Das könnte Ihnen auch gefallen

- Debt FinancingDokument1 SeiteDebt FinancingnooguNoch keine Bewertungen

- Year 11 Test 3Dokument1 SeiteYear 11 Test 3nooguNoch keine Bewertungen

- Problem Set 4Dokument3 SeitenProblem Set 4nooguNoch keine Bewertungen

- World Heritage Task Semester 1 2016Dokument3 SeitenWorld Heritage Task Semester 1 2016nooguNoch keine Bewertungen

- Who Was A Dragon Rider and Like A Father To Me. May His Name Live On in GloryDokument1 SeiteWho Was A Dragon Rider and Like A Father To Me. May His Name Live On in GlorynooguNoch keine Bewertungen

- Unit Outline FINS1612 Sem2 2015Dokument17 SeitenUnit Outline FINS1612 Sem2 2015nooguNoch keine Bewertungen

- Ingredients (8 Servings) Almond Dacquoise: WatermelonDokument2 SeitenIngredients (8 Servings) Almond Dacquoise: WatermelonnooguNoch keine Bewertungen

- Drought Surrounding LaDokument5 SeitenDrought Surrounding LanooguNoch keine Bewertungen

- Tutorial 1: Study Strategies For Psychology - Time ManagementDokument1 SeiteTutorial 1: Study Strategies For Psychology - Time ManagementnooguNoch keine Bewertungen

- Viney7e SM Ch13Dokument27 SeitenViney7e SM Ch13nooguNoch keine Bewertungen

- Helicobacter Pylori Eradication RacgpDokument6 SeitenHelicobacter Pylori Eradication Racgpnoogu100% (1)

- Year 9 Geography Study Guide - Half Yearly: Topics Covered in The ExamDokument1 SeiteYear 9 Geography Study Guide - Half Yearly: Topics Covered in The ExamnooguNoch keine Bewertungen

- Writing A Module B ResponseDokument15 SeitenWriting A Module B ResponsenooguNoch keine Bewertungen

- Legal NotesDokument45 SeitenLegal NotesnooguNoch keine Bewertungen

- Section I: Total Marks (15) Attempt Question 1 Allow About 40 Minutes For This Section Begin A New Examination BookletDokument11 SeitenSection I: Total Marks (15) Attempt Question 1 Allow About 40 Minutes For This Section Begin A New Examination BookletnooguNoch keine Bewertungen

- HSC-English Advanced - Frankenstein-Blade Runner - Yr 12-Essays and Projects-5315Dokument2 SeitenHSC-English Advanced - Frankenstein-Blade Runner - Yr 12-Essays and Projects-5315nooguNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Journal, Ledger & Trial BalanceDokument14 SeitenJournal, Ledger & Trial Balancekaran_madan2000100% (4)

- AC102-002 Midterm ExamDokument4 SeitenAC102-002 Midterm ExamArnam ManaNoch keine Bewertungen

- Ferrer-Study Notes-Chapter 4Dokument4 SeitenFerrer-Study Notes-Chapter 4Ciara FerrerNoch keine Bewertungen

- FA1 FA2 FA3 FA4 MergedDokument12 SeitenFA1 FA2 FA3 FA4 MergedBhavesh GuravNoch keine Bewertungen

- Chapter 5 - DoneDokument19 SeitenChapter 5 - DonegugusNoch keine Bewertungen

- Kunci JWB pkt2. 3 PDsuburDokument45 SeitenKunci JWB pkt2. 3 PDsuburSyifa FaNoch keine Bewertungen

- Computer in AccountingDokument10 SeitenComputer in AccountingCyber WarriorNoch keine Bewertungen

- Fundamentals of Accounting 1Dokument8 SeitenFundamentals of Accounting 1Cjhay Marcos100% (1)

- Final Report: Submitted By: TAIMOOR RIAZ 13044954-030 Submitted ToDokument65 SeitenFinal Report: Submitted By: TAIMOOR RIAZ 13044954-030 Submitted ToSherryMirzaNoch keine Bewertungen

- Handbook - On - Professional - Opportunities in Internal AuditDokument278 SeitenHandbook - On - Professional - Opportunities in Internal Auditahmed raoufNoch keine Bewertungen

- Chapter 7Dokument6 SeitenChapter 7Pranshu GuptaNoch keine Bewertungen

- Ias 16Dokument26 SeitenIas 16Niharika MishraNoch keine Bewertungen

- Accounting Terms Cheat Sheet PDFDokument5 SeitenAccounting Terms Cheat Sheet PDFBanzragch JamsranNoch keine Bewertungen

- CPA 1 - Financial Accounting-1Dokument9 SeitenCPA 1 - Financial Accounting-1LYNETTE NYAKAISIKI50% (2)

- CA IPCC Accounting Guideline Answers May 2015Dokument24 SeitenCA IPCC Accounting Guideline Answers May 2015Prashant PandeyNoch keine Bewertungen

- VI. 80% Owned-Subsidiary: Cost Model - Full Goodwill Approach Downstream and Upstream of Property, Unrealized Gain and Realized Gain On SaleDokument3 SeitenVI. 80% Owned-Subsidiary: Cost Model - Full Goodwill Approach Downstream and Upstream of Property, Unrealized Gain and Realized Gain On SaleMa'arifa HussainNoch keine Bewertungen

- MC 2 - A201 - QuestionDokument6 SeitenMC 2 - A201 - Questionlim qsNoch keine Bewertungen

- BBADokument224 SeitenBBAyawar RaoNoch keine Bewertungen

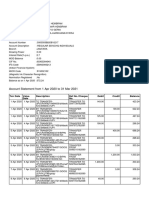

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument14 SeitenAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceHyper GamingNoch keine Bewertungen

- Osage Farm Supply Had Poor Internal Control Over Its CashDokument1 SeiteOsage Farm Supply Had Poor Internal Control Over Its CashAmit PandeyNoch keine Bewertungen

- Accounting 9th Horngren Chapter 2 SolutionDokument123 SeitenAccounting 9th Horngren Chapter 2 SolutionStenverSuurkütt67% (12)

- Asset Monitoring CbsDokument14 SeitenAsset Monitoring CbsSankara NarayananNoch keine Bewertungen

- p67645 Lcci Level 2 Certificate in Bookkeeping and Accounting Ase20093 Jan 2021Dokument20 Seitenp67645 Lcci Level 2 Certificate in Bookkeeping and Accounting Ase20093 Jan 2021Ei Ei TheintNoch keine Bewertungen

- WAC Service TheaterDokument48 SeitenWAC Service TheaterJasmine ActaNoch keine Bewertungen

- 0452 s15 Ms 23Dokument9 Seiten0452 s15 Ms 23zuzoyopi100% (1)

- Sap Fico BeginnersDokument710 SeitenSap Fico Beginnersprincereddy100% (3)

- Maintain - Financial - Standards - & - Records - Refined Pak YunDokument107 SeitenMaintain - Financial - Standards - & - Records - Refined Pak YunJohn EpraimNoch keine Bewertungen

- A Study On Working Capital of Nagarjuna Fertilizers and Chemicals LTDDokument31 SeitenA Study On Working Capital of Nagarjuna Fertilizers and Chemicals LTDorangeponyNoch keine Bewertungen

- Voucher TypesDokument4 SeitenVoucher Typesshabbir_ahmad100% (1)

- Account Closure Form1Dokument4 SeitenAccount Closure Form1gaetanopetiNoch keine Bewertungen