Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Republic Vs CA, 236 Scra 257Dokument2 SeitenRepublic Vs CA, 236 Scra 257Jef Comendador100% (1)

- Wedding ScriptDokument11 SeitenWedding ScriptJevon Lorenzo Advincula100% (1)

- Internship BS in Criminology in The PhilippinesDokument8 SeitenInternship BS in Criminology in The PhilippinesJohn Vladimir A. Bulagsay0% (1)

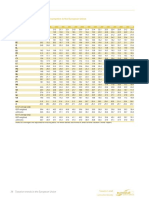

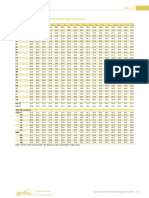

- Taxation Trends in The European Union - 2012 40Dokument1 SeiteTaxation Trends in The European Union - 2012 40Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 39Dokument1 SeiteTaxation Trends in The European Union - 2012 39Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 42Dokument1 SeiteTaxation Trends in The European Union - 2012 42Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 44Dokument1 SeiteTaxation Trends in The European Union - 2012 44Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 41Dokument1 SeiteTaxation Trends in The European Union - 2012 41Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 38Dokument1 SeiteTaxation Trends in The European Union - 2012 38Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 35Dokument1 SeiteTaxation Trends in The European Union - 2012 35Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 30Dokument1 SeiteTaxation Trends in The European Union - 2012 30Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 34Dokument1 SeiteTaxation Trends in The European Union - 2012 34Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 37Dokument1 SeiteTaxation Trends in The European Union - 2012 37Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 33Dokument1 SeiteTaxation Trends in The European Union - 2012 33Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 29Dokument1 SeiteTaxation Trends in The European Union - 2012 29Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 31Dokument1 SeiteTaxation Trends in The European Union - 2012 31Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 8Dokument1 SeiteTaxation Trends in The European Union - 2012 8Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 28Dokument1 SeiteTaxation Trends in The European Union - 2012 28Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 25Dokument1 SeiteTaxation Trends in The European Union - 2012 25Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2011 - Booklet 37Dokument1 SeiteTaxation Trends in The European Union - 2011 - Booklet 37Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 26Dokument1 SeiteTaxation Trends in The European Union - 2012 26Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 27Dokument1 SeiteTaxation Trends in The European Union - 2012 27Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 24Dokument1 SeiteTaxation Trends in The European Union - 2012 24Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 3Dokument1 SeiteTaxation Trends in The European Union - 2012 3Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2011 - Booklet 36Dokument1 SeiteTaxation Trends in The European Union - 2011 - Booklet 36Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 5Dokument1 SeiteTaxation Trends in The European Union - 2012 5Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2011 - Booklet 35Dokument1 SeiteTaxation Trends in The European Union - 2011 - Booklet 35Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2012 10Dokument1 SeiteTaxation Trends in The European Union - 2012 10Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2011 - Booklet 29Dokument1 SeiteTaxation Trends in The European Union - 2011 - Booklet 29Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2011 - Booklet 33Dokument1 SeiteTaxation Trends in The European Union - 2011 - Booklet 33Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2011 - Booklet 31Dokument1 SeiteTaxation Trends in The European Union - 2011 - Booklet 31Dimitris ArgyriouNoch keine Bewertungen

- Taxation Trends in The European Union - 2011 - Booklet 34Dokument1 SeiteTaxation Trends in The European Union - 2011 - Booklet 34Dimitris ArgyriouNoch keine Bewertungen

- Lecture 7 Political SysremDokument19 SeitenLecture 7 Political SysremDr-Najmunnisa Khan100% (1)

- AVP Compliance Director in New York City NY Resume Thomas SomelofskeDokument2 SeitenAVP Compliance Director in New York City NY Resume Thomas SomelofskeThomas SomelofskeNoch keine Bewertungen

- Tenant Construction Guide Rev1docxDokument12 SeitenTenant Construction Guide Rev1docxBer Salazar JrNoch keine Bewertungen

- Civil Service 2015Dokument44 SeitenCivil Service 2015Mesmerizing NiksNoch keine Bewertungen

- Form 26 Duplicate RCDokument1 SeiteForm 26 Duplicate RCyctgfjyNoch keine Bewertungen

- Clinical Lab FormDokument10 SeitenClinical Lab FormFlor Camille Mallari SumangNoch keine Bewertungen

- Mga Ibat Ibang Tawag Sa Mga RapistDokument7 SeitenMga Ibat Ibang Tawag Sa Mga RapistkikayNoch keine Bewertungen

- Evidence s1 PDFDokument106 SeitenEvidence s1 PDFchey_anneNoch keine Bewertungen

- 07 Government Vs Cabangis G.R. No. L 28379 Mar. 27 1929Dokument4 Seiten07 Government Vs Cabangis G.R. No. L 28379 Mar. 27 1929Awe SomontinaNoch keine Bewertungen

- State Versus Path FunctionsDokument10 SeitenState Versus Path FunctionsRohan RanaNoch keine Bewertungen

- Exam IusDokument10 SeitenExam Iusfatlum1Noch keine Bewertungen

- Ex Post FactoDokument7 SeitenEx Post FactoErica NolanNoch keine Bewertungen

- Upload A Document ScribdDokument11 SeitenUpload A Document ScribdsoumaneroprakctNoch keine Bewertungen

- Affidavit Motion For Summons by Thomas Latanowich's AttorneyDokument5 SeitenAffidavit Motion For Summons by Thomas Latanowich's AttorneyCape Cod TimesNoch keine Bewertungen

- National Highway System (United States)Dokument1 SeiteNational Highway System (United States)BMikeNoch keine Bewertungen

- Answer (Yek-146)Dokument8 SeitenAnswer (Yek-146)Ilmioamore InfermiereNoch keine Bewertungen

- Family/Community As A Site of ViolenceDokument17 SeitenFamily/Community As A Site of ViolenceHarish KumarNoch keine Bewertungen

- cwft1qb3 dmv9442135Dokument16 Seitencwft1qb3 dmv9442135Muhammad NomanNoch keine Bewertungen

- As ISO IEC 15424-2006 Information Technology - Automatic Identification and Data Capture Techniques - Data CADokument8 SeitenAs ISO IEC 15424-2006 Information Technology - Automatic Identification and Data Capture Techniques - Data CASAI Global - APACNoch keine Bewertungen

- The Danger of Joining A Gang GroupDokument22 SeitenThe Danger of Joining A Gang GroupMona Duterte LegitimasNoch keine Bewertungen

- Justification From SB 1317 and HB64Dokument4 SeitenJustification From SB 1317 and HB64robinrubinaNoch keine Bewertungen

- Self Employed Women Association (Sewa)Dokument29 SeitenSelf Employed Women Association (Sewa)man007mba3747100% (1)

- Gravity Finance White PaperDokument14 SeitenGravity Finance White PaperMichael WongNoch keine Bewertungen

- Accounting Equation: Chapter TwoDokument8 SeitenAccounting Equation: Chapter Twojohn adamNoch keine Bewertungen

- Legal Writing - Reply RejoinderDokument3 SeitenLegal Writing - Reply RejoinderdNoch keine Bewertungen

- 10 - Urbano Vs IAC - GR 72964Dokument1 Seite10 - Urbano Vs IAC - GR 72964Bae IreneNoch keine Bewertungen

- Magna Carta of WomenDokument4 SeitenMagna Carta of WomenNevej ThomasNoch keine Bewertungen