Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Consumer Reports New Cars - December 2022 USADokument204 SeitenConsumer Reports New Cars - December 2022 USAmang jim100% (4)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Remodeling Impact: D.I.Y.Dokument26 SeitenRemodeling Impact: D.I.Y.National Association of REALTORS®100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Lending Book PDFDokument335 SeitenLending Book PDFSarim ShahidNoch keine Bewertungen

- Mediation Resolution Agreement: Code of Ethics and Arbitration ManualDokument1 SeiteMediation Resolution Agreement: Code of Ethics and Arbitration ManualNational Association of REALTORS®Noch keine Bewertungen

- Mortgage Loan Process: All Right ReservedDokument20 SeitenMortgage Loan Process: All Right ReservedMadhuPreethi NachegariNoch keine Bewertungen

- 2018 Real Estate in A Digital World 12-12-2018Dokument33 Seiten2018 Real Estate in A Digital World 12-12-2018National Association of REALTORS®100% (2)

- Q 1 To 15 CIVIL LAW MOCK BAR QUESTIONS EDITED AND REVSIEDDokument12 SeitenQ 1 To 15 CIVIL LAW MOCK BAR QUESTIONS EDITED AND REVSIEDTyroneNoch keine Bewertungen

- Campaign and Election Timeline For 2021 Elected Office 01-23-2019Dokument1 SeiteCampaign and Election Timeline For 2021 Elected Office 01-23-2019National Association of REALTORS®Noch keine Bewertungen

- Form #A-17b: Arbitration Settlement AgreementDokument1 SeiteForm #A-17b: Arbitration Settlement AgreementNational Association of REALTORS®Noch keine Bewertungen

- Yun Aei 04 2019Dokument49 SeitenYun Aei 04 2019National Association of REALTORS®Noch keine Bewertungen

- Form #A-2: Request and Agreement To Arbitrate (Nonmember)Dokument2 SeitenForm #A-2: Request and Agreement To Arbitrate (Nonmember)National Association of REALTORS®Noch keine Bewertungen

- CEAM Notice of Request For MediationDokument1 SeiteCEAM Notice of Request For MediationNational Association of REALTORS®Noch keine Bewertungen

- Appeal of Grievance Committee (Or Hearing Panel) Dismissal or Appeal of Classification of Arbitration RequestDokument1 SeiteAppeal of Grievance Committee (Or Hearing Panel) Dismissal or Appeal of Classification of Arbitration RequestNational Association of REALTORS®Noch keine Bewertungen

- 2018 Q4 HOME SurveyDokument18 Seiten2018 Q4 HOME SurveyNational Association of REALTORS®Noch keine Bewertungen

- 2018 Profile of International Residential Real Estate in Florida 10-25-2018Dokument30 Seiten2018 Profile of International Residential Real Estate in Florida 10-25-2018National Association of REALTORS®100% (1)

- CEAM Ethics Form E20Dokument2 SeitenCEAM Ethics Form E20National Association of REALTORS®Noch keine Bewertungen

- 2017 11 Realtors Confidence Index 12-20-2017Dokument10 Seiten2017 11 Realtors Confidence Index 12-20-2017National Association of REALTORS®Noch keine Bewertungen

- 2018 11 Commercial Real Estate Economic Issues Forum Lawrence Yun Presentation Slides 11-02-2018Dokument55 Seiten2018 11 Commercial Real Estate Economic Issues Forum Lawrence Yun Presentation Slides 11-02-2018National Association of REALTORS®0% (1)

- Realtors Confidence Index Survey: October 2017Dokument10 SeitenRealtors Confidence Index Survey: October 2017National Association of REALTORS®Noch keine Bewertungen

- 2018 11 Residential Real Estate Economic Issues Trends Forum Lawrence Yun Presentation Slides 11-02-2018Dokument65 Seiten2018 11 Residential Real Estate Economic Issues Trends Forum Lawrence Yun Presentation Slides 11-02-2018National Association of REALTORS®100% (4)

- Housing Affordability in The US:: Trends & SolutionsDokument19 SeitenHousing Affordability in The US:: Trends & SolutionsNational Association of REALTORS®100% (1)

- 2018 Commercial Member Profile 11-15-2018Dokument122 Seiten2018 Commercial Member Profile 11-15-2018National Association of REALTORS®0% (1)

- 2018 Buyer Bios Profiles of Recent Home Buyers and Sellers 11-02-2018Dokument23 Seiten2018 Buyer Bios Profiles of Recent Home Buyers and Sellers 11-02-2018National Association of REALTORS®100% (1)

- Reform Summary of State Regulatory Guidance Prepared by A Law Firm Lawsuit Brought by A Dozen State Attorneys General Against DOL's RuleDokument1 SeiteReform Summary of State Regulatory Guidance Prepared by A Law Firm Lawsuit Brought by A Dozen State Attorneys General Against DOL's RuleNational Association of REALTORS®Noch keine Bewertungen

- Realtors Confidence Index Survey: September 2018Dokument10 SeitenRealtors Confidence Index Survey: September 2018National Association of REALTORS®100% (1)

- 2018 NAR Surveillance Survey TableDokument30 Seiten2018 NAR Surveillance Survey TableNational Association of REALTORS®0% (2)

- 22 Tex. Admin. Code 535.154 (2018) : ARELLO Archive Texas - Team BrokerageDokument2 Seiten22 Tex. Admin. Code 535.154 (2018) : ARELLO Archive Texas - Team BrokerageNational Association of REALTORS®Noch keine Bewertungen

- Supplement - Sample Local Association Antitrust PolicyDokument3 SeitenSupplement - Sample Local Association Antitrust PolicyNational Association of REALTORS®Noch keine Bewertungen

- Supplement: Sample Confidentiality AgreementDokument2 SeitenSupplement: Sample Confidentiality AgreementNational Association of REALTORS®Noch keine Bewertungen

- Chapter 1 Contract Q A 1Dokument35 SeitenChapter 1 Contract Q A 1Đinh Thị Mỹ LinhNoch keine Bewertungen

- Impact On Rate of Household SavingsDokument2 SeitenImpact On Rate of Household SavingsKEVIN JUGONoch keine Bewertungen

- INterpretation & Ratio AnalysisDokument28 SeitenINterpretation & Ratio AnalysisDawar Hussain (WT)Noch keine Bewertungen

- 804 MCQDokument15 Seiten804 MCQOlamilekan JuliusNoch keine Bewertungen

- Group Coursework - MBA IDokument11 SeitenGroup Coursework - MBA IBuatienoNoch keine Bewertungen

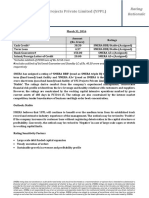

- YFC Projects Private Limited (YPPL) : Rating RationaleDokument2 SeitenYFC Projects Private Limited (YPPL) : Rating Rationalelalit rawatNoch keine Bewertungen

- Account Statement From 1 Apr 2018 To 31 Mar 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument8 SeitenAccount Statement From 1 Apr 2018 To 31 Mar 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceNarendra SaiNoch keine Bewertungen

- Microfinance Management Solution On Tally - ERP9 - MpowerDokument28 SeitenMicrofinance Management Solution On Tally - ERP9 - MpowerMilansolutionsNoch keine Bewertungen

- Chapter-1 Introduction To The StudyDokument70 SeitenChapter-1 Introduction To The StudyMOHAMMED KHAYYUMNoch keine Bewertungen

- U 5: M Money: Personal Best B1+ Word ListsDokument6 SeitenU 5: M Money: Personal Best B1+ Word Listsxiomara servonesNoch keine Bewertungen

- 1.1 Background of The StudyDokument15 Seiten1.1 Background of The StudyBhimad Municipality ChamberNoch keine Bewertungen

- Financial Statement AnalysisDokument3 SeitenFinancial Statement AnalysisglcpaNoch keine Bewertungen

- MCQ Financial Management: A Limited Partner in A Partnership. A Shareholder in A CorporationDokument15 SeitenMCQ Financial Management: A Limited Partner in A Partnership. A Shareholder in A CorporationMian RehmanNoch keine Bewertungen

- RatioanalysisanswersDokument5 SeitenRatioanalysisanswersAnu PriyaNoch keine Bewertungen

- AG Letter DocumentsDokument630 SeitenAG Letter DocumentsNational Legal and Policy CenterNoch keine Bewertungen

- Items Net Sales Gender Age Custome R Type of Customer Method of Payment Marital StatusDokument3 SeitenItems Net Sales Gender Age Custome R Type of Customer Method of Payment Marital StatusPeuli Das100% (1)

- U-Peso - PH Lending Corporation: "Bulacansan Ildefonsopoblacion365"Dokument5 SeitenU-Peso - PH Lending Corporation: "Bulacansan Ildefonsopoblacion365"Ma Leonora VijandreNoch keine Bewertungen

- Emebet Kebede FINALDokument65 SeitenEmebet Kebede FINALTefeNoch keine Bewertungen

- In Acc Chris Jean Paden BsaDokument6 SeitenIn Acc Chris Jean Paden BsaJurie BalandacaNoch keine Bewertungen

- PT Alfa YogaDokument6 SeitenPT Alfa Yogaghinaa mumthazahrachmatNoch keine Bewertungen

- CDFI Cert List 04-14-2021 FinalDokument159 SeitenCDFI Cert List 04-14-2021 FinalCalifornia WaterNoch keine Bewertungen

- Introduction To Accounting - Assignment 2 - Accounting Equation - Dr. GKDokument2 SeitenIntroduction To Accounting - Assignment 2 - Accounting Equation - Dr. GKshruthinNoch keine Bewertungen

- Chap 3 Co-Ops in The Community RevisedDokument10 SeitenChap 3 Co-Ops in The Community RevisediherrmanNoch keine Bewertungen

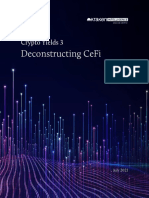

- Kraken Intelligence's Crypto Yields - Deconstructing CeFiDokument20 SeitenKraken Intelligence's Crypto Yields - Deconstructing CeFiSuraj UmarNoch keine Bewertungen

- Blank Diagram - Page 3Dokument1 SeiteBlank Diagram - Page 3Rey Joyce AbuelNoch keine Bewertungen

- Ref - No. 7854912-21572723-6: Syed AliDokument6 SeitenRef - No. 7854912-21572723-6: Syed AliPrince AliNoch keine Bewertungen