Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Aqa Accn4 W Ms Jun13Dokument12 SeitenAqa Accn4 W Ms Jun13zahid_mahmood3811Noch keine Bewertungen

- Administrative Coordinator Job DescriptionDokument8 SeitenAdministrative Coordinator Job DescriptionadministrativemanageNoch keine Bewertungen

- UP B2005 - Legal Profession ReviewerDokument42 SeitenUP B2005 - Legal Profession ReviewerSui75% (4)

- DLP - Straight Lines and Curved Lines and Three - Dimensional Flat SurfacesDokument7 SeitenDLP - Straight Lines and Curved Lines and Three - Dimensional Flat SurfacesCrizzel Mercado100% (1)

- Tos With Questions21STDokument5 SeitenTos With Questions21STEva100% (1)

- Komunikasyon Sa Akademikong FilipinoDokument17 SeitenKomunikasyon Sa Akademikong FilipinoCharo GironellaNoch keine Bewertungen

- 7110 s03 QP 1Dokument12 Seiten7110 s03 QP 1zahid_mahmood3811Noch keine Bewertungen

- 7110 s03 Ms 1Dokument1 Seite7110 s03 Ms 1zahid_mahmood3811Noch keine Bewertungen

- Aqa Accn4 W Ms Jun12Dokument15 SeitenAqa Accn4 W Ms Jun12zahid_mahmood3811Noch keine Bewertungen

- 7110 s04 Ms 1Dokument1 Seite7110 s04 Ms 1zahid_mahmood3811Noch keine Bewertungen

- Question Paper Unit f012 01 Accounting ApplicationsDokument28 SeitenQuestion Paper Unit f012 01 Accounting Applicationszahid_mahmood3811Noch keine Bewertungen

- Aqa Accn1 QP Jun13 2Dokument20 SeitenAqa Accn1 QP Jun13 2zahid_mahmood3811Noch keine Bewertungen

- Lasania Real TasteDokument6 SeitenLasania Real Tastezahid_mahmood3811Noch keine Bewertungen

- Aqa 2121 Accn3 W MS Jan 12Dokument14 SeitenAqa 2121 Accn3 W MS Jan 12zahid_mahmood3811Noch keine Bewertungen

- Aqa Accn1 W Ms Jan13Dokument10 SeitenAqa Accn1 W Ms Jan13zahid_mahmood3811Noch keine Bewertungen

- 2008 June Paper 1Dokument2 Seiten2008 June Paper 1zahid_mahmood3811Noch keine Bewertungen

- Aqa Accn1 QP Jun12Dokument16 SeitenAqa Accn1 QP Jun12zahid_mahmood3811Noch keine Bewertungen

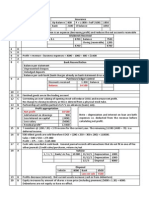

- Income Summary 3500 Balance (Prepayment) 1000: November 2009 Paper 11 Rent ReceivedDokument2 SeitenIncome Summary 3500 Balance (Prepayment) 1000: November 2009 Paper 11 Rent Receivedzahid_mahmood3811Noch keine Bewertungen

- 2013 June Paper 11Dokument2 Seiten2013 June Paper 11zahid_mahmood3811Noch keine Bewertungen

- Insurance: Balance 14 100Dokument2 SeitenInsurance: Balance 14 100zahid_mahmood3811Noch keine Bewertungen

- General Journal: Goodwill 70Dokument2 SeitenGeneral Journal: Goodwill 70zahid_mahmood3811Noch keine Bewertungen

- 2012 Nov Paper 32Dokument2 Seiten2012 Nov Paper 32zahid_mahmood3811Noch keine Bewertungen

- Capital X (Share of Gain) 10 Capital Y (Share of Gain) 5: Revaluation AccountDokument2 SeitenCapital X (Share of Gain) 10 Capital Y (Share of Gain) 5: Revaluation Accountzahid_mahmood3811Noch keine Bewertungen

- Profit (50:50 Split) 16: RealisationDokument3 SeitenProfit (50:50 Split) 16: Realisationzahid_mahmood3811Noch keine Bewertungen

- GoodmorningDokument17 SeitenGoodmorningzahid_mahmood3811Noch keine Bewertungen

- Diet PlanDokument1 SeiteDiet Planzahid_mahmood3811Noch keine Bewertungen

- Depreciation Schedule: Income Statement 95Dokument2 SeitenDepreciation Schedule: Income Statement 95zahid_mahmood3811Noch keine Bewertungen

- (Normal Probability) (Discrete Probability) : Xy Xy X yDokument1 Seite(Normal Probability) (Discrete Probability) : Xy Xy X yzahid_mahmood3811Noch keine Bewertungen

- The Childrens EraDokument4 SeitenThe Childrens Eraapi-318410427Noch keine Bewertungen

- Networking Essentials Release Notes: PurposeDokument2 SeitenNetworking Essentials Release Notes: PurposeGLNoch keine Bewertungen

- Sage ReferenceDokument36 SeitenSage ReferenceVirgilio de CarvalhoNoch keine Bewertungen

- Ryan International School (CBSE), Malad: Schedule For The Week 20/09/2021 To 25/09/2021Dokument4 SeitenRyan International School (CBSE), Malad: Schedule For The Week 20/09/2021 To 25/09/2021Anu SinghNoch keine Bewertungen

- Summer 22-23 ADMS 3060 Welcome To The Course and InstructionsDokument6 SeitenSummer 22-23 ADMS 3060 Welcome To The Course and InstructionsIris YanNoch keine Bewertungen

- Result B.A. (Hons) 2nd Generic Sem - I (2015-18 To 2019-22)Dokument257 SeitenResult B.A. (Hons) 2nd Generic Sem - I (2015-18 To 2019-22)NIRAJ KUMARNoch keine Bewertungen

- BA903158 Ashfaq Ahmed LSST UWL BEDokument15 SeitenBA903158 Ashfaq Ahmed LSST UWL BENazmus SaifNoch keine Bewertungen

- Snas Idp 2023-2028Dokument80 SeitenSnas Idp 2023-2028cmcarreonNoch keine Bewertungen

- Resume Abigail Elsant Docx 4 14 16Dokument2 SeitenResume Abigail Elsant Docx 4 14 16api-323491949Noch keine Bewertungen

- Project ProposalDokument2 SeitenProject ProposalVinay KumarNoch keine Bewertungen

- Midnight: A True Story of Loyalty in World War I Teachers' GuideDokument5 SeitenMidnight: A True Story of Loyalty in World War I Teachers' GuideCandlewick PressNoch keine Bewertungen

- Notice: Dean, Students' WelfareDokument1 SeiteNotice: Dean, Students' WelfareSthitapragyan RathNoch keine Bewertungen

- 2022 Action Plan - ScienceDokument4 Seiten2022 Action Plan - ScienceArlene L. AbalaNoch keine Bewertungen

- Graphic Design Thinking Beyond Brainstorming EbookDokument4 SeitenGraphic Design Thinking Beyond Brainstorming EbookSam NaeemNoch keine Bewertungen

- GT Program Orientation 2014Dokument18 SeitenGT Program Orientation 2014api-235701100Noch keine Bewertungen

- Education and SocietyDokument14 SeitenEducation and SocietyluluNoch keine Bewertungen

- Annex C Parental Consent and Waiver FormDokument4 SeitenAnnex C Parental Consent and Waiver FormBLANCA ABANAGNoch keine Bewertungen

- Bohol Island State University: College of Advance Studies (Cads) Master of Arts in Teaching Vocational Education (Matve)Dokument2 SeitenBohol Island State University: College of Advance Studies (Cads) Master of Arts in Teaching Vocational Education (Matve)RoanBronolaSumalinogNoch keine Bewertungen

- Trends in Educational PlanningDokument2 SeitenTrends in Educational PlanningRyan Negad100% (4)

- Strategic Training: 6 Edition Raymond A. NoeDokument45 SeitenStrategic Training: 6 Edition Raymond A. NoeHami YaraNoch keine Bewertungen

- Modelado de Un Helicóptero de 2 Grados de LibertadDokument4 SeitenModelado de Un Helicóptero de 2 Grados de Libertadlarc0112Noch keine Bewertungen

- Small Grant Guideline-Kh (March 26)Dokument41 SeitenSmall Grant Guideline-Kh (March 26)Ly SopheaNoch keine Bewertungen

- Andhra PradeshDokument39 SeitenAndhra PradeshsumanramanujanNoch keine Bewertungen

- Geostrategy - WikiDokument13 SeitenGeostrategy - WikiJohnnutz IonutzNoch keine Bewertungen

- Project 101082749Dokument2 SeitenProject 101082749muddassir razzaqNoch keine Bewertungen