25 - August - 1989 $1.00 U.S. StampDokument2 SeitenTITLE 4: U.-S.-W.: CODES: CHAPTER 1: 1 2. FOR THE FLAG: CONTRACT-STATES-CORPORATION-VESSEL. Copyclaim - 25 - August - 1989 $1.00 U.S. StampSnowdenKonan100% (1)

- 1 A Short History On Connection To The Philippines and TaxationDokument4 Seiten1 A Short History On Connection To The Philippines and TaxationSnowdenKonanNoch keine Bewertungen

- CHAPTER 6 - PAYROLL SCHEMES - Principles of Fraud Examination, 4th EditionDokument17 SeitenCHAPTER 6 - PAYROLL SCHEMES - Principles of Fraud Examination, 4th Editionscribd20014Noch keine Bewertungen

- Lenovo Company, Mis AssingmentDokument20 SeitenLenovo Company, Mis AssingmentNarendra RaoNoch keine Bewertungen

- The Withholding Tax SystemDokument191 SeitenThe Withholding Tax SystemDa Yani ChristeeneNoch keine Bewertungen

- Introduction To E-Commerce and ERP LabDokument18 SeitenIntroduction To E-Commerce and ERP LabYogesh SharmaNoch keine Bewertungen

- Internal Auditor As Fraud BusterDokument12 SeitenInternal Auditor As Fraud BusterpalashndcNoch keine Bewertungen

- TGS - CM - Absentee Payroll Onboarding Guide - v11.0Dokument32 SeitenTGS - CM - Absentee Payroll Onboarding Guide - v11.0Radhika RadhikagNoch keine Bewertungen

- Best Practices in Creating A Strategic Finance Function: Sap InsightDokument16 SeitenBest Practices in Creating A Strategic Finance Function: Sap Insightaramaky2001Noch keine Bewertungen

- CVDokument7 SeitenCVNur MohdNoch keine Bewertungen

- E-Commerce:: E-Business Is The Use of The Internet and Other Networks andDokument13 SeitenE-Commerce:: E-Business Is The Use of The Internet and Other Networks andImroz MahmudNoch keine Bewertungen

- Fast FormulasDokument185 SeitenFast FormulasMurali KrishnaNoch keine Bewertungen

- AIS-1 - Module On Topic 2Dokument8 SeitenAIS-1 - Module On Topic 2MiaNoch keine Bewertungen

- Rais12 SM CH03Dokument46 SeitenRais12 SM CH03Maliha JahanNoch keine Bewertungen

- Sample Resume CHRMPDokument5 SeitenSample Resume CHRMPajshri23Noch keine Bewertungen

- FUSION HCM - Using Time and Labor With Global PayrollDokument26 SeitenFUSION HCM - Using Time and Labor With Global PayrollAravind Alavanthar0% (1)

- Housekeeping Supervisors)Dokument4 SeitenHousekeeping Supervisors)aliNoch keine Bewertungen

- CAF-9 Mock (Q.P)Dokument5 SeitenCAF-9 Mock (Q.P)manadish nawazNoch keine Bewertungen

- Top Ten QuickBooks Tips and TricksDokument52 SeitenTop Ten QuickBooks Tips and Tricksjaalcivar100% (2)

- Computerized Payroll System Thesis 2010Dokument5 SeitenComputerized Payroll System Thesis 2010jamieboydreno100% (2)

- Summative Test (BusMath)Dokument1 SeiteSummative Test (BusMath)Fatima Elsan OrillanNoch keine Bewertungen

- Ebook Business Math 9Th Edition Cleaves Test Bank Full Chapter PDFDokument65 SeitenEbook Business Math 9Th Edition Cleaves Test Bank Full Chapter PDFjaydenur3jones100% (15)

- Wage Type Request Form Overview 102011vs2Dokument2 SeitenWage Type Request Form Overview 102011vs2Singh 10Noch keine Bewertungen

- GBusiSBG11 PDFDokument168 SeitenGBusiSBG11 PDFkemime100% (2)

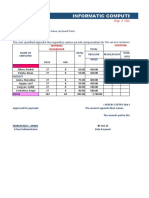

- Payroll: Informatic Computer Institute of Agusan Del SurDokument4 SeitenPayroll: Informatic Computer Institute of Agusan Del SurJulius SalasNoch keine Bewertungen

- Chapter 10-Compensation Income: True or FalseDokument15 SeitenChapter 10-Compensation Income: True or FalseJarren Basilan57% (7)

- Assignment 1 Csc508 Data Structure From Class: CSC2534A Lecturer: Anis Amilah Binti ShariDokument22 SeitenAssignment 1 Csc508 Data Structure From Class: CSC2534A Lecturer: Anis Amilah Binti ShariMUHAMMAD SHADAMIER EMRANNoch keine Bewertungen

- SLF103 ApplicationRefundExcessOverpaymentSTL V02Dokument1 SeiteSLF103 ApplicationRefundExcessOverpaymentSTL V02Al Jardeliza Aspera100% (1)

- RRL With References RhodaDokument3 SeitenRRL With References Rhodad dwdf100% (3)

- Organizational Polices & Procedures Sourounding The Preparation of Tax ReturnsDokument18 SeitenOrganizational Polices & Procedures Sourounding The Preparation of Tax ReturnsStephen PommellsNoch keine Bewertungen

- Better Work, Better LifeDokument15 SeitenBetter Work, Better LifeparuljainibmrNoch keine Bewertungen

- Hayden Kho Sr. Vs Dolores Nagbanua, Et. Al. G.R. No. 237246. July 29, 2019Dokument10 SeitenHayden Kho Sr. Vs Dolores Nagbanua, Et. Al. G.R. No. 237246. July 29, 2019Mysh PDNoch keine Bewertungen