Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A A1471e PDFDokument108 SeitenA A1471e PDFAnil ChauhanNoch keine Bewertungen

- Business Plan On Food Vending in Finland PDFDokument65 SeitenBusiness Plan On Food Vending in Finland PDFAnil ChauhanNoch keine Bewertungen

- New Microsoft Office Word DocumentDokument1 SeiteNew Microsoft Office Word DocumentAnil ChauhanNoch keine Bewertungen

- Advantages of Joint Family System Include Equitable Economy, Care for All MembersDokument2 SeitenAdvantages of Joint Family System Include Equitable Economy, Care for All MembersAnil ChauhanNoch keine Bewertungen

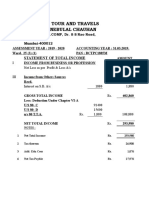

- M/S. Sunil Tour and Travels Mr. Sunil Nebulal Chauhan: Statement of Total IncomeDokument8 SeitenM/S. Sunil Tour and Travels Mr. Sunil Nebulal Chauhan: Statement of Total IncomeAnil ChauhanNoch keine Bewertungen

- Experiment No 3 DWTTDokument10 SeitenExperiment No 3 DWTTAnil ChauhanNoch keine Bewertungen

- Bank statement request letter templateDokument1 SeiteBank statement request letter templateAnil ChauhanNoch keine Bewertungen

- Urban Farm Business PlanDokument77 SeitenUrban Farm Business PlanZartosht Matthijs100% (11)

- ReambbmbdmeDokument1 SeiteReambbmbdmeNibedanPalNoch keine Bewertungen

- Book 1Dokument10 SeitenBook 1Anil ChauhanNoch keine Bewertungen

- Advantages of Joint Family System Include Equitable Economy, Care for All MembersDokument2 SeitenAdvantages of Joint Family System Include Equitable Economy, Care for All MembersAnil ChauhanNoch keine Bewertungen

- Flow ChatDokument1 SeiteFlow ChatAnil ChauhanNoch keine Bewertungen

- Goa TourismDokument11 SeitenGoa TourismAnil ChauhanNoch keine Bewertungen

- Goa TourismDokument11 SeitenGoa TourismAnil ChauhanNoch keine Bewertungen

- The Recycling of Paper Has Become Increasingly Important Over The Past DecadeDokument2 SeitenThe Recycling of Paper Has Become Increasingly Important Over The Past DecadeAnil ChauhanNoch keine Bewertungen

- What Is The Role of The SecretaryDokument3 SeitenWhat Is The Role of The SecretaryAnil ChauhanNoch keine Bewertungen

- The Recycling of Paper Has Become Increasingly Important Over The Past DecadeDokument2 SeitenThe Recycling of Paper Has Become Increasingly Important Over The Past DecadeAnil ChauhanNoch keine Bewertungen

- AbhishekDokument1 SeiteAbhishekAnil ChauhanNoch keine Bewertungen

- The Importance of Recycling PaperDokument1 SeiteThe Importance of Recycling PaperAnil ChauhanNoch keine Bewertungen

- Municipal Solutions for Eco-Efficient Recyclables ManagementDokument1 SeiteMunicipal Solutions for Eco-Efficient Recyclables ManagementAnil ChauhanNoch keine Bewertungen

- Preparation of Balance Sheet and Profit and Loss Account: TotalDokument7 SeitenPreparation of Balance Sheet and Profit and Loss Account: TotalAnil ChauhanNoch keine Bewertungen

- Paper RecyclingDokument1 SeitePaper RecyclingAnil ChauhanNoch keine Bewertungen

- Index & First 4 Pages of AfmDokument4 SeitenIndex & First 4 Pages of AfmAnil ChauhanNoch keine Bewertungen

- Born: January 23, 1897 Died: August 18, 1945 Achievements: Passed Indian Civil Services Exam Elected CongressDokument1 SeiteBorn: January 23, 1897 Died: August 18, 1945 Achievements: Passed Indian Civil Services Exam Elected CongressAnil ChauhanNoch keine Bewertungen

- Books of Account To Be Kept by A CompanyDokument8 SeitenBooks of Account To Be Kept by A CompanyAnil ChauhanNoch keine Bewertungen

- Form 12 Print PDFDokument4 SeitenForm 12 Print PDFKrishna YeldiNoch keine Bewertungen

- A Good Argument To Halt Human Advancement in Technology Is That If We Continue Creating Technologies and Researching Sciences To ReDokument1 SeiteA Good Argument To Halt Human Advancement in Technology Is That If We Continue Creating Technologies and Researching Sciences To ReAnil ChauhanNoch keine Bewertungen

- Index & First 4 Pages of AfmDokument4 SeitenIndex & First 4 Pages of AfmAnil ChauhanNoch keine Bewertungen

- Final of AFMDokument34 SeitenFinal of AFMAnil ChauhanNoch keine Bewertungen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Feasibility Study PresentationDokument22 SeitenFeasibility Study PresentationCarryl MañoscaNoch keine Bewertungen

- CH 5Dokument10 SeitenCH 5Miftahudin MiftahudinNoch keine Bewertungen

- Indian RailWay E Ticket ExampleDokument1 SeiteIndian RailWay E Ticket ExamplegouthamlalNoch keine Bewertungen

- Budgeting and Cost ControlDokument7 SeitenBudgeting and Cost Controlnags18888Noch keine Bewertungen

- Market StructureDokument42 SeitenMarket StructureSurya PanwarNoch keine Bewertungen

- Theoretical Framework on Cash Management and Business ValueDokument2 SeitenTheoretical Framework on Cash Management and Business ValuePaula ReyesNoch keine Bewertungen

- 3 - Zahtjev Za EORI Broj Primjer Kako Se PopunjavaDokument4 Seiten3 - Zahtjev Za EORI Broj Primjer Kako Se PopunjavaiŠunjić_1Noch keine Bewertungen

- Case Questions Spring 2012Dokument2 SeitenCase Questions Spring 2012Refika TetikNoch keine Bewertungen

- Swot Analysis of Indian Road NetworkDokument2 SeitenSwot Analysis of Indian Road NetworkArpit Vaidya100% (1)

- Indian All Colleges Cources List For BcomDokument56 SeitenIndian All Colleges Cources List For BcomAkshayKawaleNoch keine Bewertungen

- Problems in Estimating Production Function Empirically For A Ceramic Tile Manufacture in Sri LankaDokument15 SeitenProblems in Estimating Production Function Empirically For A Ceramic Tile Manufacture in Sri LankaRavinath NiroshanaNoch keine Bewertungen

- Pe Irr 06 30 15Dokument4 SeitenPe Irr 06 30 15Fortune100% (1)

- IRCTC E-ticket from Kota Jn to BhagalpurDokument2 SeitenIRCTC E-ticket from Kota Jn to BhagalpurAditya JhaNoch keine Bewertungen

- Bkf4143-Process Engineering Economics 11213 PDFDokument11 SeitenBkf4143-Process Engineering Economics 11213 PDFJeevanNairNoch keine Bewertungen

- Case StudyDokument6 SeitenCase Studyjuanp12560% (1)

- Solutions For Economics Review QuestionsDokument28 SeitenSolutions For Economics Review QuestionsDoris Acheng67% (3)

- EconomicDokument6 SeitenEconomicDaniloCardenasNoch keine Bewertungen

- CH 01Dokument28 SeitenCH 01aliNoch keine Bewertungen

- Executive SummaryDokument1 SeiteExecutive SummaryGuen ParkNoch keine Bewertungen

- Engineering Steel - SBQ - Supply and Demand in EuropeDokument1 SeiteEngineering Steel - SBQ - Supply and Demand in EuropeAndrzej M KotasNoch keine Bewertungen

- Reaction PaperDokument2 SeitenReaction PaperPerry Ellorin QuejadaNoch keine Bewertungen

- Eu4 Loan-To-Build Profits CalculatorDokument8 SeitenEu4 Loan-To-Build Profits CalculatorAnonymous pw0ajGNoch keine Bewertungen

- OPOSing Telugu Curries PDFDokument2 SeitenOPOSing Telugu Curries PDFpaadam68100% (2)

- End Beginning of Year of Year: Liquidity of Short-Term Assets Related Debt-Paying AbilityDokument4 SeitenEnd Beginning of Year of Year: Liquidity of Short-Term Assets Related Debt-Paying Abilityawaischeema100% (1)

- CIN - TAXINN Procedure - An Overview: Transaction Code: OBYZDokument8 SeitenCIN - TAXINN Procedure - An Overview: Transaction Code: OBYZNeelesh KumarNoch keine Bewertungen

- Food/restaurant Tenants List With Contact Details of The Company For Easy Access in The PhilippinesDokument6 SeitenFood/restaurant Tenants List With Contact Details of The Company For Easy Access in The Philippinesbey_dbNoch keine Bewertungen

- PRC Room Assignment For December 2013 Nursing Board Exam (Cebu)Dokument150 SeitenPRC Room Assignment For December 2013 Nursing Board Exam (Cebu)PhilippineNursingDirectory.comNoch keine Bewertungen

- Personal Financial StatementDokument1 SeitePersonal Financial StatementKiran KumarNoch keine Bewertungen

- Hotel ReportDokument6 SeitenHotel ReportRamji SimhadriNoch keine Bewertungen