Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

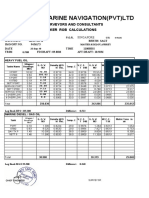

- SerargaegDokument2 SeitenSerargaegArief HidayatNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Company IIDokument1 SeiteCompany IIArief HidayatNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Manual Pvelite 2014 Egpet - Penelusuran GoogleDokument2 SeitenManual Pvelite 2014 Egpet - Penelusuran GoogleArief HidayatNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Department Production: Pt. Showa Esterindo IndonesiaDokument1 SeiteDepartment Production: Pt. Showa Esterindo IndonesiaArief HidayatNoch keine Bewertungen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Ingatlah Pada DirimuDokument6 SeitenIngatlah Pada DirimuArief HidayatNoch keine Bewertungen

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Person in Charge For C-121 UnitDokument1 SeitePerson in Charge For C-121 UnitArief HidayatNoch keine Bewertungen

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Pump & Mechanical SealsDokument41 SeitenPump & Mechanical SealsArief Hidayat100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Furnace Flooding, 011107Dokument11 SeitenFurnace Flooding, 011107Arief HidayatNoch keine Bewertungen

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Daftar Pustaka: Chem 18 (4) : 1515-1521Dokument4 SeitenDaftar Pustaka: Chem 18 (4) : 1515-1521dhiyaulNoch keine Bewertungen

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Water Fueled CarDokument12 SeitenWater Fueled CarVenkata Harish Yadavalli100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- 2.3 Fuels: Camarines Norte State CollegeDokument17 Seiten2.3 Fuels: Camarines Norte State CollegeAnsley San Juan DelvalleNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- D910 Aviation FuelDokument8 SeitenD910 Aviation Fuelamhd4806Noch keine Bewertungen

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- WLTP-06-18-rev1e - Proposal On Density NMHC by ACEADokument8 SeitenWLTP-06-18-rev1e - Proposal On Density NMHC by ACEAAlbert StratingNoch keine Bewertungen

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- 4 Carbonization of CoalDokument24 Seiten4 Carbonization of Coalraja.mt100% (4)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Manhour NSRPDokument10 SeitenManhour NSRPvazzoleralex6884Noch keine Bewertungen

- Energy Sector: Training Materials For National Greenhouse Gas InventoriesDokument40 SeitenEnergy Sector: Training Materials For National Greenhouse Gas InventoriesRatan GamitNoch keine Bewertungen

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Studi Penentuan Peringkat Batubara Berdasarkan Analisa Fisika Dan Kimia Di Daerah Air Laya Dan Mangunjaya Provinsi Sumatera SelatanDokument7 SeitenStudi Penentuan Peringkat Batubara Berdasarkan Analisa Fisika Dan Kimia Di Daerah Air Laya Dan Mangunjaya Provinsi Sumatera SelatanPanji NovendraNoch keine Bewertungen

- 1004003R4-OM-EnG-International Hopper Cooled 1.5 To 2.5 and 3 To 5 H.P LB EngineDokument56 Seiten1004003R4-OM-EnG-International Hopper Cooled 1.5 To 2.5 and 3 To 5 H.P LB EngineVìctorMqzNoch keine Bewertungen

- Annualmerged CompressedDokument480 SeitenAnnualmerged CompressedKanan kumar DasNoch keine Bewertungen

- AV Gas Brochure 7CCDokument4 SeitenAV Gas Brochure 7CCQuality Manager Jet ServeNoch keine Bewertungen

- Bunker CalculationDokument10 SeitenBunker CalculationNimesh PereraNoch keine Bewertungen

- Industrial Chemistry II Module Chem451 Finasubmitted 1 1Dokument206 SeitenIndustrial Chemistry II Module Chem451 Finasubmitted 1 1tesfayeNoch keine Bewertungen

- Cruise Control, CVT and Shift Indicator, Engine ControlDokument25 SeitenCruise Control, CVT and Shift Indicator, Engine ControlNhật Đặng100% (1)

- EN-1207-302 - Simulation of Syngas Production Through Plasma Gasification From Indonesia's Low-Grade Coal As A New EnergyDokument10 SeitenEN-1207-302 - Simulation of Syngas Production Through Plasma Gasification From Indonesia's Low-Grade Coal As A New EnergypsesotyoNoch keine Bewertungen

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Introduction To BIODIESELDokument4 SeitenIntroduction To BIODIESELdumi-dumiNoch keine Bewertungen

- Anais Bbcbrazil 2018Dokument339 SeitenAnais Bbcbrazil 2018Thiago LimaNoch keine Bewertungen

- Kaj Portin - Wartsila FinlandDokument11 SeitenKaj Portin - Wartsila FinlandSenthil KumarNoch keine Bewertungen

- Cetane Number: University of Karbala College of Engineering Third StageDokument7 SeitenCetane Number: University of Karbala College of Engineering Third StageMohamed ModerNoch keine Bewertungen

- Case Study in Industrial Plant EngineeringDokument4 SeitenCase Study in Industrial Plant Engineeringjhenalbano100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Renewable SourcesDokument15 SeitenRenewable SourcesSousaNoch keine Bewertungen

- Harga Batubara Acuan (Hba) & Harga Patokan Batubara (HPB) December 2019Dokument8 SeitenHarga Batubara Acuan (Hba) & Harga Patokan Batubara (HPB) December 2019Adnan NstNoch keine Bewertungen

- April-Distri Totachi Price Vis Min PL 2022Dokument1 SeiteApril-Distri Totachi Price Vis Min PL 2022Kelly TemewNoch keine Bewertungen

- Oil & Gas Industry ConversionsDokument9 SeitenOil & Gas Industry ConversionsWagus GinanjarNoch keine Bewertungen

- Mina Al FahalDokument2 SeitenMina Al Fahalmethyou777Noch keine Bewertungen

- My Mathematics School 2Dokument7 SeitenMy Mathematics School 2Kumar FongNoch keine Bewertungen

- Ministry of Education Secondary Engagement Programme Grade 11 ChemistryDokument4 SeitenMinistry of Education Secondary Engagement Programme Grade 11 ChemistryNikoli MajorNoch keine Bewertungen

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Fuels and ThermochemistryDokument40 SeitenFuels and ThermochemistryVineet Kumar SinghNoch keine Bewertungen

- Lay Out-Plot PlanDokument1 SeiteLay Out-Plot PlanHadiNoch keine Bewertungen