Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Why Do Vietnamese Like Tiktok Shopping enDokument18 SeitenWhy Do Vietnamese Like Tiktok Shopping enChi Linh NguyenNoch keine Bewertungen

- Car Loan FinalDokument21 SeitenCar Loan Finalislamkilaniya66100% (1)

- The Nature of Electronic Commerce Group 2Dokument23 SeitenThe Nature of Electronic Commerce Group 2Danica ZabalaNoch keine Bewertungen

- Flow Chart of Sales SystemDokument2 SeitenFlow Chart of Sales SystemleekosalNoch keine Bewertungen

- Citibank SingaporeDokument8 SeitenCitibank SingaporeYudis TiawanNoch keine Bewertungen

- Letter of CreditDokument7 SeitenLetter of CreditCh WaqasNoch keine Bewertungen

- Airtel Nigeria - Manager TransmissionDokument3 SeitenAirtel Nigeria - Manager Transmissionogagz ogagzNoch keine Bewertungen

- Verizon Case StudyDokument3 SeitenVerizon Case StudyAashiq Rahman100% (1)

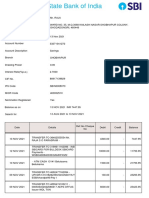

- Account Statement From 1 Jun 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument8 SeitenAccount Statement From 1 Jun 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancekiran gemsNoch keine Bewertungen

- Bank Op Manager JDDokument4 SeitenBank Op Manager JDgopal royNoch keine Bewertungen

- Chapter 1 Part 1 Multiple ChoiceDokument4 SeitenChapter 1 Part 1 Multiple ChoiceArlanosaurusNoch keine Bewertungen

- GomeDokument9 SeitenGomeaakashblueNoch keine Bewertungen

- Difference Between Bookkeeping and AccountingDokument1 SeiteDifference Between Bookkeeping and AccountingUtsav KumarNoch keine Bewertungen

- Computerised Accounting AutoCount - EnGDokument46 SeitenComputerised Accounting AutoCount - EnGEra Trace100% (1)

- 2nd Floor, Paramount Apartment, Daram Karam Road, Ameerpet-500032Dokument2 Seiten2nd Floor, Paramount Apartment, Daram Karam Road, Ameerpet-500032Raghavendar Reddy BobbalaNoch keine Bewertungen

- Neft Challan CanaraDokument1 SeiteNeft Challan Canarasrivenkateshwaracoirs250533% (3)

- Ecom 1Dokument81 SeitenEcom 1sparkle_suruNoch keine Bewertungen

- Principles of Marketing: RetailingDokument26 SeitenPrinciples of Marketing: RetailingDevanshu BaberwalNoch keine Bewertungen

- Institute of Corporate Secretaries of Pakistan: Icsp - Admission GuideDokument8 SeitenInstitute of Corporate Secretaries of Pakistan: Icsp - Admission GuideARquam JamaliNoch keine Bewertungen

- Medical School InterviewDokument7 SeitenMedical School InterviewVanessa Offda WallNoch keine Bewertungen

- Current Affairs 2017Dokument43 SeitenCurrent Affairs 2017BaskarBossYuvanRomeo'zNoch keine Bewertungen

- Payment Receipt PDFDokument1 SeitePayment Receipt PDFrajeshNoch keine Bewertungen

- Lovelyn Q. Bunda, Rca, LPT: Davao City, Davao Del SurDokument3 SeitenLovelyn Q. Bunda, Rca, LPT: Davao City, Davao Del SurLovelyn Bunda-PalomoNoch keine Bewertungen

- Consent For Use and Disclosure of Health InformationDokument2 SeitenConsent For Use and Disclosure of Health Informationapi-355962771Noch keine Bewertungen

- Research Project (Prateek Gulati)Dokument82 SeitenResearch Project (Prateek Gulati)prateekNoch keine Bewertungen

- Chapter 3: An Introduction To The Payments System I. Payment SystemDokument2 SeitenChapter 3: An Introduction To The Payments System I. Payment SystemDeniña Elaine MaeNoch keine Bewertungen

- Certificate of Insurance: Outbound TravelDokument2 SeitenCertificate of Insurance: Outbound Travelafzymohd1710Noch keine Bewertungen

- Postpay Bill: VAT Registration Number VAT: 0113241A PIN Number: P051129820X 1-229587980332Dokument3 SeitenPostpay Bill: VAT Registration Number VAT: 0113241A PIN Number: P051129820X 1-229587980332Chrispus MutabuuzaNoch keine Bewertungen

- TM 12-Ch07 Accounting Information System EDITDokument40 SeitenTM 12-Ch07 Accounting Information System EDITLydia PujiellitaNoch keine Bewertungen

- Account StatementDokument12 SeitenAccount StatementProfit Mart100% (1)