Das könnte Ihnen auch gefallen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Write About Global Catalog. How To View Replication Properties For AD PropertiesDokument19 SeitenWrite About Global Catalog. How To View Replication Properties For AD PropertiesChandan KumarNoch keine Bewertungen

- UNLV PHD InformaticsDokument3 SeitenUNLV PHD InformaticsAnonymous gzESmV9Noch keine Bewertungen

- Using Visio PDFDokument12 SeitenUsing Visio PDFAnonymous Af4ORJNoch keine Bewertungen

- STAAD ANALYSIS - Adrressing Requirements AISC 341-10 - RAM - STAAD Forum - RAM - STAAD - Bentley CommunitiesDokument2 SeitenSTAAD ANALYSIS - Adrressing Requirements AISC 341-10 - RAM - STAAD Forum - RAM - STAAD - Bentley Communitieschondroc11Noch keine Bewertungen

- Es ZC424 Course HandoutDokument13 SeitenEs ZC424 Course HandoutJAYAKRISHNAN.K.RNoch keine Bewertungen

- MIS AssignmentDokument3 SeitenMIS Assignmentsparepaper7455Noch keine Bewertungen

- P2P Technology User's ManualDokument8 SeitenP2P Technology User's ManualElenilto Oliveira de AlmeidaNoch keine Bewertungen

- Proposal SampleDokument33 SeitenProposal SampleMichael MesfinNoch keine Bewertungen

- ADPRO XO5.3.12 Security GuideDokument19 SeitenADPRO XO5.3.12 Security Guidemichael.f.lamieNoch keine Bewertungen

- Benefits Management PlanDokument1 SeiteBenefits Management PlanTariq AlzahraniNoch keine Bewertungen

- Free PDF Reader Sony Ericsson w595Dokument2 SeitenFree PDF Reader Sony Ericsson w595AdamNoch keine Bewertungen

- Controller, Asst - Controller, SR - Accountant, Accounting ManagerDokument3 SeitenController, Asst - Controller, SR - Accountant, Accounting Managerapi-72678201Noch keine Bewertungen

- 9000-41034-0100600 - Data Sheet - enDokument2 Seiten9000-41034-0100600 - Data Sheet - endAvId rObLeSNoch keine Bewertungen

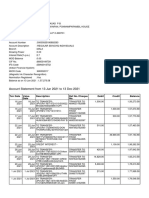

- Account Statement From 13 Jun 2021 To 13 Dec 2021Dokument10 SeitenAccount Statement From 13 Jun 2021 To 13 Dec 2021Syamprasad P BNoch keine Bewertungen

- Lea Dardanos Efi-Controller eDokument6 SeitenLea Dardanos Efi-Controller eadfumegaNoch keine Bewertungen

- A Microsoft Teams OutlineDokument2 SeitenA Microsoft Teams OutlineMaheswaren MahesNoch keine Bewertungen

- Axioms Activity (Games) PDFDokument3 SeitenAxioms Activity (Games) PDFKristopher TreyNoch keine Bewertungen

- CsoundDokument238 SeitenCsoundorchestration100% (1)

- BLCC610I Solution 6000 Installation Manual FTR2.6Dokument190 SeitenBLCC610I Solution 6000 Installation Manual FTR2.6ammy17643Noch keine Bewertungen

- CIS201 Chapter 1 Test Review: Indicate Whether The Statement Is True or FalseDokument5 SeitenCIS201 Chapter 1 Test Review: Indicate Whether The Statement Is True or FalseBrian GeneralNoch keine Bewertungen

- R-Net System R-Net System: Multi-Rehab Powerchair Control SystemDokument4 SeitenR-Net System R-Net System: Multi-Rehab Powerchair Control SystemMikel VillanuevaNoch keine Bewertungen

- Information Security Logical DesignDokument17 SeitenInformation Security Logical DesignnskaralsathyaNoch keine Bewertungen

- Fuzzy SetsDokument3 SeitenFuzzy SetsShugal On HaiNoch keine Bewertungen

- Iedscout: Versatile Software Tool For Working With Iec 61850 DevicesDokument12 SeitenIedscout: Versatile Software Tool For Working With Iec 61850 DeviceshmhaidarNoch keine Bewertungen

- Tda 7293Dokument16 SeitenTda 7293AntónioRodriguesNoch keine Bewertungen

- Question Bank - Module 1 and Module 2Dokument3 SeitenQuestion Bank - Module 1 and Module 2Manasha DeviNoch keine Bewertungen

- Cleaning and Diagnostic Tools 1Dokument14 SeitenCleaning and Diagnostic Tools 1flash driveNoch keine Bewertungen

- Seismic Processing - Noise Attenuation Techniques PDFDokument3 SeitenSeismic Processing - Noise Attenuation Techniques PDFDavid Karel AlfonsNoch keine Bewertungen

- CaFSET (Antigua) Office Workbook - Sixth Edition - Programming Concepts Sample PagesDokument4 SeitenCaFSET (Antigua) Office Workbook - Sixth Edition - Programming Concepts Sample PagescafsetNoch keine Bewertungen

- St. Therese School Second Periodic Test Mapeh 2Dokument4 SeitenSt. Therese School Second Periodic Test Mapeh 2dona manuela elementary schoolNoch keine Bewertungen