Das könnte Ihnen auch gefallen

- 2 ImsDokument37 Seiten2 ImsZelyna RamosNoch keine Bewertungen

- First Working GroupDokument8 SeitenFirst Working GroupdivyanshushuklaNoch keine Bewertungen

- Foreign Exchange RateDokument20 SeitenForeign Exchange RatePrabhneet100% (1)

- Senate Hearing, 108TH Congress - Bank Secrecy Act EnforcementDokument124 SeitenSenate Hearing, 108TH Congress - Bank Secrecy Act EnforcementScribd Government DocsNoch keine Bewertungen

- Bretton Wood 2Dokument3 SeitenBretton Wood 2Neil NeilsonNoch keine Bewertungen

- The Scam That Is Silicon Valley Tech StocksDokument15 SeitenThe Scam That Is Silicon Valley Tech StocksSCRIBD444Noch keine Bewertungen

- Reserve Bank of India's Policy Dilemmas: Reconciling Policy Goals in Times of TurbulenceDokument31 SeitenReserve Bank of India's Policy Dilemmas: Reconciling Policy Goals in Times of TurbulenceAsian Development Bank100% (1)

- Cryptocurrency: What Is Cryptocurrency ? The Money of The Future?Dokument8 SeitenCryptocurrency: What Is Cryptocurrency ? The Money of The Future?Sweetha MNoch keine Bewertungen

- Commercial BankingDokument5 SeitenCommercial BankingJasleen kaurNoch keine Bewertungen

- Triffin Dilemma: Onset During Bretton Woods EraDokument4 SeitenTriffin Dilemma: Onset During Bretton Woods Erayoutube watcherNoch keine Bewertungen

- 5 Int Monetary SystemDokument43 Seiten5 Int Monetary SystemumangNoch keine Bewertungen

- Business Cycle PDFDokument15 SeitenBusiness Cycle PDFBernard OkpeNoch keine Bewertungen

- History Money Usury in America Revised 2015Dokument208 SeitenHistory Money Usury in America Revised 2015ROBERTO CAVALCANTINoch keine Bewertungen

- A Project On Central BankDokument15 SeitenA Project On Central BankSonu PradhanNoch keine Bewertungen

- International Monetary SystemsDokument102 SeitenInternational Monetary SystemsATHINoch keine Bewertungen

- Government General ObjectivesDokument7 SeitenGovernment General ObjectivesHamak Twotorial KollegeNoch keine Bewertungen

- BN Research Report 2018 FINALDokument19 SeitenBN Research Report 2018 FINALchristophe RenaudineauNoch keine Bewertungen

- TransactionalDokument34 SeitenTransactionalanon_314682394Noch keine Bewertungen

- 重建美国共和国的行政命令Dokument12 Seiten重建美国共和国的行政命令Xun LuNoch keine Bewertungen

- Unregulated Markets: How Regulatory Reform Will Shine A Light in The Financial SectorDokument83 SeitenUnregulated Markets: How Regulatory Reform Will Shine A Light in The Financial SectorScribd Government Docs100% (1)

- Theories of Trade CyclesDokument13 SeitenTheories of Trade CyclesSurekha NayakNoch keine Bewertungen

- GCRDokument75 SeitenGCRArti DobariyaNoch keine Bewertungen

- Globalisation and Changing Nature of Nation-StateDokument8 SeitenGlobalisation and Changing Nature of Nation-StateRitesh KhandelwalNoch keine Bewertungen

- The Rothschilds Stage Revolutions in Tunisia and EgyptDokument10 SeitenThe Rothschilds Stage Revolutions in Tunisia and EgyptZeka Sumerian OutlawNoch keine Bewertungen

- GRP 1 Financial-Market-Intro-TypesDokument34 SeitenGRP 1 Financial-Market-Intro-TypesXander C. PasionNoch keine Bewertungen

- Chapter 2Dokument44 SeitenChapter 2Shafiq HafizullahNoch keine Bewertungen

- Central Banking PDFDokument112 SeitenCentral Banking PDFSK Mishra100% (2)

- CAPE Logistics and Supply Chain Operations U1 M1 Obj 7 8 TransportationDokument11 SeitenCAPE Logistics and Supply Chain Operations U1 M1 Obj 7 8 TransportationX100% (2)

- Balance of PaymentDokument38 SeitenBalance of PaymentAyush SinghNoch keine Bewertungen

- Writ of Replevin, Vatican Bank Reissued 10-23-2013Dokument1 SeiteWrit of Replevin, Vatican Bank Reissued 10-23-2013Cindy Kay CurrierNoch keine Bewertungen

- Indian Money Market and Capital MarketDokument17 SeitenIndian Money Market and Capital MarketMerakizz100% (1)

- Factors Contributing To The Growth of The Aviation SectorDokument8 SeitenFactors Contributing To The Growth of The Aviation SectorVidhiNoch keine Bewertungen

- How The Federal Reserve Implements Monetary PolicyDokument37 SeitenHow The Federal Reserve Implements Monetary Policybüşra çakmakNoch keine Bewertungen

- Rural Development Theory, Lec. 1,2Dokument16 SeitenRural Development Theory, Lec. 1,2Matin Muhammad AminNoch keine Bewertungen

- US-China Relations - A Changing World OrderDokument17 SeitenUS-China Relations - A Changing World OrderOwen LerouxNoch keine Bewertungen

- Treaty of Versailles NotesDokument28 SeitenTreaty of Versailles NotesMukul BajajNoch keine Bewertungen

- Human Rights and United NationsDokument10 SeitenHuman Rights and United NationsEbadur RahmanNoch keine Bewertungen

- Art of War by MachiavelliDokument104 SeitenArt of War by Machiavelliペラルタ ヴィンセントスティーブNoch keine Bewertungen

- Keynes' Liquidity Preference Theory of InterestDokument3 SeitenKeynes' Liquidity Preference Theory of Interestpenny93Noch keine Bewertungen

- Introduction To Regional PlanningDokument46 SeitenIntroduction To Regional PlanningKhairul Akmal MusaNoch keine Bewertungen

- Special Drawing RightDokument12 SeitenSpecial Drawing RightrirannaNoch keine Bewertungen

- Senate Hearing, 109TH Congress - Money Laundering and Terror Financing Issues in The Middle EastDokument103 SeitenSenate Hearing, 109TH Congress - Money Laundering and Terror Financing Issues in The Middle EastScribd Government DocsNoch keine Bewertungen

- Why The US Is CollapsingDokument11 SeitenWhy The US Is CollapsingKregener100% (3)

- The World Bank and Its CriticsDokument14 SeitenThe World Bank and Its CriticsNayana SinghNoch keine Bewertungen

- Engert & Spencer IR at The Movies Teaching and Learning About International Politics Through Film Chapter4Dokument22 SeitenEngert & Spencer IR at The Movies Teaching and Learning About International Politics Through Film Chapter4BoNoch keine Bewertungen

- Economic Test Chapter 2 Economic SystemsDokument3 SeitenEconomic Test Chapter 2 Economic SystemsNathaniel Lepasana100% (2)

- Money Supply and Money Demand (File 4)Dokument21 SeitenMoney Supply and Money Demand (File 4)Sadaqatullah NoonariNoch keine Bewertungen

- Bretton Woods Complete InformationDokument1 SeiteBretton Woods Complete InformationNikhil Joshi100% (1)

- Terms of Trade: Balance of Payment Disequilibrium Corrective MeasuresDokument34 SeitenTerms of Trade: Balance of Payment Disequilibrium Corrective MeasuresvijiNoch keine Bewertungen

- Bretton Woods SystemDokument4 SeitenBretton Woods SystemTaisir MahmudNoch keine Bewertungen

- Money and Banking: Chapter - 8Dokument36 SeitenMoney and Banking: Chapter - 8Nihar NanyamNoch keine Bewertungen

- IMF and WTODokument28 SeitenIMF and WTOFahmiatul JannatNoch keine Bewertungen

- Study Material - Financial Economics-FinalDokument184 SeitenStudy Material - Financial Economics-FinalAmarendra PattnaikNoch keine Bewertungen

- Strategy For Financing The 2030 Agenda Synopsis 17 SepDokument1 SeiteStrategy For Financing The 2030 Agenda Synopsis 17 Sepmuun yayoNoch keine Bewertungen

- Cut, Cap & Balance Act As Approved by The House of Representatives - Full Text of BillDokument10 SeitenCut, Cap & Balance Act As Approved by The House of Representatives - Full Text of BillZim VicomNoch keine Bewertungen

- About The IMFDokument2 SeitenAbout The IMFdevraj5388100% (1)

- Rationale For The Study: Forex OperationsDokument64 SeitenRationale For The Study: Forex OperationsAditya DigheNoch keine Bewertungen

- CurrencyDokument35 SeitenCurrencymohit.almalNoch keine Bewertungen

- BDNG 3103Dokument11 SeitenBDNG 3103prithinahNoch keine Bewertungen

- Aiswarya V V 4 DcmsDokument37 SeitenAiswarya V V 4 DcmsRuksana BiazNoch keine Bewertungen

- Principles of CopyrightsDokument81 SeitenPrinciples of CopyrightskocherlakotapavanNoch keine Bewertungen

- Approaches To HR EvaluationDokument4 SeitenApproaches To HR EvaluationkocherlakotapavanNoch keine Bewertungen

- Treasury and Cash ManagementDokument8 SeitenTreasury and Cash ManagementkocherlakotapavanNoch keine Bewertungen

- Public Private and Joint SectorsDokument11 SeitenPublic Private and Joint SectorskocherlakotapavanNoch keine Bewertungen

- Concept of MNCDokument17 SeitenConcept of MNCkocherlakotapavanNoch keine Bewertungen

- Ipr BasicsDokument33 SeitenIpr BasicskocherlakotapavanNoch keine Bewertungen

- MEFADokument12 SeitenMEFAkocherlakotapavanNoch keine Bewertungen

- Rich Text Editor FileDokument2 SeitenRich Text Editor FilekocherlakotapavanNoch keine Bewertungen

- Product ModificationDokument2 SeitenProduct ModificationkocherlakotapavanNoch keine Bewertungen

- Processing IDOC Through LSMWDokument9 SeitenProcessing IDOC Through LSMWknani9090Noch keine Bewertungen

- Sap Tan - CodesDokument2 SeitenSap Tan - CodeskocherlakotapavanNoch keine Bewertungen

- What Is EthicsDokument39 SeitenWhat Is Ethicskocherlakotapavan100% (1)

- Sap Cin Overview & Taxation in IndiaDokument103 SeitenSap Cin Overview & Taxation in IndiaGirish RajNoch keine Bewertungen

- What's The Buzz On Smart Grids? Case StudyDokument33 SeitenWhat's The Buzz On Smart Grids? Case StudyOrko AbirNoch keine Bewertungen

- Al Baraka Islamic Bank Internship ReportDokument64 SeitenAl Baraka Islamic Bank Internship Reportsyed abu naveedNoch keine Bewertungen

- Nepal Investment Guide BookDokument40 SeitenNepal Investment Guide BookManish SinghalNoch keine Bewertungen

- 09d Investment in Equity Securities Cost Equity Method PDFDokument76 Seiten09d Investment in Equity Securities Cost Equity Method PDFXNoch keine Bewertungen

- 2130 Ds Machinery HealthAnaDokument14 Seiten2130 Ds Machinery HealthAnajose rubenNoch keine Bewertungen

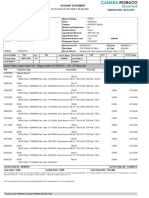

- Canara Robeco Equity Hybrid Fund - Regular Monthly IDCW (GBDP) - ISIN: INF760K01068Dokument2 SeitenCanara Robeco Equity Hybrid Fund - Regular Monthly IDCW (GBDP) - ISIN: INF760K01068brotoNoch keine Bewertungen

- July 15, 2015Dokument12 SeitenJuly 15, 2015The Delphos HeraldNoch keine Bewertungen

- Internal Reconstruction - Theory NotesDokument3 SeitenInternal Reconstruction - Theory NotesNaomi SaldanhaNoch keine Bewertungen

- Audio ScriptsDokument6 SeitenAudio ScriptsNguyên NguyễnNoch keine Bewertungen

- International Financial Management 11 Edition: by Jeff MaduraDokument33 SeitenInternational Financial Management 11 Edition: by Jeff MaduraCorolla SedanNoch keine Bewertungen

- Plantilla de Excel Con Dashboard FinancieroDokument36 SeitenPlantilla de Excel Con Dashboard FinancieroSamuel FLoresNoch keine Bewertungen

- Peninsular Malaysia Electricity Supply Outlook 2017Dokument60 SeitenPeninsular Malaysia Electricity Supply Outlook 2017You Wei WongNoch keine Bewertungen

- Gann Trading PointsDokument16 SeitenGann Trading PointsKalidas Sundararaman100% (2)

- Notes To Finacial Statements: Question 6-1Dokument23 SeitenNotes To Finacial Statements: Question 6-1Kim FloresNoch keine Bewertungen

- Chapter 2 Literature ReviewDokument24 SeitenChapter 2 Literature Reviewcoolpeer91Noch keine Bewertungen

- Presentation On SIPDokument23 SeitenPresentation On SIPRanusummiNoch keine Bewertungen

- Break Even AnalysisDokument33 SeitenBreak Even AnalysisArunraj ArumugamNoch keine Bewertungen

- Cash Flow Analysis 1Dokument61 SeitenCash Flow Analysis 1Chhaya ThakorNoch keine Bewertungen

- Case Study - BamboocraftDokument6 SeitenCase Study - BamboocraftNicah AcojonNoch keine Bewertungen

- Wrigley Gum 21Dokument18 SeitenWrigley Gum 21Fidelity RoadNoch keine Bewertungen

- Basics of Stock Market For Beginners Lectures by CA Rachana Phadke Ranade Topics (Notes)Dokument3 SeitenBasics of Stock Market For Beginners Lectures by CA Rachana Phadke Ranade Topics (Notes)kunal khurana33% (3)

- Sample Final Exam With SolutionDokument17 SeitenSample Final Exam With SolutionYevhenii VdovenkoNoch keine Bewertungen

- Sample Exam Questions (FINC3015, S1, 2012)Dokument5 SeitenSample Exam Questions (FINC3015, S1, 2012)Tecwyn LimNoch keine Bewertungen

- ECT Readers GuideDokument85 SeitenECT Readers GuideMaame Akua Adu BoaheneNoch keine Bewertungen

- IBPS Clerk Prelimsl Previous PaperDokument26 SeitenIBPS Clerk Prelimsl Previous PapershakthiNoch keine Bewertungen

- Discount Rate or Hurdle Rate Module 7 (Class 24)Dokument18 SeitenDiscount Rate or Hurdle Rate Module 7 (Class 24)Vineet Agarwal100% (1)

- Dhaka Bank FinalDokument95 SeitenDhaka Bank FinalAnonymous 8g7BHLNoch keine Bewertungen

- 10K.Jala Mammadova&Aynura AliyevaDokument12 Seiten10K.Jala Mammadova&Aynura AliyevaAynura AliyevaNoch keine Bewertungen

- Research PPT On Online TradingDokument10 SeitenResearch PPT On Online TradingbhagyashreeNoch keine Bewertungen

- Macroeconomics EssayDokument7 SeitenMacroeconomics EssayAchim EduardNoch keine Bewertungen