Das könnte Ihnen auch gefallen

- Sd10 Forecasting Free CashflowsDokument8 SeitenSd10 Forecasting Free CashflowsDemi Tugano BernardinoNoch keine Bewertungen

- Sd7-Discount Rates in ValuationDokument7 SeitenSd7-Discount Rates in Valuationanah ÜNoch keine Bewertungen

- SD12-The Residual Income ModelDokument6 SeitenSD12-The Residual Income ModelErickk EscanooNoch keine Bewertungen

- sd5 Financial Statement AnalysisDokument7 Seitensd5 Financial Statement Analysisxxx101xxxNoch keine Bewertungen

- Sd8-The Dividend Discount and Flows To Equity ModelsDokument7 SeitenSd8-The Dividend Discount and Flows To Equity Modelsanah ÜNoch keine Bewertungen

- Capital Budgeting and Cost AnalysisDokument4 SeitenCapital Budgeting and Cost Analysishxn1421Noch keine Bewertungen

- Financial Performance Measures and Value Creation: the State of the ArtVon EverandFinancial Performance Measures and Value Creation: the State of the ArtNoch keine Bewertungen

- Intermediate Accounting HWDokument6 SeitenIntermediate Accounting HWbossman890% (1)

- The Validity of Company Valuation Using Discounted Cash Flow MethodsDokument25 SeitenThe Validity of Company Valuation Using Discounted Cash Flow MethodsSoumya MishraNoch keine Bewertungen

- CSE - 3rd ECONOMICS - FOR - ENGINEERSDokument8 SeitenCSE - 3rd ECONOMICS - FOR - ENGINEERSsamir pramanikNoch keine Bewertungen

- The Appraisal of Capital Projects: C. G. LewinDokument28 SeitenThe Appraisal of Capital Projects: C. G. LewinBhuvana ArasuNoch keine Bewertungen

- Investment Management ConclusionDokument14 SeitenInvestment Management ConclusionDeepak OswalNoch keine Bewertungen

- Tutorial 2Dokument5 SeitenTutorial 2Hirushika BandaraNoch keine Bewertungen

- Capital BugetingDokument6 SeitenCapital BugetingMichael ReyesNoch keine Bewertungen

- RW J Chapter 14 Problem SolutionsDokument6 SeitenRW J Chapter 14 Problem SolutionsAlexandro Lai100% (1)

- Chapter 4Dokument10 SeitenChapter 4Seid KassawNoch keine Bewertungen

- Intermediate Accounting ch02 PDFDokument4 SeitenIntermediate Accounting ch02 PDFRonald KahoraNoch keine Bewertungen

- Techniques of Financial Analysis: Unit 2Dokument33 SeitenTechniques of Financial Analysis: Unit 2RAHUL GHOSALENoch keine Bewertungen

- LBO AnalysisDokument7 SeitenLBO AnalysisLeonardoNoch keine Bewertungen

- 13Dokument14 Seiten13JDNoch keine Bewertungen

- Modeling CH 2Dokument58 SeitenModeling CH 2rsh765Noch keine Bewertungen

- Case Study - WACC in Practice and Change in Capital Structure - 231024Dokument4 SeitenCase Study - WACC in Practice and Change in Capital Structure - 231024lolojNoch keine Bewertungen

- 05-Financial Stratement AnalysisDokument8 Seiten05-Financial Stratement AnalysisPratheep GsNoch keine Bewertungen

- DCF PrimerDokument30 SeitenDCF PrimerAnkit_modi2000Noch keine Bewertungen

- Constructing Consistent Financial Planning Models For ValuationDokument32 SeitenConstructing Consistent Financial Planning Models For ValuationFlavio Vilas-BoasNoch keine Bewertungen

- Chapter 26 Web Extension Comparison of Alternative Valuation ModelsDokument9 SeitenChapter 26 Web Extension Comparison of Alternative Valuation ModelsLâmViênNoch keine Bewertungen

- Capitulo 2Dokument12 SeitenCapitulo 2Daniel Adrián Avilés VélezNoch keine Bewertungen

- CFINDokument10 SeitenCFINAnuj AgarwalNoch keine Bewertungen

- Chap 09 Prospective AnalysisDokument35 SeitenChap 09 Prospective AnalysisHiếu Nhi TrịnhNoch keine Bewertungen

- SM Alk 9Dokument35 SeitenSM Alk 9Jogja AntiqNoch keine Bewertungen

- Analysis of The Albanian Banking System in A Risk Performance FrameworkDokument44 SeitenAnalysis of The Albanian Banking System in A Risk Performance FrameworkYogesh MungurNoch keine Bewertungen

- 2015.11 FRM 二级 mock 题: Societe Generale'sDokument29 Seiten2015.11 FRM 二级 mock 题: Societe Generale'slowchangsongNoch keine Bewertungen

- HA3032 Auditing Tutorial Soln 6 2010 Tri 1Dokument5 SeitenHA3032 Auditing Tutorial Soln 6 2010 Tri 1sumil07Noch keine Bewertungen

- Solution CH 09-SubramanyamDokument34 SeitenSolution CH 09-SubramanyamErna hk100% (1)

- Fs Analysis 2 For Learning and StudyDokument82 SeitenFs Analysis 2 For Learning and StudyeiaNoch keine Bewertungen

- Evaluating Project Economics and Capital Rationing: Learning ObjectivesDokument53 SeitenEvaluating Project Economics and Capital Rationing: Learning ObjectivesShoniqua JohnsonNoch keine Bewertungen

- FIN 370 Final Exam Answers Grade - 100Dokument9 SeitenFIN 370 Final Exam Answers Grade - 100Alegna72100% (4)

- Gap Analysis TemplateDokument461 SeitenGap Analysis TemplateAASIM AlamNoch keine Bewertungen

- Problem 15-16 Alcorn CompanyDokument11 SeitenProblem 15-16 Alcorn CompanypanoyNoch keine Bewertungen

- Why Is It Important For The Financial Manager To Understand The Valuation Process?Dokument7 SeitenWhy Is It Important For The Financial Manager To Understand The Valuation Process?Jamilia LewisNoch keine Bewertungen

- VCM Chap 5 6 Questions Midterms PDFDokument11 SeitenVCM Chap 5 6 Questions Midterms PDFMika MolinaNoch keine Bewertungen

- 18 - Findings Conclusion and Suggestion PDFDokument22 Seiten18 - Findings Conclusion and Suggestion PDFSwarup BhagatNoch keine Bewertungen

- Mid Summer 2018Dokument3 SeitenMid Summer 2018rtgxd25zygNoch keine Bewertungen

- RTDokument58 SeitenRTKyaw Htin WinNoch keine Bewertungen

- Acct 4102Dokument40 SeitenAcct 4102Shimul HossainNoch keine Bewertungen

- FXTM - Model Question Paper 2Dokument37 SeitenFXTM - Model Question Paper 2Rajiv WarrierNoch keine Bewertungen

- Learning OutcomesDokument48 SeitenLearning OutcomesPom Jung0% (1)

- Discounted CashflowDokument36 SeitenDiscounted CashflowthanhcvaNoch keine Bewertungen

- Chapter 2 Class Example (Including CPA Exam Questions)Dokument2 SeitenChapter 2 Class Example (Including CPA Exam Questions)Rasha YatmeenNoch keine Bewertungen

- Ignou Important Questions MMPC 004Dokument2 SeitenIgnou Important Questions MMPC 004catch meNoch keine Bewertungen

- Capital Calculations:: Has The CCRO Missed The Point?Dokument4 SeitenCapital Calculations:: Has The CCRO Missed The Point?AlisterpNoch keine Bewertungen

- Questions 1 - 6 Pertain To The Case Study Each Question Should Be Answered IndependentlyDokument22 SeitenQuestions 1 - 6 Pertain To The Case Study Each Question Should Be Answered IndependentlyNoura ShamseddineNoch keine Bewertungen

- Chapter-9 Analysis of Financial Statements: Section A: One Mark Questions I. Fill in The BlanksDokument10 SeitenChapter-9 Analysis of Financial Statements: Section A: One Mark Questions I. Fill in The BlanksAlton D'silvaNoch keine Bewertungen

- Final Auditing Question Paper - May - 2008Dokument5 SeitenFinal Auditing Question Paper - May - 2008Khristine CaserialNoch keine Bewertungen

- Case StudyDokument10 SeitenCase StudyAmit Verma100% (1)

- Preparing For Solvency II - Theoretical and Practical Issues in BuildingDokument20 SeitenPreparing For Solvency II - Theoretical and Practical Issues in Buildingapi-3699209100% (1)

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkVon EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNoch keine Bewertungen

- SD2-Security Analysis and Efficient MarketDokument6 SeitenSD2-Security Analysis and Efficient Marketanah ÜNoch keine Bewertungen

- Sample Chart of AccountsDokument3 SeitenSample Chart of Accountsanah ÜNoch keine Bewertungen

- Acctg602 - Prac1Dokument1 SeiteAcctg602 - Prac1anah ÜNoch keine Bewertungen

- Accounting Services AgreementDokument5 SeitenAccounting Services Agreementanah ÜNoch keine Bewertungen

- Investments AuditingDokument4 SeitenInvestments Auditinganah ÜNoch keine Bewertungen

- Chapter 2 - Transfer Taxes and Basic SuccessionDokument5 SeitenChapter 2 - Transfer Taxes and Basic SuccessionRitzchalle Garcia-OalinNoch keine Bewertungen

- Chapter 5 - Estate TaxDokument11 SeitenChapter 5 - Estate TaxMargery Bumagat100% (1)

- Chap 018Dokument25 SeitenChap 018anah ÜNoch keine Bewertungen

- TS1018773341Dokument1 SeiteTS1018773341anah ÜNoch keine Bewertungen

- Basketball NotesDokument27 SeitenBasketball Notesanah ÜNoch keine Bewertungen

- Ballroom Dancing HandoutsDokument7 SeitenBallroom Dancing Handoutsanah Ü60% (5)

- FINANCE MANAGEMENT FIN420 CHP 3Dokument40 SeitenFINANCE MANAGEMENT FIN420 CHP 3Yanty Ibrahim50% (2)

- International FinanceDokument14 SeitenInternational Financecpsandeepgowda6828100% (1)

- Im Acco 01bc Fundamentals of Accounting Part 1Dokument110 SeitenIm Acco 01bc Fundamentals of Accounting Part 1Mikaella Del Rosario100% (1)

- Nestle Pakistan Limited Balance Sheet: 2020 2019 2018 Equity and Liabilities Share Capital and ReservesDokument39 SeitenNestle Pakistan Limited Balance Sheet: 2020 2019 2018 Equity and Liabilities Share Capital and ReservesFarah NazNoch keine Bewertungen

- Financial Accounting Assignment 1Dokument3 SeitenFinancial Accounting Assignment 1Mr Chaitanya Valiveti IPENoch keine Bewertungen

- ACF5950 - Assignment # 109 Semester 2 2014: The Business Has The Following Opening Balances: Additional InformationDokument2 SeitenACF5950 - Assignment # 109 Semester 2 2014: The Business Has The Following Opening Balances: Additional InformationkietNoch keine Bewertungen

- Consolidation Exercises With AsnwerDokument47 SeitenConsolidation Exercises With Asnwerjessica amorosoNoch keine Bewertungen

- Bus 5112 - Written Assignment Polly Pet Food Finacial StatementDokument5 SeitenBus 5112 - Written Assignment Polly Pet Food Finacial Statementmynalawal100% (2)

- Afar 05Dokument3 SeitenAfar 05ruel c armillaNoch keine Bewertungen

- Acctg122 - Chapter 1Dokument25 SeitenAcctg122 - Chapter 1Ice James Pachano0% (1)

- Caremark Investments LTD Business Plan - 11.02.2019 PDFDokument166 SeitenCaremark Investments LTD Business Plan - 11.02.2019 PDFHerbert BusharaNoch keine Bewertungen

- Chapter 20: Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeDokument9 SeitenChapter 20: Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeAnna TaylorNoch keine Bewertungen

- PS - 1 and 2Dokument6 SeitenPS - 1 and 2Rey Joyce AbuelNoch keine Bewertungen

- Adjusting The Accounts Assignment Classification TableDokument108 SeitenAdjusting The Accounts Assignment Classification TableDalbir SinghNoch keine Bewertungen

- PLX Model OfficialDokument105 SeitenPLX Model OfficialBảo Ngọc LêNoch keine Bewertungen

- Final Answer Key Buad 280 Practice Exam Midterm 3Dokument7 SeitenFinal Answer Key Buad 280 Practice Exam Midterm 3Connor JacksonNoch keine Bewertungen

- Cash & Cash EquivalentsDokument10 SeitenCash & Cash EquivalentsKristine Valerie BonghanoyNoch keine Bewertungen

- CH 10 Accruals and PrepaymentsDokument8 SeitenCH 10 Accruals and PrepaymentsBuntheaNoch keine Bewertungen

- UntitledDokument4 SeitenUntitledAditya ChavanNoch keine Bewertungen

- Basics of Accounting and Finance For Small Water SystemsDokument34 SeitenBasics of Accounting and Finance For Small Water SystemsRashe FasiNoch keine Bewertungen

- Facebook - DCF ValuationDokument9.372 SeitenFacebook - DCF ValuationDibyajyoti Oja0% (2)

- Measuring and Evaluating The Performance of Banks and Their Principal Competitors Fill in The Blank QuestionsDokument38 SeitenMeasuring and Evaluating The Performance of Banks and Their Principal Competitors Fill in The Blank QuestionsNahid Md. AlamNoch keine Bewertungen

- Pamantasan NG CabuyaoDokument2 SeitenPamantasan NG CabuyaoHhhhhNoch keine Bewertungen

- Suggested - Answer - CAP - II - June - 2016 6Dokument75 SeitenSuggested - Answer - CAP - II - June - 2016 6Dipen AdhikariNoch keine Bewertungen

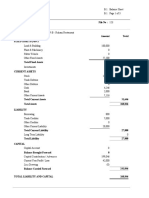

- Balance Shit!!Dokument3 SeitenBalance Shit!!Irfan izhamNoch keine Bewertungen

- Balance Sheet: As at 31st March, 2015Dokument2 SeitenBalance Sheet: As at 31st March, 2015Dhairyaa BhardwajNoch keine Bewertungen

- Chapter 11: Depreciation, Impairments and DepletionDokument24 SeitenChapter 11: Depreciation, Impairments and DepletionRahat KhanNoch keine Bewertungen

- Sample SAP Liquidity PlannerDokument13 SeitenSample SAP Liquidity Plannerapl16Noch keine Bewertungen

- Completion of The Accounting Cycle: Weygandt - Kieso - KimmelDokument51 SeitenCompletion of The Accounting Cycle: Weygandt - Kieso - KimmelAbdullah Al AminNoch keine Bewertungen

- 4.1 Theory Common Size StatementDokument3 Seiten4.1 Theory Common Size StatementNinad GadreNoch keine Bewertungen