Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- MODULE 8 Closing and Reversing EntriesDokument5 SeitenMODULE 8 Closing and Reversing EntriesChristian Cyrous AcostaNoch keine Bewertungen

- Review QsDokument92 SeitenReview Qsfaiztheme67% (3)

- R28 Financial Analysis Techniques IFT Notes PDFDokument23 SeitenR28 Financial Analysis Techniques IFT Notes PDFNoor Salman83% (6)

- MR. Rosiak PerpetualDokument13 SeitenMR. Rosiak PerpetualSelfi Riani100% (2)

- Tugas 6 AKM1 Muhammad Alfarizi 142200278 EA-IDokument9 SeitenTugas 6 AKM1 Muhammad Alfarizi 142200278 EA-Imuhammad alfariziNoch keine Bewertungen

- T24 Accounting Introduction - R14.01Dokument165 SeitenT24 Accounting Introduction - R14.01JEGADEESWARINoch keine Bewertungen

- Tulip Me Qs 2021Dokument10 SeitenTulip Me Qs 2021Jacqueline Kanesha JamesNoch keine Bewertungen

- Advanced Accounting Baker Chapter 4 AnswersDokument58 SeitenAdvanced Accounting Baker Chapter 4 AnswersOksana McCord86% (7)

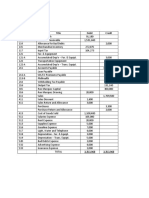

- Trial Balance February 28, 20X1Dokument3 SeitenTrial Balance February 28, 20X1Angelica MaeNoch keine Bewertungen

- Consolidation TheoryDokument22 SeitenConsolidation TheorySmruti RanjanNoch keine Bewertungen

- 2021 Full Year FinancialsDokument2 Seiten2021 Full Year FinancialsFuaad DodooNoch keine Bewertungen

- Chapter 9 ValuationDokument85 SeitenChapter 9 ValuationSaravanaaRajendran100% (1)

- Mas Chap 13Dokument23 SeitenMas Chap 13Raz MahariNoch keine Bewertungen

- Marginal Costing TYBAFDokument13 SeitenMarginal Costing TYBAFAkash BugadeNoch keine Bewertungen

- Job Profit Document 1Dokument2 SeitenJob Profit Document 1ZamurradNoch keine Bewertungen

- Fabm 1 Lesson 4-5Dokument32 SeitenFabm 1 Lesson 4-5Dionel RizoNoch keine Bewertungen

- Subs Testing Proc BBBDokument28 SeitenSubs Testing Proc BBBRosario Garcia CatugasNoch keine Bewertungen

- AE231Dokument6 SeitenAE231Mae-shane SagayoNoch keine Bewertungen

- Penerapan PSAK 73 - MaterialDokument77 SeitenPenerapan PSAK 73 - Materialni made safitriNoch keine Bewertungen

- Jad Payroll April 01-07 2022Dokument9 SeitenJad Payroll April 01-07 2022Jervie JalaNoch keine Bewertungen

- Transaction Analysis SarabiaDokument2 SeitenTransaction Analysis SarabiaJasmine Acta0% (1)

- Auditing and Ethics May 2024 1701670825Dokument6 SeitenAuditing and Ethics May 2024 1701670825Anil ReddyNoch keine Bewertungen

- 01 - Correction of ErrorsDokument4 Seiten01 - Correction of ErrorsMikaela SalvadorNoch keine Bewertungen

- Sap Accounting EntriesDokument9 SeitenSap Accounting Entriesswayam100% (1)

- PGDM I Semester I Management Accounting - 1 (Ma-1) : 1. Course ObjectiveDokument4 SeitenPGDM I Semester I Management Accounting - 1 (Ma-1) : 1. Course Objectivecooldude690Noch keine Bewertungen

- ACC-303 Discussion QuestionsDokument15 SeitenACC-303 Discussion QuestionsVivek Surana100% (1)

- CH 3.3 Errors - SDokument10 SeitenCH 3.3 Errors - Sসাঈদ আহমদ0% (1)

- Q 4 Results Intimation 240522Dokument29 SeitenQ 4 Results Intimation 240522kumar sunnyNoch keine Bewertungen

- Latihan Soal With DiscussionDokument6 SeitenLatihan Soal With DiscussionNicolas ErnestoNoch keine Bewertungen

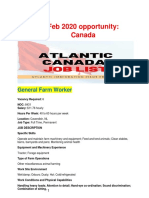

- Canada Job Opportunity ListDokument39 SeitenCanada Job Opportunity ListVaibhav Gujrati VickyNoch keine Bewertungen