Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Social Determinants of Health Executive SummaryDokument40 SeitenSocial Determinants of Health Executive Summarykingcs1100% (2)

- IHC Super Tax JudgmentDokument42 SeitenIHC Super Tax JudgmentHussain Afzal100% (1)

- Business Studies in Action Jacaranda Plus John Wiley & SonsDokument488 SeitenBusiness Studies in Action Jacaranda Plus John Wiley & SonsNateNoch keine Bewertungen

- CPAR Final Pre-Board With AnswersjjjjDokument8 SeitenCPAR Final Pre-Board With AnswersjjjjMacwin KiatNoch keine Bewertungen

- Inclusions in Gross IncomeDokument2 SeitenInclusions in Gross Incomeloonie tunesNoch keine Bewertungen

- A. General Concepts and Principles of TaxationDokument4 SeitenA. General Concepts and Principles of TaxationAngelica EsguireroNoch keine Bewertungen

- Hdfcbank Credit CtalogueDokument1 SeiteHdfcbank Credit CtalogueDrSudhanshu MishraNoch keine Bewertungen

- Tax Cases 2ND BATCHDokument17 SeitenTax Cases 2ND BATCHBestie BushNoch keine Bewertungen

- HEPI Press Release September Pdf2010Dokument7 SeitenHEPI Press Release September Pdf2010Philip LewisNoch keine Bewertungen

- 2022-S SUP 3043 - 1 Assignment 1 - StudentDokument3 Seiten2022-S SUP 3043 - 1 Assignment 1 - StudentShravanNoch keine Bewertungen

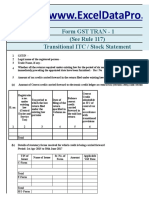

- GST TRAN 1 Return Excel TemplateDokument14 SeitenGST TRAN 1 Return Excel TemplateRaju Ranjan KumarNoch keine Bewertungen

- Export - Duty CalculationDokument2 SeitenExport - Duty CalculationSunil MateNoch keine Bewertungen

- ML-20-026 Upasani Super Specaility HospitalDokument1 SeiteML-20-026 Upasani Super Specaility Hospitaltranshind overseasNoch keine Bewertungen

- Aefpm5487a 2023Dokument4 SeitenAefpm5487a 2023enjoy enjoy enjoyNoch keine Bewertungen

- Week 7Dokument16 SeitenWeek 7Hannah Rae ChingNoch keine Bewertungen

- Full Download Ebook PDF Inside Texas Politics Power Policy and Personality of The Lone Star State PDFDokument41 SeitenFull Download Ebook PDF Inside Texas Politics Power Policy and Personality of The Lone Star State PDFmichael.acklin818100% (38)

- InvoiceDokument1 SeiteInvoice60Abhishek KalpavrukshaNoch keine Bewertungen

- CIR v. CA, CTA & Soriano Corp.Dokument3 SeitenCIR v. CA, CTA & Soriano Corp.Hinata ShoyoNoch keine Bewertungen

- Street E Town Homes ConceptDokument4 SeitenStreet E Town Homes ConceptLivewire Printing CompanyNoch keine Bewertungen

- Vendimi I Strasburgut, Antoneta SevdariDokument39 SeitenVendimi I Strasburgut, Antoneta SevdariArjola YmerajNoch keine Bewertungen

- Iedman Milton Friedman and The Social Responsibility of Business Is To Increase Its Profits The New York Times Magazine, September 13, 1970Dokument14 SeitenIedman Milton Friedman and The Social Responsibility of Business Is To Increase Its Profits The New York Times Magazine, September 13, 1970SFLDNoch keine Bewertungen

- The Courts ACT PassageDokument2 SeitenThe Courts ACT PassageimmabebigNoch keine Bewertungen

- A-28, Lawrence Road,, New Delhi - 110035 Delhi Pay Slip For The Month of January-2018Dokument2 SeitenA-28, Lawrence Road,, New Delhi - 110035 Delhi Pay Slip For The Month of January-2018Reiki Channel Anuj BhargavaNoch keine Bewertungen

- Ac2091 Za - 2019Dokument14 SeitenAc2091 Za - 2019Isra WaheedNoch keine Bewertungen

- 1 Crore: Age 40 S/A (Term - 25/16) Minimum 6 YearDokument4 Seiten1 Crore: Age 40 S/A (Term - 25/16) Minimum 6 YearramNoch keine Bewertungen

- Joshua James R. Cabinas Assignment #1 Tax 2 (3178) : WithoutDokument2 SeitenJoshua James R. Cabinas Assignment #1 Tax 2 (3178) : WithoutJoshua CabinasNoch keine Bewertungen

- Income Taxation Chapter 9Dokument11 SeitenIncome Taxation Chapter 9Kim Patrice NavarraNoch keine Bewertungen

- Taxation (Input Taxes)Dokument30 SeitenTaxation (Input Taxes)Lara Joy Junio100% (4)

- Gonzalo Puyat & Sons vs. City of Manila, G.R. No.17447, April 30, 1963 (7 CRA 790)Dokument9 SeitenGonzalo Puyat & Sons vs. City of Manila, G.R. No.17447, April 30, 1963 (7 CRA 790)Riza AkkangNoch keine Bewertungen

- Form of NBR IT Return For IndividualsDokument10 SeitenForm of NBR IT Return For IndividualsSumit GNoch keine Bewertungen